- Non-oil business activity plummets to all-time low in April as lockdown measures begin to bite. (Speed Round)

- First tranche of fresh IMF funding to land on Monday -report. (Speed Round)

- Budget deficit could widen to 7.8% due to covid-19 -Maait. (Speed Round)

- Egypt now has 7,201 covid cases after 388 new infections reported. (What We’re Tracking Today)

- Doing business in the covid economy: Here’s what CEOs and execs have been telling us. (What We’re Tracking Today)

- CBE instructs local banks to comply with new int’l reporting standards. (Speed Round)

- Instabug raises USD 5 mn in series A funding round. (Speed Round)

- Why shipping companies are suffering during covid-19, despite traffic remaining stable at Egypt’s ports. (Hardhat)

- The Market Yesterday

Wednesday, 6 May 2020

PMI plunges to record low. Plus: What CEOs expect next.

TL;DR

What We’re Tracking Today

It’s a relatively quiet morning in Egypt and around the world, with the biggest story on the home front being the breathtaking (if very much expected) plunge in the purchasing managers’ index last month. We have the full story in this morning’s Speed Round, below.

Still, we offer a sliver of sunshine on a (metaphorically) cloudy day: CEOs in Egypt are increasingly optimistic about the pace at which business could recover this year as the Madbouly government eases restrictions in place to slow the spread of covid-19. Here’s what we’re hearing after speaking with nearly a dozen CEOs and other top execs in the past week:

It was all doom and gloom from mid-March until mid-April when measures were first imposed. Sales slowed sharply across industries and execs were in full-on crisis mode managing staff safety, bankers, investors, supply chains and distribution while re-working budgets and strategy for 2020.

We’re looking at a slow Ramadan. Dessert sales coming in 30-40% lower this year compared to last? That’s the canary in the coal mine — but much better than the picture looked in the first two weeks of April.

Things have stabilized in the past two weeks as restrictions have eased somewhat. Execs have adapted to a “coexisting with covid” way of life — and their customers have, too. CEOs say their customers are slowly starting to spend again. Consumer appetite is coming back faster than is appetite from other businesses, but there’s a modest, across-the-board pickup (with all of the variation by industry that you’d expect).

Most CEOs we spoke with now expect 2Q to be their worst quarter this year. Only the last two weeks of the first quarter were hit when the state imposed covid-control measures in mid-March. April was hit from start to finish, and things have only started (slowly) stabilizing in the past 10-14 days.

They see business conditions improving in 3Q — and a handful of the most optimistic corporate bosses expect they may be able to start making up lost ground in the fourth quarter.

With the outlook for the rest of 2020 now seeming (a bit) clearer, execs should be asking what trends are going to (re?)shape their industries. We’ve previously argued that the pandemic will accelerate pre-existing trends in most industries, including the drive toward digital. With their businesses stabilizing, CEOs need to raise their heads and look to 2021 and beyond.

News triggers to keep your eye on over the coming days:

- Foreign reserves figures for April should be released sometime this week;

- Inflation figures for April are out on Sunday, 10 May.

- The CBE’s Monetary Policy Committee meets next Thursday, 14 May, to review interest rates.

The markets today: Asian shares are mixed in early trading this morning with the Nikkei and Shanghai Composite both down and shares up in Seoul and Hong Kong. Futures suggest US equities could open down this morning after posting a second straight day of gains yesterday, while Europe appears set to open cautiously in the green. The EGX30 fell for a third day in a row yesterday, easing 1.1% during a relatively light session that saw EGP 689 mn of shares change hands. The benchmark index is now down 27% since the start of the year.

So, when do we eat? Maghrib prayers are at 6:36pm and you’ll have until 3:31am to finish caffeinating. Fajr is coming one minute earlier every day through the end of the Holy Month.

