- Mashat reviews the year in development finance in annual report. (Smart Policy)

- Egycomex isn’t launching until 2H2021. (Commodities)

- Suez Cement is going private after trying to buy out as many minority shareholders as possible. (M&A Watch)

- Pharmacists Syndicate takes its beef with the 21st century to 3elagi with a lawsuit. (Dispute Watch)

- Enterprise talks to: Hoda Youssef, senior economist at the World Bank. (Spotlight)

- IMF’s Mahmoud Mohieldin on economic prospects for Egypt + the world heading into 2021. (Last Night’s Talk Shows)

- 2020 in review: How diversification and digitization guided infrastructure in 2020 and may continue to do so in 2021. (Hardhat)

- Planet Finance: Direct listings on NYSE get “ok” and iSheep have lots to talk about this morning.

Wednesday, 23 December 2020

At last, the year-end news slowdown has begun (touch wood)

TL;DR

WHAT WE’RE TRACKING TODAY

Good morning, wonderful people, and welcome to Christmas Eve Eve, for those of you who are observing. We can’t say we’re very interested in asking mom and dad for early permission to open just one gift that 2020 has left for us under the tree.

The big story this morning: Rania Al Mashat’s International Cooperation Ministry is out with an annual report. Bilingual, with a motion graphics summary for those of us who have the attention spans of fruit flies. It’s smart policy and transparency in one go — we have the rundown and links in this morning’s news well, below.

What’s up with the mutant virus market meltdown? US markets were mixed yesterday as optimism over vaccine rollouts and relief packages tempered fears of the spread of a new strain of covid-19, Bloomberg reports. Asian shares are up this morning, but futures suggest Wall Street and much of Europe will open in the red later today.

The end of year news slowdown appears to have finally begun (may we all give thanks and praise — and simultaneously touch wood). One industry that’s giving no sign of slowing down: The fast-growing non-bank financial services sector in general, and the consumer finance business in particular. Witness news yesterday that EFG Hermes’ Valu will offer finance to shoppers at Majid Al Futtaim malls and that Mastercard has inked an agreement with Carticard — a partner of Egabi FSI — that will allow the Egyptian company to sell loans directly through prepaid cards.

Wait, isn’t it supposed to be the other way around? Our inner Egyptian nationalist nevertheless welcomes news that Egypt is leading an FDI surge into Saudi Arabia. Bloomberg reports that “Saudi Arabia granted 20% more foreign investment licenses in the third quarter compared to the same period last year, with India and Egypt driving the increase despite efforts to attract American and European interest.” The kingdom issued nearly 2x as many licenses to Egyptian firms in 3Q as it did to either British or Lebanese outfits.

WHAT’S HAPPENING TODAY-

The UAE is rolling out the Sinopharm vaccine to its entire adult population without charge, the Financial Times reports. Emirati frontline healthcare workers have been receiving the jabs since September when it was given emergency authorization. Some 1 mn nationals and more than 8 mn foreign residents will now be given access to the shot.

Yes, vaccines are halal: Any shots that use pig derivatives are still halal, Dar Al Iftaa’s Khaled Omran told 90 Minutes’ Osama Kamal, assuaging fears from some Muslims that the vaccines could be religiously prohibited (watch, runtime: 5:58). Pork gelatin is a common ingredient in vaccines and works to increase their shelf life.

|

CIRCLE YOUR CALENDAR-

It’s interest rate day tomorrow: The Central Bank of Egypt meets tomorrow for its final monetary policy meeting of 2020. All 10 analysts and economists we spoke to earlier this week expect us to see out the remainder of the year with interest rates unchanged. The CBE has cut rates by 400 bps so far this year, leaving the overnight rate at 8.25% and the lending rate at 9.25%.

Taxpayers have until 31 December to file for a settlement under legislative provisions that passed earlier this year, said Hesham El Hamawy, the Finance Ministry’s advisor for tax disputes.

HOLIDAY HAPPENINGS-

The NYSE, Nasdaq and LSE will all run shorter trading sessions tomorrow in observance of Christmas Eve.

The EGX and banks in Egypt are typically closed on 1 January to close their fiscal years. Look for an announcement next week that 31 December will be off instead.

*** It’s Hardhat day — your weekly briefing of all things infrastructure in Egypt: Enterprise’s industry vertical focuses each Wednesday on infrastructure, covering everything from energy, water, transportation, urban development and as well as social infrastructure such as health and education.

In today’s issue: Part 2 of our Year in Review looks at how infrastructure development had to adapt to the turbulence this year through digitization and diversification. From the rise of digital services and digital payments to the development of the smart grid, digitizing our infrastructure was a major theme in 2020 and looks set to continue next year. Meanwhile, the government’s plan to transition to natgas cars became the biggest infrastructure diversification move of the year, while green bonds became the testing ground for our debt diversification strategy.

SMART POLICY

The year in development finance

The International Cooperation Ministry marshaled USD 9.8 bn to finance development projects in 2020, with USD 6.7 bn allocated to government projects and USD 3.1 bn going to support the private sector, Minister Rania Al Mashat said yesterday during the launch of the ministry’s annual report (pdf). Al Mashat — who took over the ministry a year ago — reviewed the measures taken by the government at large during the year to confront the repercussions of the “extremely difficult” pandemic. These measures include new financial policies, interest rate cuts, tax breaks, reducing energy prices for the industrial sector, and support for day laborers.

