- Saudi wealth fund buys stakes in EGX companies for USD 1.3 bn. (M&A Watch)

- Egypt has been a MENA M&A hotspot so far in 2022. (M&A Watch)

- Inflation hits new three-year high in July. (Economy)

- Today: We’re expecting to get the A-Z of gov’t plans to ration the nation’s electricity usage. (What We’re Tracking Today)

- The Mogamma’s face-lift could be finished in 2024. (Investment Watch)

- Swvl to sell USD 20 mn in fresh stock via private placement. (Investment Watch)

- Saybad ups its offer for Pachin. (M&A Watch)

- Convertedin + Sharwa close funding rounds. (Startup Watch)

- The threat of greenwashing accusations is weighing on ESG debt markets. (Planet Finance)

Thursday, 11 August 2022

AM — Saudi wealth fund buys stakes in EGX companies for USD 1.3 bn

TL;DR

WHAT WE’RE TRACKING TODAY

Good morning and Happy Thursday, ladies and gents. We have a packed, M&A-heavy issue for you to close out the week, so let’s jump into it.

WHAT’S HAPPENING TODAY-

Expect to hear more about the Madbouly government’s plans to ration electricity today: The cabinet will announce the full details of the measures it will implement to restrict public electricity consumption following its meeting today. Under plans announced by Prime Minister Moustafa Madbouly on Tuesday, the government will try to reduce the amount of natural gas used by the country’s power stations and instead export it abroad to bring in more hard currency. It hopes to export around 15% of that gas, which the PM said yesterday would bring in USD 450 mn a month in revenues.

ICYMI- From the few details available, here’s what we can expect: Ministers will likely announce plans to reduce lighting in public spaces, ration electricity usage in government buildings, hotels and sports venues, and limit the use of ACs in malls from next week.

Daylight-saving time could also make a comeback as soon as next year, cabinet spokesperson Nader Saad said on Tuesday (watch, runtime: 6:50).

The Madbouly government’s public consultations on its state ownership policy continue today, with experts and think tanks weighing in. Every Sunday, Tuesday, and Thursday see workshops on how privatization plans will affect specific industries. You can find more details on the schedule of the meetings here.

NEXT WEEK + BEYOND-

Ghazl El Mahalla IPO: The retail portion of Ghazl El Mahalla’s mini-IPO will wrap this coming Sunday, 14 August.

MNHD shareholders have the final word on SODIC takeover bid: Madinet Nasr Housing and Development will hold a general assembly meeting on Tuesday, 16 August, to decide whether to allow SODIC to conduct due diligence ahead of a potential takeover.

Interest rates: The Central Bank of Egypt will meet to discuss interest rates next Thursday, 18 August. Look for our poll of economists on Sunday to see where they see interest rates landing next week.

National Dialogue: The board of trustees overseeing the National Dialogue will hold its next meeting on 27 August. On the agenda: Choosing the rapporteurs for all of the committees and subcommittees of the social, political and economic tracks, and preparing the agenda and topics of discussion for the dialogue.

Check out our full calendar on the web for a comprehensive listing of upcoming news events, national holidays and news triggers.

|

THE BIG STORY ABROAD-

Trump’s tumultuous week is still dominating the global headlines this morning: The Donald repeatedly pleaded the Fifth Amendment yesterday while giving testimony for a civil investigation by the New York attorney-general into his business dealings. While the former president has in the past mocked people for using the constitutional protection, yesterday he said he was forced into the move because of “an unfounded politically motivated Witch Hunt supported by lawyers, prosecutors and the Fake News Media.” The investigation is looking into whether the family has been using misleading financial information to inflate real estate values and obtain favorable loans and get tax breaks. This came just a few days after his Mar-a-Lago estate was raided by the FBI in what is thought to be related to a separate probe into whether he illegally removed records from the White House before leaving office last year. (AP | Reuters | NYT | Financial Times | Sky News | Politico)

MARKET WATCH-

Some better news on the US inflation front: Falling gas prices caused consumer prices in the US to cool more than expected in July, increasing optimism that inflation has now peaked. The CPI rose 8.5% y-o-y last month, down from 9.1% in June and below analysts’ expectations for 8.7% growth, data from the US Labor Department showed.

In context: Inflation remains incredibly high by historical standards and is far above the Federal Reserve’s 2% target.

So don’t expect the Fed to change tack anytime soon: One optimistic inflation reading does not a change in monetary policy make. One Fed official said last week that they need to see inflation falling in a “consistent, meaningful, and lasting way” before easing off the aggressive rate hikes. This view was reiterated by another two officials yesterday, who intimated that the latest inflation reading isn’t going to be sufficient for the Fed to change course. A growing number of analysts and economists are expecting the Fed to go ahead with its third successive 75-bps rate hike next month after a recent jobs report showed the US labor market remained tight in June.

The markets aren’t listening: US stocks soared yesterday in the hope that the Fed would soon reverse course and ease monetary policy. The Nasdaq, which just a few weeks ago was having one of its worst years on record, is now back in a bull market after surging 2.9% yesterday. The S&P 500 hit its highest level in three months, while the greenback had its worst day since the start of the pandemic in 2020.

The story’s getting a lot of international press attention: Reuters | The Financial Times | WSJ | NYT | WaPo.

Live music at Somabay: 2CELLOS. World-renowned and wildly popular cellist duo, 2CELLOS, are bringing the magic of music to Somabay on 18 November, 2022. Get ready for an unforgettable night of captivating performances and electric energy.