COVID-19 IN EGYPT-

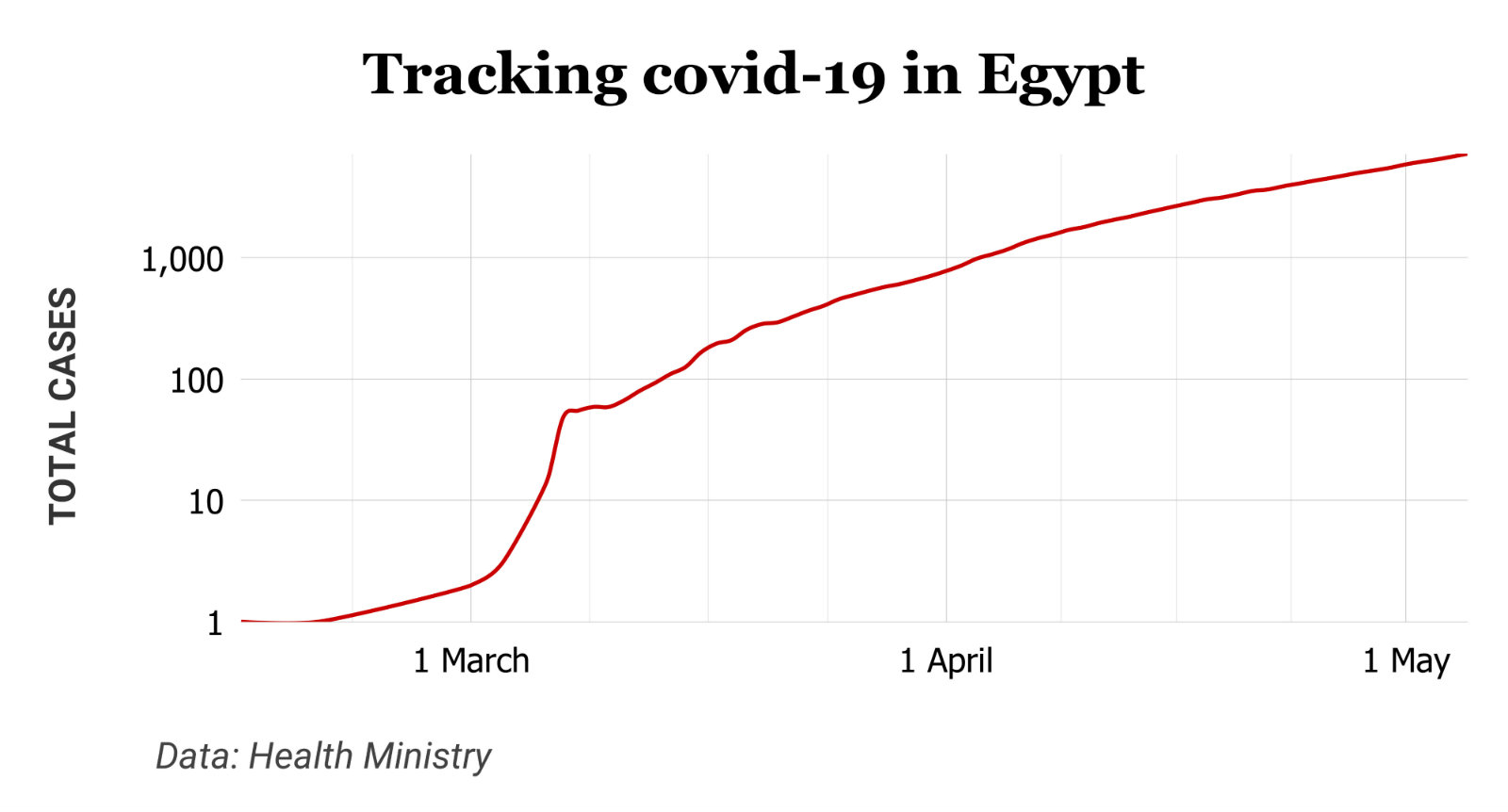

Egypt has now disclosed a total of 7,201 confirmed cases of covid-19 after the Health Ministry reported 388 new infections yesterday. The ministry also said that another 16 people had died from the virus, taking the death toll to 452. We now have a total of 2,224 confirmed cases that have since tested negative for the virus after being hospitalized or isolated, of whom 1,730 have fully recovered.

We’re running a logarithmic graph of total covid-19 infections in Egypt (above). It’s one of a number of ways to understand how the pace of infections is growing and illustrates what we suggested last week — the rate of doubling of new infections has slowed somewhat in the past month. Check out The Conversation for other ways of using graphs to understand covid-19.

Two Egyptian banks have landed USD 100 mn each from EBRD in the form of senior unsecured loans. The institution said yesterday that National Bank of Kuwait-Egypt and QNB Al Ahli had each landed tunding as part of the EBRD’s covid-19 response, noting that, “Proceeds of the proposed loan will be on-lent to local private small and medium enterprises and to corporates to cover liquidity needs that may arise as a result of covid-19.” The EBRD’s deputy chief in Egypt, Khalid Hamza, confirmed to the domestic press yesterday that the bank has earmarked EUR 850 mn in fresh credit to Egyptian banks for onlending to clients hit by covid.

Egypt is one of 13 African countries petitioning the IMF and World Bank for debt relief and restructuring, Finance Minister Mohamed Maait told the House Planning and Budgeting Committee yesterday, according to Al Mal. Maait and other African finance ministers last month called for international lenders to forgive and restructure debt. G20 countries agreed to freeze repayments for six months for low-income countries but have struggled to persuade private creditors to do the same.