The transport sector received the most public sector financing this year at USD 1.7 bn, followed by water and sanitation with USD 1.4 bn, and energy with USD 677 mn. Budget support and social solidarity initiatives received USD 638 mn and USD 505 mn respectively.

The European Investment Bank provided the most financing for the private sector, earmarking USD 1.9 bn this year, followed by the European Bank for Reconstruction and Development with USD 641 mn and the International Finance Corporation with USD 421 mn. Al Mashat highlighted the effectiveness of initiatives taken by international institutions during covid-19 such as the World Bank’s USD 50 bn response fund targeting Africa.

Next year will see the private sector receive more financing, said Al Mashat, who highlighted green projects as a priority sector.

Want to hear more on the report? Al Mashat had a chat with each of Yahduth fi Misr’s Sherif Amer (watch, runtime: 8:11) and Masaa DMC’s Ramy Radwan (watch, runtime: 4:40) to recap the broad strokes of the report and the year in development finance for Egypt.

Want the tl;dr version? Watch it here (runtime: 1:30).

COMMODITIES

Groundhog day

The launch of the long-awaited commodities exchange (Egycomex) has again been delayed, after Internal Trade Development Authority (ITDA) Chairman and Egycomex head Ibrahim Ashmawy told Al Mal that it now won’t be seeing the light of day until the second half of 2021. Sources had initially hinted at a September 2020 start date, which was later pushed back to 1H2021 before yesterday’s news.

What can you trade? Ashmawy is now saying that wheat, oil, sugar, rice, iron and gold will all be accessible to traders from the get-go. He had first told us that traders would be able to buy and sell wheat, oil, sugar and rice at launch, but a few months later said that only wheat will be tradeable at first.

The private sector has gotten its foot in the door: EFG Hermes, Beltone and CI Capital will represent the private sector in the exchange that is otherwise dominated by state players. The firms will share a 49% stake with the National Bank of Egypt, Banque Misr and the Agricultural Bank of Egypt, while the remainder will be held by the EGX, the Internal Trade Development Authority, the General Authority For Supply Commodities, the Egyptian Holding Company for Silos and Storage, Misr Holding Company, and Misr for Central Clearing Depository and Registry.

WHILE WE’RE TALKING COMMODITIES- This year’s domestic wheat harvest is expected to yield an extra 1 mn tonnes, for a total of 9 mn tonnes, Al Mal reports. The Agriculture Ministry is banking on a newly planted hybrid wheat variety and improved irrigation techniques to provide productivity gains. This would allow Egypt — the world’s largest wheat importer — to reduce its reliance on foreign supply and import 13 mn tonnes to meet its 21 mn tonne domestic consumption needs.

M&A WATCH

Sign of the times for cement

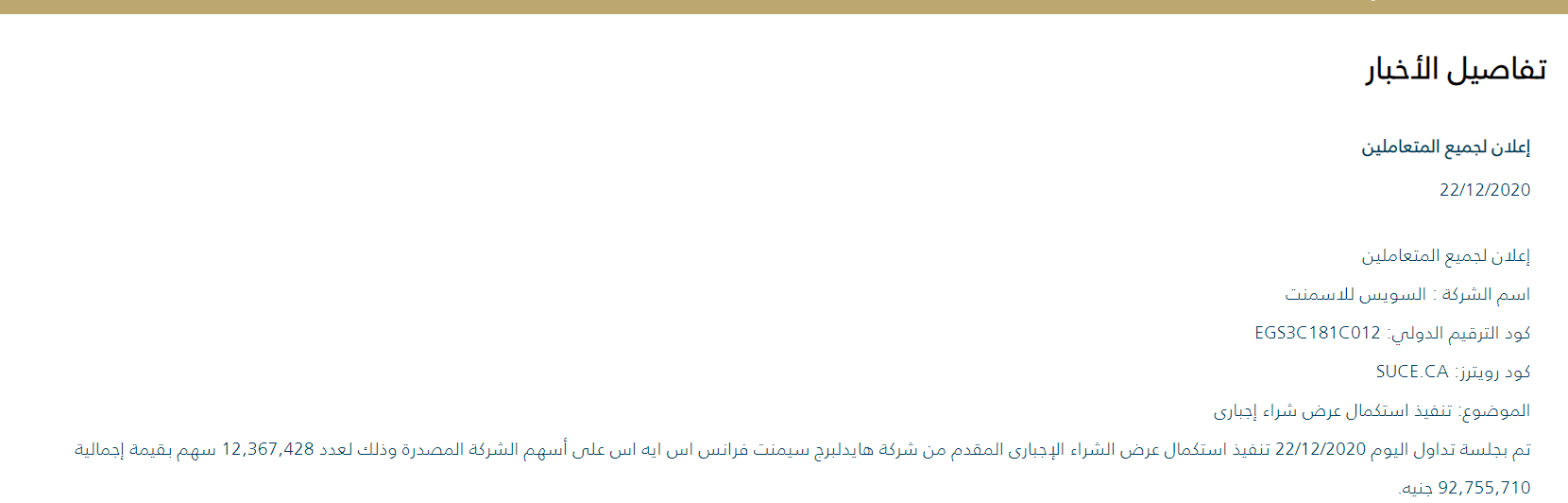

Suez Cement is going to go private after trying to buy out as many minority shareholders as possible. Shareholders sold some 12.4 mn shares for EGP 92.7 mn to Suez parent company Heidelberg Cement, the EGX said without giving further details. Heidelberg had targeted 59.8 mn shares at a MTO price of EGP 7.5 a share. This would’ve given it ownership of the remaining 33% it doesn't already hold.

