Egypt’s renewable energy capacity is on track to grow 65% by 2027, says IEA

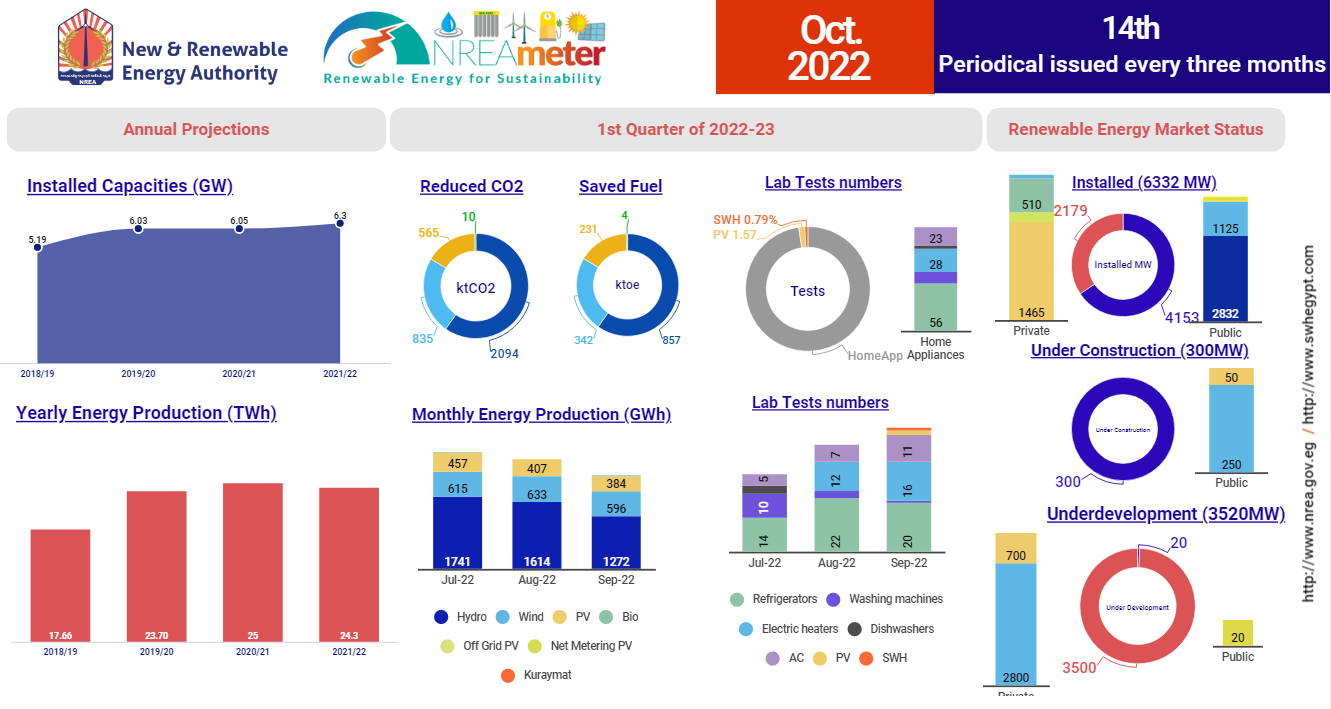

A new report brings promising news on renewables growth — here and across the MENA region: Egypt’s renewable energy capacity is on track to grow some 65% by 2027, thanks primarily to new offshore wind projects, according to the International Energy Agency’s (IEA) annual report (pdf) on the global renewables industry. We’re set to add some 4.1 GW of renewable capacity over the next five years, the IEA says — bringing total capacity to 10.4 GW from the 6.3 GW currently installed, according to the most recent data from the New and Renewable Energy Authority (NREA).

{kind=link}

Egypt will account for almost a quarter of total renewables capacity in the MENA region by 2027: Rapid growth in wind and solar will see renewables capacity across MENA rise even faster than in Egypt alone. Capacity is set to triple to reach 45 GW in five years’ time, the IEA says. The regional outlook marks a significant upwards revision from the IEA’s 2021 report, when it estimated that the region would double its capacity to reach 32 GW between 2021 and 2026.

The caveat: New renewables growth in Egypt appears to be slowing, per the IEA…: “Uncertainty over the government’s plans for state-owned utility projects and delays in the competitive auction scheme have caused this year’s forecast to be revised downwards” for Egypt, the report reads. In its 2021 report, the IEA predicted that we would add some 4 GW of capacity over five years to reach 10.1 GW by 2026. The report points to the 100-MW solar tender that was canceled back in 2020 as an example — and notes that of the 1-GW worth of state-owned renewables projects announced in 2017, only 26 MW has so far been commissioned.

…Meaning some of our neighbors are set to surpass us in the next five years: In 2021, Egypt was fourth in MENA for the amount of new renewable capacity it was expected to add over the following five years, behind the UAE, Saudi Arabia and Morocco. This year, the IEA expects Saudi, the UAE, Israel, Oman, and Morocco to add more renewable energy capacity than us by 2027. Egypt and these five countries will account for some 85% of renewable energy growth in the region, the report says. We took a closer look over the summer at how our regional neighbors could overtake us on solar and wind power this decade.