M&A WATCH

The Saudis have arrived

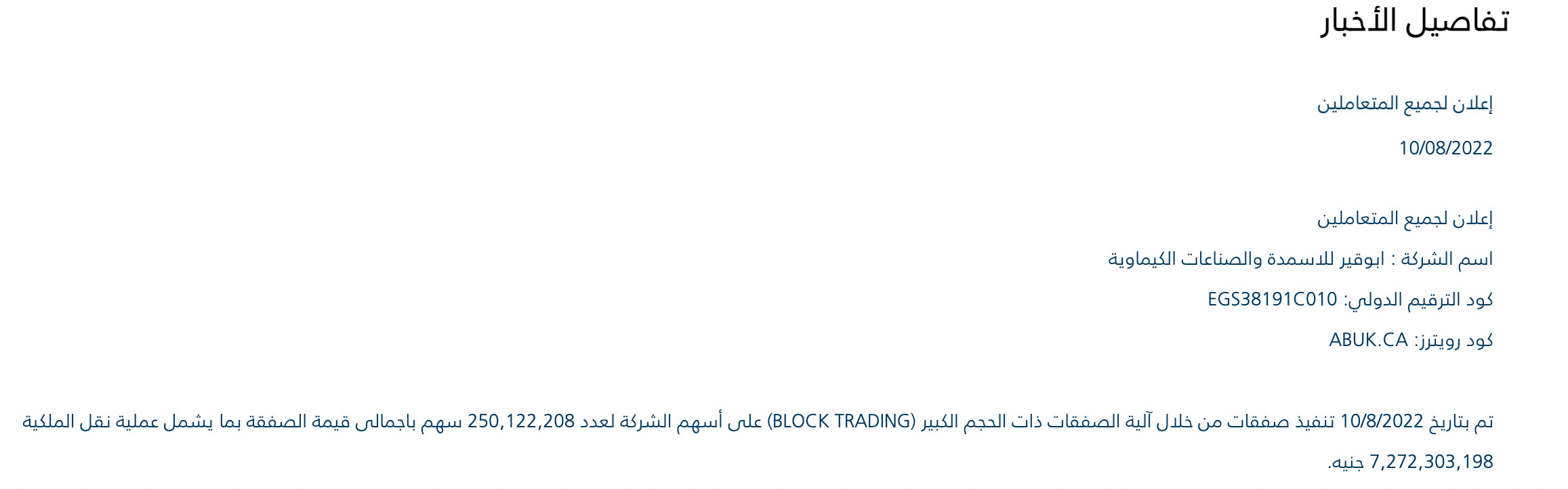

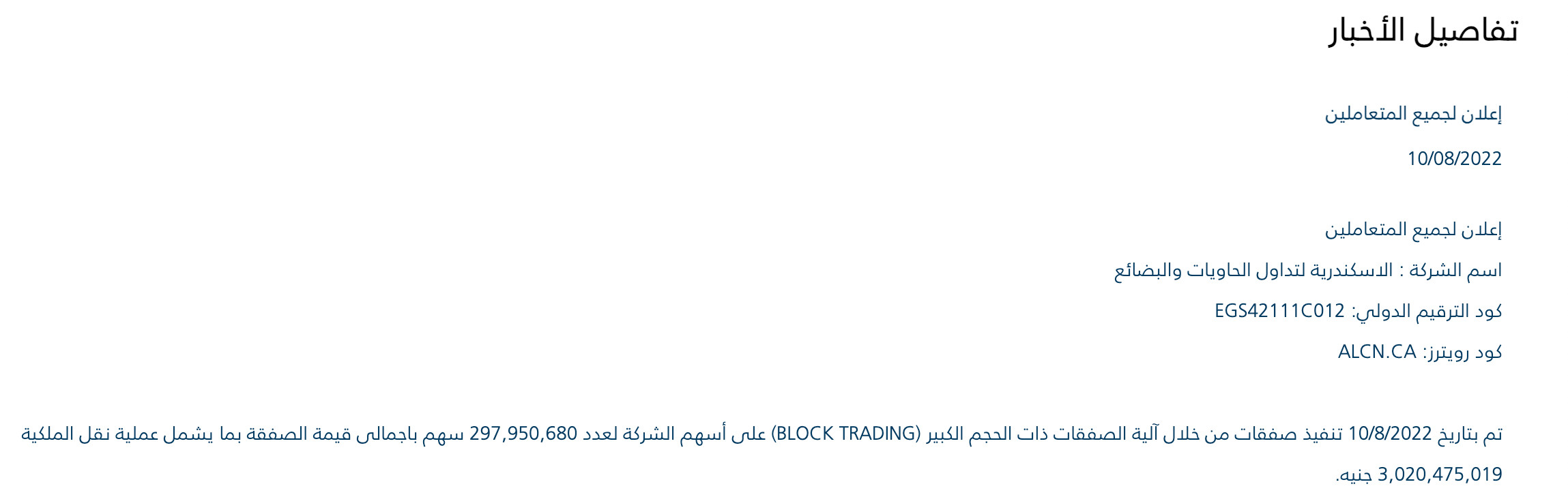

The Saudi sovereign wealth fund acquired minority stakes in four EGX-listed companies for USD 1.3 bn yesterday, the Planning Ministry said in a statement. The Saudi Egyptian Investment Company (SEIC), the newly-established Egypt investment arm of the Public Investment Fund, purchased shares in Misr Fertilizers Production Company (Mopco), Abu Qir Fertilizers, Alexandria Container and Cargo Handling, and E-Finance, according to the statement.

The breakdown: Market data yesterday showed that the SEIC bought stakes in:

- Mopco: A 25% stake was sold for EGP 7.15 bn, at an average price of EGP 123.96.

- Abu Qir: A 19.82% stake was sold for EGP 7.3 bn, at an average price of EGP 29.08.

- e-Finance: A 25% stake was sold for EGP 7.5 bn, at an average price of EGP 16.23.

- Alex Containers: A 20% stake was sold for EGP 3 bn, at an average price of EGP 10.14.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

The sellers: Informed sources told Al Mal that SEIC purchased the e-Finance shares from the National Investment Bank (NIB) and the Abu Qir stake from Al Ahly Capital Holding (the investment arm of state-owned National Bank of Egypt) and the Industrial Development Authority. The Holding Company for Maritime and Land Transport sold a 20% stake in Alex Containers, while Mopco saw NIB, Gasco and others selling, they added. The Finance Ministry and Misr Life were reported to be among the selling shareholders on Tuesday.