{kind=link}

Now that the MTO is over, Heidelberg Cement will take Suez’s shares off the EGX. A regulatory filing (pdf) earlier this month said that the Suez board had given the go-ahead to the German parent to purchase the shares of shareholders objecting to the delisting plan or negatively affected by it at the MTO price. Suez Cement subsidiary Tourah Cement, which is indirectly owned by Heidelberg, is also part of the same plan.

What’s going on? The cement industry in Egypt has been suffering for years from a drawn out supply glut that has seen producers bleed cash, potentially leaving as many as six players on the cusp of exiting the market. Tourah Cement suspended operations last year, and is currently struggling to return to get into the black. Suez Cement’s losses have also been widening in recent quarters, with sales struggling to pick up.

DISPUTE WATCH

Revenge of the Luddites, Part II

The Pharmacists Syndicate is taking its beef with the 21st century to 3elagi, filing a lawsuit yesterday against the digital pharmacy platform for selling directly to consumers without a pharmacist as an intermediary, Masrawy reports. The case accuses the app of contravening a 1955 law that says only pharmacies and hospitals can sell meds to consumers. The lawsuit also accuses the company of violating article 27 of the Cybercrimes Act, which criminalizes the use of the internet to aid in committing a crime.

The syndicate already picked this bone with distributor Ibnsina Pharma, calling for a boycott of the company after Ibnsina said it planned to acquire a 75% stake in the app’s mother company, 3elagi Tech. Ibnsina denied wrongdoing but walked away from the purchase last week. Pharmacists are Ibnsina’s core customers.

3elagi links customers to stores around the country offering direct delivery. The company’s website claims its algorithm selects pharmacists based on their prices and location. Yodawy uses a similar model, but its business model emphasizes benefit management for ins companies. The Pharmacists Syndicate has long acted as a gatekeeper to the profession and insists that any sale of medicines outside of brick and mortar pharmacies (owned by an individual, licensed druggist) is illegal.

SHIPPING

The Suez Canal is preparing for another trade slowdown

More breaks at the Suez Canal: Liquified petroleum gas shippers will continue to pay lower Suez Canal transit fees until June 2021 as the government tries to support revenues as the pandemic continues to sap trade, the Suez Canal Authority said, according to Al Mal. Since April, carriers traveling between southeast Asia and the US have gotten breaks ranging between 24% and 75%, depending on their route. The measures were introduced by the authority in response to a slowdown in global trade caused by the pandemic.

They’re not the only ones getting a hand: The authority earlier this week slashed transit fees for large oil tankers traveling between northern Europe and southeast Asia by 48%.

INVESTMENT WATCH

Monginis to open second factory in 2Q2021

Sweetmaker Monginis is planning to inaugurate its planned EGP 100 mn factory in Sadat City in 2Q2021, Business Development Director Osama Soliman said. The company had been planning to open the factory — its second in Egypt — by the end of the year or in early January, after sales recovered 70% from lows seen during the height of the pandemic earlier in the year. The Indian company is also planning to invest EGP 200 mn to double its branches to 200 by 2022, Soliman said last week.

COVID WATCH

Closing in on 800 new cases per day

The Health Ministry reported 788 new covid-19 infections yesterday, up from 718 the day before. The ministry also reported 37 new deaths, bringing the country’s total death toll to 7,167. Egypt has now disclosed a total of 127,601 confirmed cases of covid-19.

Setting up more quarantine facilities: Parts of Kasr Al Aini Hospital will be turned into a dedicated covid-19 quarantine area to accommodate the increase in cases, Masrawy reports. As of last week, around 60% of ICU beds were occupied and a third of ventilators at isolation facilities were in use.

There are currently some 1,450 Egyptian expats stuck in transit in the UAE, Turkey, and Oman on their way back to Kuwait, which has suspended all air travel for one week amid fears of a new, more transmissible strain of the virus, Emigration Minister Nabila Makram Ebeid said yesterday. The ministry is working with hotels and other agents to arrange for the travelers to find accommodation until the suspension is lifted, Ebeid told Masaa DMC’s Ramy Radwan (watch, runtime: 5:21).

Should we expect another repatriation campaign? Not just yet, Ebeid said. The ministry is “keeping an eye” on Egyptians who are facing difficulties coming home because of flight suspensions, but hasn’t yet made a decision to operate repatriation flights.