BUT- This report doesn’t include the raft of fresh wind projects signed at COP27. A flurry of initial agreements for mega wind projects were signed between private sector developers and the government during November’s climate summit in Sharm El Sheikh. The agreements are set to bring up to 29.5 GW of fresh wind power online.That includes two massive 10-GW wind farms that are set to among the largest in the world: one from our friends at Infinity Power and Hassan Allam Utilities together with long-time partner Masdar; and the other from Saudi renewable energy developer ACWA Power. These projects are all in the earliest stages of implementation, pending feasibility studies and final contracts — meaning we don’t yet know which of them will ultimately come to fruition or how long it could take to get them online.

A change in strategy: Tenders for utility-scale projects have been few and far between in recent years, the IEA notes. Instead, “most of the expansion” the agency is expecting by 2027 will come through “unsolicited bilateral IPP [independent power producer] contracts negotiated with the state utility.” That rings true as far as the fresh agreements signed at COP, all of which were negotiated directly between the authorities and consortiums including local and international renewables players.

Nevertheless, solar tenders could make a comeback on the back of the enthusiasm generated at the summit: The NREA is reportedly planning to issue at least one tender in the new year as it looks to employ the 350 MW of unused capacity at our mega Benban solar park, with potential financing coming from the European Bank for Reconstruction and Development.

There are challenges still to address: We have some 59 GW of total installed energy capacity (both renewable and non-renewable) — almost double peak demand. Overcapacity has hindered the development of new energy projects, the IEA says. A lack of private financing for new projects has also been a sticking point, according to the report.

Overcapacity will be partially addressed by the energy pillar of the government’s NWFE program announced at COP, under which 5 GW of gas-fired power plants will be decommissioned from 2023 to make room for fresh renewables investment. The program has already secured some USD 10 bn in development financing, which will be leveraged to de-risk the sector and attract private investors. Moves to link our electricity grid with neighboring countries including Greece and Cyprus — allowing us to export electricity to Europe — could also help solve the overcapacity problem.

Our net metering system is also expected to “continue to encourage distributed PV growth, especially large utility-scale projects for onsite self-consumption in agriculture and the cement industry,” the report says.

Saudi Arabia and Oman have their sights set on green hydrogen: Some 14% of the new renewable capacity (about 6 GW) added in the MENA region between 2022 and 2027 will come from hydrogen, the report says, with Oman and Saudi Arabia accounted for 80% of new hydrogen projects as they look to become export hubs for green ammonia.

That’s an ambition we share: The government has signed some 16 agreements with private firms to explore green hydrogen and green ammonia projects — including nine framework agreements signed at COP for projects that would, if implemented, bring in north of USD 80 bn worth of investments. Like the new wind projects, these are in the initial stages and so not reflected in the IEA figures.

Zooming out, the report has plenty to make us feel positive about the state of global renewables: Solar power as a global energy source is likely to surpass coal, natgas and hydropower by 2027, the report says. Renewable energy sources will make up about 40% of electricity output worldwide by the end of 2022. Meanwhile, green technology costs are on the decline, climate VCs are booming, and EV sales are on the rise. Check out this Twitter thread for a snapshot of more genuinely good climate news out of the report.

Your top green economy stories for the week:

- We held our inaugural Enterprise Climate X Forum last week: Catch the highlights from our panel on green hydrogen and the NWFE program.

- More green hydrogen momentum: Egypt signed MoUs with seven companies and consortiums to conduct feasibility studies on new projects to produce green hydrogen and its derivatives.

- Sustainable development bonds are still in the cards: The Finance Ministry is still on track to issue USD 500 mn of sustainable development bonds before the end of this fiscal year.

Enterprise is a daily publication of Enterprise Ventures LLC, an Egyptian limited liability company (commercial register 83594), and a subsidiary of Inktank Communications. Summaries are intended for guidance only and are provided on an as-is basis; kindly refer to the source article in its original language prior to undertaking any action. Neither Enterprise Ventures nor its staff assume any responsibility or liability for the accuracy of the information contained in this publication, whether in the form of summaries or analysis. © 2022 Enterprise Ventures LLC.

Enterprise is available without charge thanks to the generous support of HSBC Egypt (tax ID: 204-901-715), the leading corporate and retail lender in Egypt; EFG Hermes (tax ID: 200-178-385), the leading financial services corporation in frontier emerging markets; SODIC (tax ID: 212-168-002), a leading Egyptian real estate developer; SomaBay (tax ID: 204-903-300), our Red Sea holiday partner; Infinity (tax ID: 474-939-359), the ultimate way to power cities, industries, and homes directly from nature right here in Egypt; CIRA (tax ID: 200-069-608), the leading providers of K-12 and higher level education in Egypt; Orascom Construction (tax ID: 229-988-806), the leading construction and engineering company building infrastructure in Egypt and abroad; Moharram & Partners (tax ID: 616-112-459), the leading public policy and government affairs partner; Palm Hills Developments (tax ID: 432-737-014), a leading developer of commercial and residential properties; Mashreq (tax ID: 204-898-862), the MENA region’s leading homegrown personal and digital bank; Industrial Development Group (IDG) (tax ID:266-965-253), the leading builder of industrial parks in Egypt; Hassan Allam Properties (tax ID: 553-096-567), one of Egypt’s most prominent and leading builders; and Saleh, Barsoum & Abdel Aziz (tax ID: 220-002-827), the leading audit, tax and accounting firm in Egypt.