There’s more where that came from: The investments are the first of USD 10 bn pledged by the PIF earlier this year as part of Saudi efforts to support Egypt’s external position, which has been rocked by soaring commodity prices. The fund is looking to invest in the infrastructure, real estate, healthcare, financial services, food and agriculture, manufacturing and pharma sectors, and was reported this week to be closing in on the acquisition of United Bank.

Any of this sound familiar? Ths Saudi wealth fund isn’t the first this year to make a major round of purchases in publicly-traded firms. Abu Dhabi wealth fund ADQ purchased state-owned stakes in five companies for around USD 1.8 bn in April.

The Saudis have now bought into some of the same state-owned names as ADQ, which snapped up a 20% stake in Mopco, 21.5% of Abu Qir, and 32% of Alex Containers. ADQ also bought shares in CIB (17.5%) and Fawry (11.8%).

Shares were mixed over the news: Alex Containers rose 7.2% to EGP 10.1, while Abu Qir closed in green at 1.4% to EGP 24.2. Both e-Finance and Mopco ended in red, down 3.6% to EGP 15.5 and 0.4% to EGP 106, respectively.

What they said: The “transaction comes under the state’s plan to expand the ownership base and promote foreign direct investment,” Planning Minister Hala El Said said in the ministry statement. “It reflects foreign investors’ confidence in the Egyptian economy as one of the most promising strategic markets,” she said. “The acquisitions are in line with SEIC’s objective to invest in promising sectors,” the PIF-owned company said in a press release.

Privatization plans: All of this is part of the government's plans to attract USD 10 bn of investments a year over the next four years as it looks to open up more of the economy to the private sector.

Advisors: Our friends at EFG Hermes executed the transaction on the EGX for SEIC while Pharos Holding executed the transaction on behalf of the state-affiliated sellers, Al Mal reports citing anonymous sources. Matouk Bassiouny & Hennawy was legal advisor to the SEIC, while Baker McKenzie was advisor to the state entities, Al Mal reported.

There’s more to come from the KSA and its neighbors: Several Saudi companies in June signed agreements that will see them invest USD 7.7 bn in Egypt, with the KSA at the time saying it intends to “lead” USD 30 bn in investments here. Gulf state neighbors have pledged more than USD 22 bn in total to support the economy amid the fallout from the crisis in Ukraine.

The news is getting attention in the global press: Bloomberg | Reuters.

M&A WATCH

The first half of the year was good for M&A in Egypt

Egypt has been a MENA M&A hotspot so far in 2022: Egypt recorded 65 M&A transactions worth USD 3.2 bn in the first six months of the year, making it the second-largest M&A destination in the region by value and dealcount, according to a report from EY.

2022 > 2021: This is more than triple the M&A activity seen in 1H 2021 and marks Egypt’s emergence as a “major investment destination,” EY said. The surge was driven mainly by “favorable government initiatives, including granting a special license to foreign investors,” it added.

Egypt has ADQ to thank: Abu Dhabi wealth fund ADQ’s USD 1.8 bn investment in several publicly-traded companies in April accounted for more than half of the capital raised in M&A transactions during the period.

Expect 2H to look a lot like 1H with the Saudi sovereign wealth fund’s announcement yesterday kicking off a USD 10 bn investment spree.

Across the region: The MENA region saw USD 42.6 bn worth of M&A transactions during the six-month period, EY said. Dealcount rose 12% y-o-y to 359, as surging oil prices offset the market volatility that caused a fall in dealmaking in other parts of the world.

Number one in the region: The UAE accounted for a third of the region’s M&A activity during 1H, recording 105 transactions worth USD 14.2 bn.

Rounding out the top five: Saudi Arabia (USD 2.8 bn), Morocco (USD 1.8 bn) and Oman (USD 700 mn).

The biggest sectors targeted in M&A transactions for the region in the first half of the year were transportation, consumer products, telecommunications, real estate and power and utilities.

ECONOMY

Inflation hits new three-year high in July

Inflation resumed its upward trend in July, reaching a fresh three-year high on the back of higher food and fuel prices, according to official figures from state statistics agency Capmas (pdf). Consumer prices in urban areas rose 13.6% y-o-y in July, up from 13.2% in June when prices unexpectedly cooled after months of rising inflation triggered by the war in Ukraine and the devaluation of the EGP. Urban inflation increased 1.3% month-on-month, after declining 0.1% m-o-m in June.

Food + fuel were the culprits: Food and beverage prices — the biggest component of the basket used to measure inflation — rose again in July after falling back the month before. Prices rose 22.4% y-o-y and were up 0.5% from June after falling almost 2% m-o-m in June. The decision to raise fuel prices last month also fanned further inflation, pushing transport costs up 17% y-o-y and more than 10% from June. Housing, electricity, water and fuel costs also rose 5.2% y–o-y and 0.1% m-o-m.

Core inflation hit a 4.5-year high: Core inflation, which strips out volatile items such as food and fuel, climbed 15.6% on an annual basis in July, up from 14.6% in May, according to central bank data (pdf). This is its highest level since December 2017.

Inflation came in higher than some analysts’ expectations: The median average forecast in a Reuters poll of 14 economists was for inflation to rise 13.2%.

Other analysts expected worse: Al Ahly Pharos had forecast inflation to clock in at 15%, and said that weaker-than-expected food and fuel price growth was behind the softer figures in a note yesterday.

The good news: Supply-side factors fueling inflation around the world have eased in recent weeks. Global food prices have fallen for four consecutive months and were helped last month with the breakthrough agreement between Ukraine and Russia to resume Ukrainian grain exports via the Black Sea. Oil prices have also fallen significantly and are now at pre-Ukraine war lows and edging towards USD 90 a barrel.