It will take two weeks until we know if the Pfizer / BioNTech vaccine is effective against the new virus strain as the companies gather data from ongoing clinical trials, Sky News reports BioNTech CEO Ugur Sahin as saying. A new vaccine, if necessary, could be manufactured within 6 weeks, said Sahin. The mutant virus is hitting parts of Europe after being discovered in the UK and is believed to be 70% more transmissible, but not necessarily more deadly.

Don’t panic yet: The BioNTech boss said there was a “relatively high” chance that the vaccine will be effective in combating the new strain, explaining that the new form of covid-19 shares 99% of the proteins with the previous iterations.

This publication is proudly sponsored by

ENTERPRISE+: LAST NIGHT’S TALK SHOWS

The highlight of last night’s talk shows: IMF executive board member Mahmoud Mohieldin’s chat with Kelma Akhira’s Lamees El Hadidi on prospects for individual Arab economies and the global economy at large heading into 2021 (watch, runtime: 31:39).

Egypt must stay the course on reforms and start moving towards its plans for deeper reforms, including doubling down on investments in healthcare, education, and infrastructure to create sustainable, long-lasting growth, Mohieldin said. The government has so far shown a high degree of commitment to the program, which has helped Egypt earn and maintain the confidence of international organizations such as the IMF, he told Lamees.

We could see the global economy bounce back next year to register 2-3% growth if the covid-19 vaccines are 85-95% effective, but the recovery is going to vary greatly between individual sectors (think tourism versus fintech, for example) and also between countries that suffered or benefited differently from the pandemic. Mohieldin also touched on the situation in Lebanon, stressing that a political resolution is the only absolute fix for the economy.

Also on the airwaves last night:

- Gastec Chairman Abdel Fattah El Farahat explained how to go about converting a vehicle to run on natgas (watch, runtime: 1:09)

- Masaa DMC recapped the national projects that were inaugurated this year (watch, runtime: 2:42)

SPOTLIGHT

Enterprise talks to: Hoda Youssef, senior economist at the World Bank

Embracing the private sector: An interview with Hoda Youssef, senior economist at the World Bank. Earlier this week, the World Bank and the International Finance Corporation published an in-depth report on the barriers facing private investment in Egypt which prevent local industries from becoming internationally competitive and integrating into global supply chains. Covering state involvement in the economy, trade barriers and the legal system, the paper identifies the key impediments to private sector development and offers a detailed policy prescription for how the future might look different. Tap / click here for full coverage.

To go deeper into some of the issues raised in the report, as well as gauge how the economy is responding to the pandemic, we talked to World Bank senior economist and team leader of the report Hoda Youssef. Youssef is a MENA-focused economist with 15 years’ experience researching macro trends, private sector development and political economy.

The key takeaways:

- The trajectory of Egypt’s — and the world’s — economic recovery is still TBC

- Our debt load remains a problem but progress is being made on diversification

- Easing tariffs doesn’t have to mean pain

- Privatization can only do so much to level the playing field

- Firm but fair antitrust rules are a must to protect market competition

- Levelling up the digital economy starts in the classroom

- Intelligent deregulation can nudge businesses to go legit.

Edited excerpts of our conversation:

The economic recovery in Egypt — like the rest of the world — remains in the balance: The outlook is highly uncertain, and the impact of the pandemic will depend on the duration and severity of the crisis both domestically and abroad. As we speak, various restrictive measures have been reintroduced around the world as covid-19 continues to spread, and in Egypt daily new cases are on an increasing trend.

The pace of the recovery will hence vary considerably, with greater weakness in countries that have larger outbreaks or greater exposure to global spillovers, through tourism, exports, remittances or capital flows. For Egypt, our most recent projection for growth in FY2020-2021 is 2.3%. This could however be revised as things develop and more information becomes available.

Egypt has contained the fallout from the crisis, but attention now turns to Reform 2.0: In response to this crisis, Egypt undertook key measures to curb the spread of covid-19, and to mitigate its adverse implications on the economy. Many of these measures were taken preemptively. Social protection programs were also scaled up, to help mitigate the impact on the most vulnerable groups, including for informal workers and Takaful and Karama beneficiaries.

Going forward, the government needs to focus on continuing the reform agenda and embarking on a second generation of reforms to address the structural constraints on the economy, strengthen its resilience in the face of crises, and ensure a sustainable and inclusive growth model.

The national debt remains high but progress is being made on diversification. Egypt entered the crisis with a broadly stable macroeconomic environment, helped by its important reform measures. Yet, debt levels are still elevated despite falling from 108% of GDP to 87% over the previous three years. And government external debt in absolute terms is remarkably higher than before the reforms, jumping from USD 35 bn to USD 69.4 bn over the same period

A positive development is on the maturity structure, which Egypt has begun to extend to an average time-to-maturity of 3.3 years in FY2019-2020 compared to 1.9 years in FY2017-2018. Yet, the latest available official numbers show that domestic debt maturity structure remains unfavorable, with 67% being short-term debt. While we expect debt levels to exceed pre-crisis targets, Egypt continues, however, to diversify the sources of external financing — including the issuance of its first sovereign green bond — and widen the investor base.