But we may not have reached the peak: “Inflationary pressures continue to build as a result of cumulative pressures on the local currency, which is expected to weaken further,” economist Mona Bedair told Enterprise. She also expects fuel prices to rise again later this year and said that continued uncertainties over global energy prices, supply chains and shipping costs will continue to present risks going forward. CI Capital also expects inflation to continue to rise on the back of the train and metro fare hikes being introduced this month and the continued impact of higher fuel costs. Beltone Financial expects inflation to peak at 16.5% this month and average 15.5% in 3Q, macro director Alia Mamdouh wrote in a note yesterday.

EGP + energy are set to be the drivers looking forward: Headline inflation will accelerate over the coming months as the EGP is expected to further weaken, “and fuel prices are likely to be hiked further to reflect high global energy prices,” James Swanston, MENA economist at Capital Economics, wrote in a note. Capital Economics is now anticipating inflation to peak at c. 18% in 4Q 2022.

What does this mean for interest rates? Al Ahly Pharos and Beltone expect the central bank to leave rates on hold when it meets next Thursday. The easing of global supply-side pressures, the government’s surging interest bill, and the continued bearish sentiment among foreign investors towards emerging markets are all reasons why policymakers will choose to keep rates at their current levels, Al Ahly Pharos economist Esraa Ahmed wrote yesterday.

On the other hand, Capital Economics expects the CBE to act preemptively against further rises in inflation and hike rates next week. “We have penciled in a total of 150 bps of hikes, taking the overnight deposit rate to 12.75%, by the end of this year,” Swanston said. Economist Hany Genena expects the CBE to raise interest rates next Thursday in anticipation of another large rate hike by the US Federal Reserve in September, he tells Salet El Tahrir (watch, runtime: 10:50). The Fed has embarked on its most aggressive tightening cycle in decades this year, putting further pressure on Egypt’s borrowing costs.

The CBE has hiked rates by 300 bps since March under efforts to tame inflation and curb outflows. The Monetary Policy Committee kept rates unchanged in its latest meeting in June. The central bank is currently targeting 7% (±2%) inflation by the end of 2022, but has said it will “temporarily tolerate” the elevated annual headline inflation rate relative to its target until 2023.

Egypt’s inflation story is getting attention internationally: Bloomberg | Reuters.

INVESTMENT WATCH

The Mogamma will become the Cairo House Hotel by the end of 2024

The Mogamma’s face-lift could be finished in 2024: The consortium of investors redeveloping the Mogamma into a hotel will finish construction by the end of 2024, Bloomberg Asharq reported Tuesday. This came from Randall Langer, chairman of MENA-focused US investment firm Global Ventures, who together with Oxford Capital and the UAE’s Al Otaiba Investment in December won the EGP 3.5 bn contract to revamp the administrative building in downtown Cairo.

Introducing the Cairo House Hotel: The Mogamma will be transformed into a new 450-room, five-star hotel. It will have more than 85k sqm of meeting and events spaces, several entertainment venues and restaurants, and feature the capital’s largest rooftop venue. The consortium signed the contract to redevelop the Mogamma with the Sovereign Fund of Egypt (SFE) and the Planning Ministry in December. The investors will manage the redevelopment of the complex and operate it once it is complete.

It’s costing more than originally planned: The development is now expected to cost around USD 240 mn, Langer told Asharq. The consortium will directly finance about 35% of the project, while the remaining 65% will be raised from banks, he added. The consortium is currently in talks with several local banks and is planning to announce the results of the negotiations within a month, he said, declining to identify the potential lenders.

Contractors have been hired: The consortium has contracted the Middle East-focused Consolidated Contractors Company (CCC) as its general contractor, managing director of CCC’s North Africa division, Mohamed Tarek, told CNBC Arabia (watch, runtime: 2:50). RMC Engineering and project management firm Chrome are also onboard.

We could see more activity from CCC in Egypt: The project comes as part of Lebanon-based CCC’s plans to expand in Egypt, Tarek told CNBC Arabia. The company’s current portfolio in Egypt is valued at USD 2 bn.

INVESTMENT WATCH

Swvl to sell USD 20 mn in fresh stock via private placement

Cairo-born mass transport app Swvl has agreed to sell new shares to an institutional investor, giving it an important cash infusion as it restructures costs in a bid to stem widening losses. The company hopes to raise USD 20 mn with the sale of c.12.1 mn shares, which will be bought by the investor for USD 1.65 apiece at a private placement expected to close on Friday, it said in a statement (pdf) yesterday.

That’s not all: Under the agreement, the investor has the ability to purchase another c.18.2 mn shares over the next five years at the same price. If these “warrants” are exercised, Swvl will receive a further USD 30 mn in investment.

SOUND SMART- Simply put, warrants give investors the right to purchase shares at a certain price at a specific time in the future. All warrants have expiration dates: if the investor exercises the right within the time frame, they immediately purchase the stock at the agreed price, but waiting until after the expiration date will see the warrant expire.

Swvl needs the cash: The Nasdaq-listed company has embarked on dramatic cost-cutting measures this year to try and stay on track to its goal of becoming cashflow-positive in 2023. The firm has warned that losses will almost double this year, and has slashed its headcount by a third, cut executive pay and eliminated a number of unprofitable routes to support its finances.

Market reax: Swvl’s shares fell 16.4% yesterday to close at a near-record low of USD 1.53. The company’s shares have fallen 84.7% since it debuted on the Nasdaq in April via a SPAC merger.

A MESSAGE FROM

![]()

The Coca-Cola Company launched a more sustainable product by replacing the memorable green Sprite bottle with a transparent (clear PET) one. The Coca-Cola Company, with its World Without Waste program, aims to help in collecting and recycling the same number of bottles for every bottle sold, leading to plastic neutrality by 2030, as well as to use up to 50% of recycled materials in the bottles and cans by the same year. Learn more here.

M&A WATCH

The bidding war for Pachin is heating up

Saybad ups its offer for Pachin: Saybad Industrial Investment has increased its offer for Paint and Chemical Industries (Pachin) to EGP 16.50-18.75 per share, it said in an EGX disclosure (pdf). The new offer would value the EGX-listed company at up to EGP 450 mn, according to our calculations. The upper end of the price range is 14% higher than its initial EGP 16-16.50 offer, which was rejected by Pachin for being too low.

The bidding war is now in full swing: The top end of Saybad’s revised offer comes in above the maximum bid that Universal Building Materials and Chemicals (Sipes) put in for Pachin earlier this week. Sipes is offering to purchase at least 60% of the state-owned company for between EGP 17.50-EGP 18.50 per share.

Market reax: Pachin’s shares jumped 1.65% on the news to close at EGP 17.22 yesterday.

Part of the government’s privatization plans: The bids come as the state looks to reduce its involvement in or exit certain industries to make way for the private sector. Pachin is currently approximately 54% owned by state-owned companies and banks.

ADVISORS- Catalyst Partners is acting as Pachin's financial advisor. Adsero–Raji Soliman & Associates is the firm’s legal advisor.

IN OTHER M&A NEWS-

Oriental Weavers is exiting the Chinese market after its board agreed to accept an offer to sell its Chinese unit to an unnamed buyer, it said in an EGX disclosure (pdf). The company has been considering the offer since last year, weighing its options between selling or liquidating its Chinese subsidiary.

STARTUP WATCH

Convertedin + Sharwa close funding rounds

Marketing startup Convertedin has closed a USD 3 mn seed round, it said in a press release picked up by Zawya. The round was led by Saudi tech investor Merak Capital with participation from 500 Global and MSAS.

Marketing for e-commerce: Founded in 2019 by Mohamed Fergany (LinkedIn), Mohamed Atef (LinkedIn) and Mustafa Raslan (LinkedIn), Convertedin operates a marketing platform targeted at e-commerce companies. The company says its data-driven services help businesses double their return on ad spend and cut customer acquisition costs by 40%. It is working with local and multinational companies in the Middle East, Africa and South America, and has offices in Saudi Arabia and Brazil in addition to its Egyptian HQ.

What’s next: The company will use the funding for hiring and platform development, according to the statement. It also wants to expand across MENA and Latin America.

IN OTHER STARTUP NEWS- Social commerce startup Sharwa raised USD 2 mn in a pre-seed funding round co-led by Nuwa Capital and Hambro Perks’ Oryx Fund, with participation from several strategic angel investors, according to a press release picked up by Wamda.

Sharwa gets you cheaper household goods: Founded earlier this year by Aladdin Shalaby (LinkedIn), Hassan Elshourbagi (LinkedIn) and Mohamed Hanafy (LinkedIn), Sharwa is an e-commerce platform that allows customers to club together and purchase household items at wholesale prices. The startup was launched as an answer to spiraling inflation in Egypt, according to Sharwa’s website. The platform — which currently has “tens of thousands” of customers — is operating in Cairo and “nearby areas,” according to the press release.

Where the money’s going: The funds will be used to expand the team and develop the online platform. The company also has ambitions to launch nationwide across Egypt and process hundreds of thousands of orders in the next 12 months.

KUDOS

Global Banking and Finance Review names best Egyptian banks + NBFIs of the year: The Global Banking and Finance Review has released its 2022 list of top-ranked Egyptian banks and non-banking financial institutions. Check out the full list here.

Five Egyptian fintech companies have been featured on Forbes’ top 25 fintech companies for 2022:

- Financial services provider Aman: Founded in 2015 by Mohamed Wahby (LinkedIn) and Hazem Moghazi (LinkedIn), the company is Raya Holding’s non-banking financial services outfit.

- E-payment platform Fawry, which was founded in 2008 by Ashraf Sabry (LinkedIn). Abu Dhabi sovereign wealth fund ADQ purchased an 11.8% stake in the company in April.

- Super app MNT-Halan, which was set up in 2018 by Mounir Nakhla and Ahmed Mohsen (LinkedIn). It is the product of Netherlands-based payments company MNT entering into a share swap agreement with Egyptian fintech / delivery / ride-hailing company Halan.

- E-payment platform Paymob, which was founded in 2015 by Islam Shawky, Alain El Hajj (LinkedIn) and Mostafa Menessy (LinkedIn). The company is responsible for Egypt’s largest funding round so far this year, raising USD 50 mn in a series B round in May.

- BNPL platform valU: The EFG Hermes consumer finance subsidiary was founded in 2017 by Walid Hassouna (LinkedIn). Last we heard the company is looking to make its EGX debut sometime within the coming two years.

LAST NIGHT’S TALK SHOWS

The government’s plan to cut back on public electricity consumption was still dominating the airwaves last night: Prime Minister Moustafa Madbouly’s meeting with the cabinet yesterday saw them discuss the measures he plans to implement to cut electricity consumption in a bid to redirect more natural gas towards exports got airtime on Masaa DMC (watch, runtime: 2:39 | 4:22) and Al Hayah Al Youm (watch, runtime: 7:26). Ala Mas’ouleety’s Ahmed Moussa was particularly aggrieved about the idea of darkening Tahrir Square at night and called on ministers to exclude hotels and the tourist industry from the measures (watch, runtime: 6:59).

Yesterday’s inflation figures also got some attention: As we noted above, economist Hany Genena phoned into Salet El Tahrir (watch, runtime: 10:50) to give his take on the figures and how the central bank will likely respond at its policy meeting next week.

Does Egypt actually have ambitions to enter the semiconductor fabrication business? Apparently so, according to former Oil Minister Osama Kamal, who told Ala Mas’ouleety that the country is working on projects in the sector (watch, runtime: 7:25). He declined to provide any details but suggested that Egypt’s plentiful supply of sand makes it a good place to produce silicon chips.