FDI needs a pick-me-up: It will be important for Egypt to prioritize steps to attract FDI and facilitate trade. This is important as FDI inflows (while declining globally), have been low and declining in Egypt, even prior to the crisis and have remained concentrated in the extractives sectors, while the share of FDI in more labor-intensive sectors, such as services, manufacturing, and construction, remained modest.

Privatization can only do so much to level the playing field: The issue is not privatization but the need to ensure a level playing field in sectors and markets where both public and private operators compete. Lack of a clear separation between the State’s regulatory and operational bodies in certain sectors can create conflicts of interest as regulators might have incentives to protect public operators under their supervision, and this can create risks for the private sector. For instance, the Communications Ministry oversees both the National Telecom Regulatory Authority (NTRA) and Telecom Egypt — an SOE that is 80% owned by the government and holds a dominant position in the sector.

But it can lead to improved firm performance, healthier public finances, and positive macroeconomic effects — when done right. As it prepares to open up military-owned firms to investors, the State will need to focus on how the privatization is done. Specifically, there will be a need to create an encouraging environment by undertaking other reforms to strengthen competition and ensure a level-playing field, and prepare the enterprises for privatization by making the necessary disclosure on their performance.

It will also be very important for the sale to be conducted with openness and through a transparent process. Stronger protection for minority shareholders will also be essential, given the possibility that some privatizations could involve retention of a government stake and / or participation of large private investors.

Strengthening antitrust legislation is key: The ability to control anticompetitive effects of mergers is an important feature for competition regimes and most competition laws around the world include such powers. Merger control allows competition authorities to act ex ante rather than ex post. In other words, instead of prosecuting anticompetitive practices once they have taken place and harmed consumers, they can limit the risks beforehand.

Nevertheless, we cannot forget that market consolidation is part of the day to day business of the private sector, especially in the context of covid-19. Thus, merger control policy should allow for beneficial dynamic changes in market structure without unjustifiably increasing the cost of doing business.

Tap or click here to continue reading the discussion on our website, including trade, customs reform, how to level-up the digital economy, industries that will benefit from going digital, and how to drag the informal economy (kicking and screaming) into the light.

EGYPT IN THE NEWS

On an otherwise quiet morning in the foreign press: The Committee to Protect Journalists is calling on the government to release satirist Shadi Abou Zeid and Egyptian director Mayye Zayed’s documentary on Egypt’s women weightlifters “Lift Like a Girl” is getting more digital ink from Reuters.

ALSO ON OUR RADAR

Al Azhar issued a fatwa confirming that joining the Ikhwan is religiously forbidden on grounds that the group has engaged in “distorting some texts, taking them out of their context, and using them to achieve personal goals or interests and corrupting the land.”

A handful of headlines we’re keeping an eye on this morning:

- Palm Hills Development’s London-listed GDRs were written off yesterday (pdf), a plan the company approved in August.

- A new system to disburse export subsidies based on company size and turnover will be introduced in January.

PLANET FINANCE

Powered by

![]()

GAME CHANGER for US capital markets- The US has given the green light to direct listings on the New York Stock Exchange in a move that will surely cut into the feel wallets allocated to investment banks across the pond, the Financial Times writes.

iSheep have plenty to chew over today, including the prospect (once again) of an Apple Car (this time by 2024) and news that Elon Musk tried to shop Tesla to the tech giant, but couldn’t convince CEO Tim Cook to sit down for a cup of coffee. Apple shares are heading into the final days of trading up some 80% year-on-year for the second year in a row. CNBC has more.

US companies are going full George Romero, borrowing a record USD 2.5 tn this year and increasing leverage at investment grade companies to an all-time high. The number of so-called zombie companies — firms whose profits only allow them to meet interest payments on their debt — are nearing historical peaks. The Financial Times says the 2020 bond mania has left balance sheets in a “far riskier” state, as Fed policy leaves companies ever more reliant on emergency liquidity.

Peak 2020: SoftBank is launching a SPAC so it can … buy SoftBank assets. The Financial Times reports that the company wants to raise USD 604 mn of public money so it can acquire a Japanese tech firm it has already invested in. This seems fine…

There’s been a changing of the guard at Saudi’s USD 360 bn sovereign wealth fund as it prepares to step up its involvement in the economy, Bloomberg reports. Among the new faces are Fahad Alsaif (LinkedIn), who has been appointed head of corporate finance, and Rania Nashar, who was the first woman in the country to head up a bank, was tapped to become senior adviser to PIF Governor Yasir Al-Rumayyan.

|

|

EGX30 |

10,656 |

+0.7% (YTD: -23.7%) |

|

|

USD (CBE) |

Buy 15.64 |

Sell 15.74 |

|

|

USD at CIB |

Buy 15.63 |

Sell 15.73 |

|

|

Interest rates CBE |

8.25% deposit |

9.25% lending |

|

|

Tadawul |

8,681 |

+1.7% (YTD: +3.5%) |

|

|

ADX |

5,110 |

+0.7% (YTD: +0.7%) |

|

|

DFM |

2,481 |

+0.8% (YTD: -10.3%) |

|

|

S&P 500 |

3,687 |

-0.2% (YTD: +14.1%) |

|

|

FTSE 100 |

6,453 |

+0.6% (YTD: -14.4%) |

|

|

Brent crude |

USD 50.08 |

-0.6% |

|

|

Natural gas (Nymex) |

USD 2.77 |

-0.5% |

|

|

Gold |

USD 1,867.10 |

-0.2% |

|

|

BTC |

USD 23,723.66 |

+3.8% |

The EGX30 rose 0.7% yesterday on turnover of EGP 1.1 bn (19.3% below the 90-day average). Domestic investors were net sellers. The index is down 23.7% YTD.

In the green: Juhayna (+7.3%), GB Auto (+6.9%) and TMG Holding (+3.4%).

In the red: Dice (-3.5%), Export Development Bank (-2.9%) and Qalaa Holdings (-1.8%).

AROUND THE WORLD

Qatari media outlets are “undermining” a resolution to its feud with the Arab Quartet, the UAE’s Foreign Affairs Minister Anwar Gargash said in a tweet yesterday. Gargash’s statement comes amid signals that Saudi Arabia, the UAE, Bahrain and Egypt were inching toward ending the three-year-old flap. The four countries have been demanding that Doha shut down state mouthpiece Al Jazeera as a condition to resolving the stand-off.

Bibi could be dethroned as Israel’s prime minister in the country’s fourth election in two years, as his fragile coalition government with centrist rival Benny Gantz collapsed after the Knesset failed to approve a state budget. The vote — scheduled for 23 March — will come a few weeks after Netanyahu’s trial for bribery and fraud “kicks into high gear,” Bloomberg notes.

The USD 892 bn covid relief bill passed in the United States may be on the rocks after Agent Orange threatened yesterday not to sign it, arguing that he wants the USD 600 cheques for every American to be upgraded to USD 2k apiece.

2020 in review: How diversification and digitization guided infrastructure in 2020 and may continue to do so in 2021: In part 1 of our Year in Review, we looked at how infrastructure businesses, particularly in energy, construction, and shipping, were hit by covid-driven supply chain disruptions, while businesses like ride-hailing saw demand lessen amid social distancing. Now in part 2, we look at digital infrastructure and diversification — two other big themes for the year.

By adaptation we mean digitization and diversification. From e-commerce, fintech, and e-payments, digitizing basic services was a big theme of 2020. We’re also seeing moves on that front in our electricity infrastructure as we transition towards a smart grid. Meanwhile, we’re seeing diversification become a major theme in infrastructure, especially with regards to our transition to natural gas, and the move towards diversifying our funding of infrastructure.

The explosion of digital payments by the numbers: This boom in digital payments, fintech and e-commerce is being witnessed across all metrics this year. Ceilings on contactless transactions have doubled since the start of the pandemic, allowing consumers to make contactless payments for larger purchases. Between the beginning of the outbreak and June, e-commerce sales in Egypt shot up 80%, Jumia Egypt CEO Hisham Safwat said at the time. 15% of businesses in Egypt reported more online sales now than before the pandemic, according to a survey by Facebook, the World Bank, and the Organization for Economic Cooperation and Development.

Meanwhile, the number of mobile wallets in Egypt has jumped at least 17% to 14.4 mn between March and October as the pandemic boosted digital payments, the National Telecom Regulatory Authority said in a report last month. The number of e-payment cards in use also rose 7% in the first six months of 2020, rising to 39.6 mn from 36.7 mn at the end of December, according to CAPMAS data from September. The figure includes credit cards, debit cards and prepaid cards. There were 18.28 mn prepaid cards in use by the end of June.

In addition to usage, we’re seeing an expansion in the types of services being offered. We’re seeing traditional banks such as Banque Misr extending banking services through apps such as Masary, including QR code payments, Meeza card services, and accepting e-payment cards. Fawry and Banque du Caire, meanwhile, have set up an instant remittance transfer service through Fawry outlets. We’re also seeing a series of partnerships since the covid-19 crisis between education providers and e-payments and e-finance companies to facilitate tuition payments.

The lesson from startup land was clear: Businesses that reduced face-to-face contact through digitization fared well. Delivery services and healthtech startups saw a substantial increase in demand, with daily orders at online pharma app 3elagi having doubled or even tripled by late April. Digital healthcare platform Vezeeta accelerated the launch of its new telehealth service by several months, helping to plug a gap as physical consultations decreased. It was no different in infrastructure-based startups, such as digital trucking marketplace Trella, which found that as covid concern grew, clients became much more amenable to digitizing payment mechanisms and documents used to transfer equipment, like proof of delivery.

Even electricity is set to be transformed by a digital shift: Egypt’s electricity generation capacity far outstrips network transmission capacity, creating a huge oversupply while failing to fully eradicate persistent power cuts. The national grid itself relies on outdated technology that incurs major maintenance costs and makes identifying the causes of interruptions difficult. So the Electricity Ministry plans to turn the old grid into a smart grid that incorporates digital technology into the traditional electrical system. It lets electricity distribution companies analyze big data on consumption using IT infrastructure embedded into control centers. This maximizes the efficiency of electricity usage, and lets engineers monitor performance and anticipate problems. It can also offer mechanisms for electricity storage.