This publication is proudly sponsored by

EGYPT IN THE NEWS

It’s another slow morning in the pages of the foreign press: AFP reports that a male student has been arrested on charges of murdering a female student after she rejected his advances. This is the second woman to be killed at an Egyptian university in two months after student Nayera Ashraf was stabbed to death on the campus of Mansoura University.

ALSO ON OUR RADAR

e-Aswaaq has rolled out its online ticketing platform to archeological sites: You can now buy tickets online for 29 tourist attractions in Egypt through the online portal run by e-Aswaaq, the e-commerce and tourism arm of state fintech player e-Finance, the company said in a press release (pdf). The platform allows you to purchase barcode-enabled tickets that can then be used directly through your phone at electronic gateways that the company installed at each of the sites, according to the statement.

This is ahead of schedule: The company had been looking to finish upgrading ticketing systems and complete the rollout of the portal for 30 archeological sites by the end of the year, after rolling it out at the Giza Pyramids and a number of other museums last year.

Food exports rose 2.4% y-o-y to USD 2.17 bn in 1H 2022, up from USD 2.12 bn last year, according to new figures from the Food Export Council. Arab countries were the biggest buyers, accounting for half of all exports during the period. EU countries came in second, importing USD 427 mn worth of food (20%), while the US accounted for 7% and non-Arab African countries 6%.

Other things we’re keeping an eye on this morning:

- Prime Minister Moustafa Madbouly directed each governorate and major city to establish a central park and plant trees along new roads nationwide under the plan to plant 100 mn trees. (Statement)

- EFG Hermes’ e-payments subsidiary PayTabs is partnering with Waffarha to allow users of the savings platform to make online payments through PayTabs. (Statement, pdf)

- The Health Ministry is getting a USD 11.2 mn grant from the UN Development Programme to make HIV and tuberculosis treatments more accessible and mitigate the impact of covid. (MENA)

PLANET FINANCE

Powered by

The threat of greenwashing accusations is weighing on ESG debt markets: More bond issuers are concerned that tapping the ESG debt market will invite increased scrutiny and PR nightmares related to accusations of greenwashing, Bloomberg reports. While many issuers have found ESG bonds attractive because of their lower borrowing costs, “there’s a number of issuers that are reconsidering the cost benefit trade-off,” Jason Taylor, managing director for sustainability advisory and finance at National Bank of Canada told the business information service. After a number of recent PR headaches for companies like Chanel and the UK supermarket Tesco, who either failed to meet their sustainability targets or were using minuscule metrics, more asset managers — including Goldman Sachs — are getting pickier with ESG pitches.

“Greenwashing across the board is going to be more and more scrutinized as we head into 2030,” Taylor said. Green bond issuers are also beginning to overlook longer-tenured ESG debt issuances because of the fast-changing nature of the regulatory landscape for the industry. “Standards are also developing at a faster rate so those gray zones are dissipating more and more,” Taylor said. “Over time, the market’s going to tighten up on its own.”

EARNINGS WATCH- Disney’s streaming subscriber numbers are now bigger than Netflix: Disney reported (pdf) a 26% y-o-y jump in revenues to USD 21.5 bn in 2Q 2022, easily beating analysts’ estimates of USD 20.9 bn as new spending at its theme parks rose and its streaming service Disney+ saw larger-than-expected subscriber growth. The company added 14.4 mn Disney+ subscribers during the quarter, taking total subscriptions across all its streaming services to 221 mn, above Netflix’s 220.7 mn. Disney shares rose almost 7% in after-hours trading.

|

|

EGX30 |

9,965 |

0.0% (YTD: -16.6%) |

|

|

USD (CBE) |

Buy 19.09 |

Sell 19.20 |

|

|

USD at CIB |

Buy 19.12 |

Sell 19.18 |

|

|

Interest rates CBE |

11.25% deposit |

12.25% lending |

|

|

Tadawul |

12,431 |

+0.8% (YTD: +10.2%) |

|

|

ADX |

10,198 |

+0.8% (YTD: +20.1%) |

|

|

DFM |

3,394 |

+0.3% (YTD: +6.2%) |

|

|

S&P 500 |

4,210 |

+2.1% (YTD: -11.7%) |

|

|

FTSE 100 |

7,507 |

+0.3% (YTD: +1.7%) |

|

|

Euro Stoxx 50 |

3,749 |

+0.9% (YTD: -12.8%) |

|

|

Brent crude |

USD 97.08 |

+0.8% |

|

|

Natural gas (Nymex) |

USD 8.20 |

+4.7% |

|

|

Gold |

USD 1,813.70 |

+0.1% |

|

|

BTC |

USD 23,981 |

+3.4% (YTD: -48.2%) |

THE CLOSING BELL-

The EGX30 was effectively flat at yesterday’s close on turnover of EGP 1.01 bn (19.1% above the 90-day average). Regional investors were net buyers. The index is down 16.6% YTD.

In the green: Alexandria Container and Cargo Handling (+7.2%), CIRA (+4.7%) and Abu Qir Fertilizers (+1.4%).

In the red: e-Finance (-3.6%), Cleopatra Hospitals (-3.3%) and Palm Hills (-2.5%).

Asian markets are picking up where Wall Street left off yesterday and are seeing large gains this morning as investors bet that cooling US inflation last month will persuade the Federal Reserve to temper its aggressive tightening cycle. Shares are on course to continue rallying in Europe and the US today, according to stock futures.

CALENDAR

OUR CALENDAR APPEARS in two sections:

- Events with specific dates or months are right here up top

- Events happening in a quarter or other range of time with no specific date / month appear at the bottom of the calendar.

AUGUST

Late July-14 August: 2Q2022 earnings season.

August: Work to extend the capacity of the Egypt-Sudan electricity interconnection to 600 MW to be completed.