Plans to set up the smart grid moved forward this year: 15 smart control centers out of a planned 47 were set to be rolled out, with Schneider Electric having snapped up four of them for EGP 4.7 bn as of mid-August.

Perhaps the biggest move in diversification this year was our natgas transition: This year saw one of the most ambitious infrastructure turnarounds, as Egypt looks to move all passenger cars to run natural gas in a bid to drastically cut fuel costs while bringing a reduction in Egypt’s oil imports, and less pollution. The first phase of the plan would see some 250k old cars taken off the road and outfitted with dual-fuel engines by the end of 2023 in Cairo, Giza, Alexandria, and Qalyubia. Initial estimates suggested the program will ultimately see an estimated 1.8 mn cars converted or replaced at a cost of EGP 320 bn, officials told us back in July. The plan will run on three tracks:

#1- Setting up the infrastructure: At least another 366 natgas stations will be opened by the government at a cost of EGP 6.7 bn over the next two years, Trade Minister Nevine Gamea said. In tandem, the government is considering reviving Safi Misr, a state company that will partner with Italy’s Landi Renzo, with the aim of accelerating the establishment of conversion and fuel stations. The government is also looking to foreign companies to help expedite the conversions of cars to natgas.

#2- Providing financial incentives to transition: The Trade and Industry Ministry, CBE, and the MSME Development Agency is setting up financial incentives to fund the program, offering EGP 1.2 bn in low-interest loans to owners of vehicles over 20 years old, while those with younger vehicles can access zero-interest finance to outfit them with new engines.

#3- Getting auto assemblers on board: Currently there are several models of locally-assembled passenger cars and microbuses that use natural gas by Chevrolet, Hyundai, Lada, and BYD. But in order to buy into the plan further, auto players had been asking for further incentives back in August. There now appears to be plans for dual-fuel cars assembled locally to be in line for value-added tax and customs breaks on inputs. We’re now hearing that carmakers Toyota, Foton, and Jinbei are expected to begin locally assembling natgas models in 2021, officials tell us. Meanwhile, Brilliance Auto Group is in talks with its parent company, HuaChen Group Auto Holding, about potentially participating with locally-assembled microbuses. An expo inviting private sector companies to join in on the effort is scheduled to take place in January 2021.

Infrastructure became the testing ground for our debt diversification strategy: In September, Egypt sold its first green bonds — a component of the Finance Ministry’s debt diversification strategy — listing USD 750 mn in green bonds on the London Stock Exchange. Based on the Finance Ministry’s Green Framework, green bonds are set to be a main source of funding for some of our most important upcoming and existing major infrastructure projects. These include clean transportation, renewable energy, pollution prevention and control, climate change adaptation, energy efficiency, and water and wastewater management.

Will corporate green bonds follow next year? As we’re seeing with sukuks, a number of companies have been exploring buying into this new instrument. CIB was supposed to be the first to test the water with a USD 65 mn offering in collaboration with the International Finance Corporation (IFC) in 3Q2020. The proposal would have seen the IFC invest USD 65 mn in the first tranche of the five-year bonds. If successful, the IFC will bring its investment up to USD 100 mn in another tranche. It is unclear whether the offering will go ahead in 2021. Meanwhile, BariQ, Raya’s recycling unit, is expected to take its green bonds to market in early 2021.

Your top infrastructure stories for the week:

- Egyptera licensed three companies to set up solar power stations with a collective capacity of 19.4 MW.

- Egypt is considering building a logistics terminal on the Sudanese border that could act as a distribution hub in the region for leather goods, appliances, sugar and pharma products.

- Egypt could be getting EUR 1 mn courtesy of the EBRD next month to fund feasibility studies for the Tenth of Ramadan, Beni Suef and Borg El Arab dry ports, General Authority for Land and Dry Ports head Amr Ismail said, according to the local press.

- The Public Enterprises Ministry signed a contract with Vodafone and Viber to install a data management system in 63 state-owned enterprises that will automate workflow, according to Hapi Journal.

CALENDAR

23 December (Wednesday): Prime Minister Moustafa Madbouly will deliver the keynote address at the 19th edition of Dubai’s Arab Media Forum, held virtually this year.

24 December (Thursday): The CBE’s Monetary Policy Committee will meet to review interest rates.

25 December (Friday): Western Christmas.

31 December (Thursday): Egypt-UK post-Brexit trade agreement to take effect.

31 December (Thursday): Deadline for car owners to comply with traffic regulations to install a RFID electronic sticker on their cars.

31 December (Thursday): Deadline for EGX-listed companies to comply with regulations requiring at least one member of their boards of directors be a woman.

1Q2021: The Annual Egypt Automotive Summit will be held.

January 2021: Expo to promote auto natgas transition strategy.

January 2021: US Treasury Secretary Steven Mnuchin is set to visit Egypt.

1 January 2021 (Friday): New Year’s Day, national holiday.

7 January 2021 (Thursday): Coptic Christmas, national holiday.

13-31 January (Wednesday-Sunday): Egypt will host the 2021 Men’s Handball World Championship at the Giza Pyramids.