August: Sharm El Sheikh will host the African Sumo Championship.

11 August (Thursday): The government hosts public consultations on its state ownership policy document with experts and think tanks.

12 August (Friday): Swvl to sell USD 20 mn in stock to a US investor in a private placement.

14 August (Sunday): Retail portion of Ghazl El Mahalla IPO ends.

14 August (Sunday): The government hosts public consultations on its state ownership policy document with finance and ins. players.

16 August (Tuesday): The government hosts public consultations on its state ownership policy document with wood manufacturers.

16 August (Tuesday): MNHD’s general assembly meeting to decide whether to allow SODIC to go ahead with due diligence on its takeover bid.

18 August (Thursday): The government hosts public consultations on its state ownership policy document with experts and think tanks.

18 August (Thursday): Central Bank of Egypt’s Monetary Policy Committee meeting.

23 August (Tuesday): The government hosts public consultations on its state ownership policy document with chemical producers.

25 August (Thursday): Second Egypt and UN-led regional climate roundtable ahead of COP27, Bangkok, Thailand.

25 August (Thursday): The government hosts public consultations on its state ownership policy document with experts and think tanks.

25-27 August (Thursday-Saturday): Jackson Hole Economic Symposium.

27 August (Saturday): The National Dialogue board of trustees holds its fifth meeting, which will set the agenda for the dialogue and choose rapporteurs for the involved committees.

28 August (Sunday): The government hosts public consultations on its state ownership policy document with mining and petroleum refining players.

30 August (Tuesday): The government hosts public consultations on its state ownership policy document with minerals players.

31 August (Wednesday): Late tax payment deadline.

31 August (Wednesday): Deadline for qualifying companies to submit offers to manage and operate a soon-to-be-established state company for EV charging stations.

31 August (Wednesday): Submission deadline for fall 2022 cycle of EGBank’s Mint Incubator.

31 August (Wednesday): Beltone convenes its general assembly to restructure the board following the change of ownership.

SEPTEMBER

September: Naval Power, Egypt’s first naval defense expo

September: Central Bank of Egypt’s Innovation and Financial Technology Center to launch incubator for 25 fintech startups.

September: Egyptian-German Joint Economic Committee.

September: A delegation from Germany’s Aldi will visit Egypt to look at potential investments.

September: Government to launch an international promotional campaign for Egyptian tourism.

September: Egypt will host the second edition of the Egypt-International Cooperation Forum (ICF).

1 September (Thursday): Credit hikes for ration card holders will come into effect.

1 September (Thursday): The government hosts public consultations on its state ownership policy document with experts and think tanks.

1-2 September (Thursday-Friday): Third Egypt and UN-led regional climate roundtable ahead of COP27, Santiago, Chile.

4 September (Sunday): The government hosts public consultations on its state ownership policy document with electricity players.

6 September (Tuesday): The government hosts public consultations on its state ownership policy document with building and construction players.

6-9 September (Tuesday-Friday): Gate Travel Expo 2022, El Qubba Palace, Cairo.

7-9 September (Wednesday-Friday): African Finance Ministers to meet in Cairo to coordinate an African-led position during COP27.

8 September (Thursday): European Central Bank monetary policy meeting.

8 September (Thursday): The government hosts public consultations on its state ownership policy document with experts and think tanks.

11 September (Sunday): The government hosts public consultations on its state ownership policy document with accommodation and food services players.

13 September (Tuesday): The government hosts public consultations on its state ownership policy document with sports industry players.

11-13 September (Tuesday-Thursday): Environment and Development Forum (EDF), InterContinental City Stars, Cairo.

15 September (Thursday): The government hosts public consultations on its state ownership policy document with water and sewage utilities players.

15 September (Thursday): Fourth Egypt and UN-led regional climate roundtable ahead of COP27, Beirut, Lebanon.

18 September (Sunday): Deadline for brokerage firms, asset managers and financial advisors to register with the Egyptian Securities Federation.

20 September (Tuesday): Fifth Egypt and UN-led regional climate roundtable ahead of COP27, Geneva, Switzerland.

20-21 September (Tuesday-Wednesday): Federal Reserve interest rate meeting.

22 September (Thursday): Central Bank of Egypt’s Monetary Policy Committee meeting.

26–27 September (Monday-Tuesday): The Africa Women Innovation and Entrepreneurship Forum (AWIEF) at the Cairo Marriott Hotel.

27-29 September (Tuesday-Thursday): Africa Renewables Investment Summit (ARIS), Cape Town, South Africa.

OCTOBER

October: House of Representatives reconvenes after summer recess

October: Air Sphinx, EgyptAir’s low-cost subsidiary to commence operations.

October: Fuel pricing committee meets to decide quarterly fuel prices.

1 October (Saturday): Use of Nafeza becomes compulsory for air freight.

1 October (Saturday): 2022- 2023 academic year begins for public universities.

6 October (Thursday): Armed Forces Day, national holiday.

8 October (Saturday): Prophet Muhammad’s birthday, national holiday.

10-16 October (Monday-Sunday): World Bank and IMF annual meetings chaired by CBE Governor Tarek Amer, Washington, DC.

16-19 October (Sunday-Wednesday): Cairo Water Week 2022, Nile Ritz Carlton, Cairo.

18-20 October (Tuesday-Thursday): Mediterranean Offshore Conference, Alexandria.

27 October (Thursday): European Central Bank monetary policy meeting.

Late October-14 November: 3Q2022 earnings season.

NOVEMBER

1-2 November (Tuesday-Wednesday): Federal Reserve interest rate meeting.

3 November (Thursday): Central Bank of Egypt’s Monetary Policy Committee meeting.

3-5 November (Thursday-Saturday): Egypt Fashion Week.

4-6 November (Friday-Sunday): Autotech auto exhibition, Cairo International Exhibition and Convention Center.

6-18 November (Sunday-Friday): Egypt will host COP27 in Sharm El Sheikh.