Mid-January: Local expo to display natural gas-powered and dual-engine vehicles for Egypt’s car replacement program.

17 January 2021 (Sunday): A court will hold a postponed hearing to look into an appeal by Syria’s Anataradous against an arbitration ruling in favor of Amer Group and Amer Syria in case 445 of 2019.

25 January 2021 (Monday): 25 January revolution anniversary / Police Day.

25-29 January 2021 (Monday-Friday): The World Economic Forum’s “Davos Dialogues” will take place virtually.

26-28 January (Tuesday-Thursday): Future Investment Initiative, Riyadh, Saudi Arabia.

28 January 2021 (Thursday): National holiday in observance of 25 January revolution anniversary / Police Day.

4 February 2021 (Thursday): The CBE’s Monetary Policy Committee will meet to review interest rates.

6-18 February 2021 (Saturday-Thursday): Mid-year school break.

20 February 2021 (Saturday): The CBE’s Monetary Policy Committee will meet to review interest rates.

18 March 2021 (Thursday): The CBE’s Monetary Policy Committee will meet to review interest rates.

12 April 2021 (Monday): First day of Ramadan (TBC).

25 April 2021 (Sunday): Sinai Liberation Day.

29 April 2021 (Thursday): National holiday in observance of Sinai Liberation Day.

29 April 2021 (Thursday): The CBE’s Monetary Policy Committee will meet to review interest rates.

3 May 2021 (Monday): Sham El Nessim.

6 May 2021 (Thursday): National holiday in observance of Sham El Nessim.

12-15 May 2021 (Wednesday-Saturday): Eid El Fitr (TBC).

18-21 May 2021 (Tuesday-Friday): The World Economic Forum’s annual meeting will be held under the theme of “The Great Reset” in Lucerne-Bürgenstock, Switzerland

31 May-2 June 2021 (Monday-Wednesday): Egypt Petroleum Show, Egypt International Exhibition Center, Nasr City, Cairo.

30 May-15 June 2021 (Wednesday-Thursday): Cairo International Book Fair.

1 June 2021 (Tuesday): The IMF will conduct a second review of targets set under the USD 5.2 bn standby loan approved in June 2020 (proposed date).

17 June 2021 (Thursday): The CBE’s Monetary Policy Committee will meet to review interest rates.

24 June 2021 (Thursday): End of the 2020-2021 academic year.

26-29 June 2021 (Saturday-Tuesday): The Big 5 Construct Egypt, Cairo International Convention Center

30 June- 15 July 2021: National Book Fair.

2H2021: Egypt’s Commodities Exchange (Egycomex) will begin trading.

30 July-3 August 2021 (Thursday-Monday): Eid Al Adha, national holiday (TBC).

5 August 2021 (Thursday): The CBE’s Monetary Policy Committee will meet to review interest rates.

16 September 2021 (Thursday): The CBE’s Monetary Policy Committee will meet to review interest rates.

1 October 2021-31: March 2022 (Friday-Thursday): Postponed Expo 2020 Dubai.

28 October 2021 (Thursday): The CBE’s Monetary Policy Committee will meet to review interest rates.

13-17 December 2021: United Nations Convention against Corruption, Sharm El Sheikh, Egypt.

16 December 2021 (Thursday): The CBE’s Monetary Policy Committee will meet to review interest rates.

Enterprise is a daily publication of Enterprise Ventures LLC, an Egyptian limited liability company (commercial register 83594), and a subsidiary of Inktank Communications. Summaries are intended for guidance only and are provided on an as-is basis; kindly refer to the source article in its original language prior to undertaking any action. Neither Enterprise Ventures nor its staff assume any responsibility or liability for the accuracy of the information contained in this publication, whether in the form of summaries or analysis. © 2022 Enterprise Ventures LLC.

Enterprise is available without charge thanks to the generous support of HSBC Egypt (tax ID: 204-901-715), the leading corporate and retail lender in Egypt; EFG Hermes (tax ID: 200-178-385), the leading financial services corporation in frontier emerging markets; SODIC (tax ID: 212-168-002), a leading Egyptian real estate developer; SomaBay (tax ID: 204-903-300), our Red Sea holiday partner; Infinity (tax ID: 474-939-359), the ultimate way to power cities, industries, and homes directly from nature right here in Egypt; CIRA (tax ID: 200-069-608), the leading providers of K-12 and higher level education in Egypt; Orascom Construction (tax ID: 229-988-806), the leading construction and engineering company building infrastructure in Egypt and abroad; Moharram & Partners (tax ID: 616-112-459), the leading public policy and government affairs partner; Palm Hills Developments (tax ID: 432-737-014), a leading developer of commercial and residential properties; Mashreq (tax ID: 204-898-862), the MENA region’s leading homegrown personal and digital bank; Industrial Development Group (IDG) (tax ID:266-965-253), the leading builder of industrial parks in Egypt; Hassan Allam Properties (tax ID: 553-096-567), one of Egypt’s most prominent and leading builders; and Saleh, Barsoum & Abdel Aziz (tax ID: 220-002-827), the leading audit, tax and accounting firm in Egypt.