7 November (Monday): The inauguration of the first line of the high-speed rail.

7-13 November (Mon-Sun): The International University Sports Federation (FISU) World University Squash Championships, New Giza.

21 November-18 December (Monday-Sunday): 2022 Fifa World Cup, Qatar.

DECEMBER

13-14 December (Tuesday-Wednesday): Federal Reserve interest rate meeting.

13-15 December (Tuesday-Thursday): US-Africa Leaders Summit.

15 December (Thursday): European Central Bank monetary policy meeting.

22 December (Thursday): Central Bank of Egypt’s Monetary Policy Committee meeting.

December: The Sixth of October dry port will begin operations.

JANUARY 2023

January: EGX-listed companies and non-bank lenders will submit ESG reports for the first time.

January: Fuel pricing committee meets to decide quarterly fuel prices.

1 January (Sunday): Residential electricity bills are set to rise as per the government’s six-year roadmap (pdf) to restructure electricity prices by 2025.

7 January (Saturday): Coptic Christmas.

25 January (Wednesday): 25 January revolution anniversary / Police Day.

26 January (Thursday): National holiday in observance of 25 January revolution anniversary / Police Day.

FEBRUARY 2023

11 February (Saturday): Second semester of 2022-2023 academic year begins for public universities.

13-15 February (Monday-Wednesday): The Egypt Petroleum Show (Egyps), Egypt International Exhibition Center, Cairo.

MARCH 2023

March: 4Q2022 earnings season.

23 March (Wednesday) — First day of Ramadan (TBC). Maghreb will be at 6:08pm CLT.

APRIL 2023

17 April (Monday): Sham El Nessim.

22 April (Saturday): Eid El Fitr (TBC).

25 April (Tuesday): Sinai Liberation Day.

27 April (Thursday): National holiday in observance of Sinai Liberation Day (TBC).

Late April – 15 May: 1Q2023 earnings season.

MAY 2023

1 May (Monday): Labor Day.

4 May (Thursday) National holiday in observance of Labor Day (TBC).

22-26 May (Monday-Friday): Egypt will host the African Development Bank (AfDB) annual meetings in Sharm El Sheikh.

JUNE 2023

28 June-2 July (Wednesday-Sunday): Eid El Adha (TBC).

30 June (Friday): June 30 Revolution Day.

JULY 2023

18 July (Tuesday): Islamic New Year.

20 July (Thursday): National holiday in observance of Islamic New Year (TBC).

23 July (Sunday): Revolution Day.

27 July (Thursday): National holiday in observance of Revolution Day.

Late July-14 August: 2Q2023 earnings season.

SEPTEMBER 2023

26 September (Tuesday): Prophet Muhammad’s birthday (TBC).

28 September (Thursday): National holiday in observance of Prophet Muhammad’s birthday (TBC).

OCTOBER 2023

6 October (Friday): Armed Forces Day.

Late October-14 November: 3Q2023 earnings season.

EVENTS WITH NO SET DATE

2H 2022: The inauguration of the Grand Egyptian Museum.

2H 2022: IEF-IGU Ministerial Gas Forum, Egypt. Date + location TBA.

2H 2022: The government will have vaccinated 70% of the population.

3Q 2022: Ayady’s consumer financing arm, The Egyptian Company for Consumer Finance Services, to release its first financing product.

3Q 2022: Swvl to close acquisition of Urbvan Mobility.

4Q 2022: Infinity + Africa Finance Corporation to close acquisition of Lekela Power.

End of 2022: Decent Life first phase scheduled for completion.

End of 2022: e-Aswaaq’s tourism platform will complete the roll out of its ticketing and online booking portal across Egypt.

2023: Egypt will host the Asian Infrastructure Investment Bank’s Annual Meeting of the Board of Governors in 2023.

1Q 2023: Adnoc Distribution’s acquisition of 50% of TotalEnergies Egypt to close.

**Note to readers: Some national holidays may appear twice above. Since 2020, Egypt has observed most mid-week holidays on Thursdays regardless of the day on which they fall and may also move those days to Sundays. We distinguish above between the actual holiday and its observance.

Enterprise is a daily publication of Enterprise Ventures LLC, an Egyptian limited liability company (commercial register 83594), and a subsidiary of Inktank Communications. Summaries are intended for guidance only and are provided on an as-is basis; kindly refer to the source article in its original language prior to undertaking any action. Neither Enterprise Ventures nor its staff assume any responsibility or liability for the accuracy of the information contained in this publication, whether in the form of summaries or analysis. © 2022 Enterprise Ventures LLC.

Enterprise is available without charge thanks to the generous support of HSBC Egypt (tax ID: 204-901-715), the leading corporate and retail lender in Egypt; EFG Hermes (tax ID: 200-178-385), the leading financial services corporation in frontier emerging markets; SODIC (tax ID: 212-168-002), a leading Egyptian real estate developer; SomaBay (tax ID: 204-903-300), our Red Sea holiday partner; Infinity (tax ID: 474-939-359), the ultimate way to power cities, industries, and homes directly from nature right here in Egypt; CIRA (tax ID: 200-069-608), the leading providers of K-12 and higher level education in Egypt; Orascom Construction (tax ID: 229-988-806), the leading construction and engineering company building infrastructure in Egypt and abroad; Moharram & Partners (tax ID: 616-112-459), the leading public policy and government affairs partner; Palm Hills Developments (tax ID: 432-737-014), a leading developer of commercial and residential properties; Mashreq (tax ID: 204-898-862), the MENA region’s leading homegrown personal and digital bank; Industrial Development Group (IDG) (tax ID:266-965-253), the leading builder of industrial parks in Egypt; Hassan Allam Properties (tax ID: 553-096-567), one of Egypt’s most prominent and leading builders; and Saleh, Barsoum & Abdel Aziz (tax ID: 220-002-827), the leading audit, tax and accounting firm in Egypt.