Mass repatriation of Egyptians stranded aborad gets underway: The government is sending planes all over the region to bring back Egyptian expats stranded abroad. Press reports throughout the day yesterday (here, here, here, here, and here) talked about the flights a day Egyptians workers marooned in Kuwait protested and demanded to be allowed to return home.

What’s going on here? An increasing number of expats now want to return home, including those who had lost their jobs in the Gulf and some with health conditions, Emigration Minister Nabila Makram told talk show host Sherif Amer yesterday (watch, runtime: 6:18). As we noted yesterday, the Sisi administration is now running repatriation flights for Egyptians who were deemed resident in other countries; earlier flights focused on citizens who had been stranded while abroad for tourism or business visits.

Work on the Dabaa nuclear power plant hasn’t been slowed by covid-19, project director Grigory Sosnin tells Asharq Al Awsat. The first of four reactors is still on track to be operational within seven years.

ON THE GLOBAL FRONT-

Jordan has reached a USD 400 mn loan agreement with IMF to support the country’s liquidity position as it struggles with declining tourism revenues and exports, central bank governor Ziad Fariz said, according to Bloomberg.

Forecast predicts US death toll could double by August with lockdown rollbacks: Scientists are warning that the US could be looking down the barrel of a second surge of covid-19 as a growing number of states begin to relax lockdown restrictions, according to the Wall Street Journal. The University of Washington’s Institute for Health Metrics and Evaluation projects the death toll hitting 135k — double the current number of deaths — by the end of the summer as a result of the relaxed measures. A leaked government document seen by the New York Times this week suggests that the Trump administration is planning for around 3k daily deaths by 1 June.

The US, Russia, and China are flying solo in their bids to develop a covid0-19 vaccine, deciding against contributing to an EU-led fundraiser that has so far raised USD 8 bn, the New York Times reports. The EU and Norway made the largest pledges of EUR 1 bn each, with Canada having chipped in CAD 850 mn as the US, China and Russia each contributed USD 0.00.

We’re not out of the woods yet (with one in five Wendy’s in the US being out of beef), but food hoarding and curbs on exports are easing as worries about food security ease, according to a study of 17 countries by the International Food Policy Research Institute. Romania — a key supplier of wheat to Egypt — reversed last month a ban on grain exports outside the EU, but Russia is still refusing to rule out future quotas, waiting to see its harvest yield before determining whether it will reinstate curbs.

Egypt is expected to harvest 9 mn tonnes of wheat this year, Agriculture Ministry Spokesman Mohamed El Kersh said on eXtra News (watch, runtime: 04:44).

AND THE REST OF THE WORLD-

Covid-19 continues to ravage corporates on both sides of the Atlantic:

Disney has done the right thing and scrapped its dividend after reporting that covid-19 had erased as much as USD 1.4 bn from its bottom line in 1Q2020. Quarterly profit was down 90%, and there is probably much worse to come in 2Q.

More layoffs in the global travel industry: AirBnb and Virgin Atlantic have joined the growing list of companies linked to the travel business to announce staff cutbacks as the pandemic grinds the industry to a halt. The home rental unicorn is preparing to let go 25% of its workforce, or almost 1.9k employees, while Richard Branson’s airline said yesterday it’s getting ready to cut more than 3.1k jobs after its pleas for a state bailout were rejected by the UK government.

M&A fights: Reuters wonders who really won the M&A battle as private equity outfit Sycamore gets to walk away from its bid to acquire Victoria’s Secret

How much are flights going to cost when they eventually return? While Bloomberg is highlighting forecasts for USD 12 flights between Sydney and Melbourne, it’s unlikely that most of us are going to be enjoying super-cheap air travel when the aviation industry finally gets off its knees. In normal times low fuel prices and weak demand would be enough to knock a few bucks off your flight ticket, but as the International Air Transport Association (IATA) points out (pdf) the near-certainty of social distancing on airplanes will leave most carriers struggling to break even. Assuming planes have a 62% capacity limit, the IATA calculates that fares would need to rise by 43-54% to keep companies in profit, possibly making air travel more expensive than in pre-covid times.

*** It’s Hardhat day — your weekly briefing of all things infrastructure in Egypt: Enterprise’s industry vertical focuses each Wednesday on infrastructure, covering everything from energy, water, transportation, urban development and even social infrastructure such as health and education.

In today’s issue: Our follow up to last month’s surprising revelations on how little the global trade slowdown has impacted ship activity on Egypt’s ports. This time, we look at how things have panned out for the shipping companies, who have been suffering greatly during the covid-19 crisis. Why are shipping companies suffering during covid-19, despite traffic remaining stable at Egypt’s ports?

This publication is proudly sponsored by

Enterprise+: Last Night’s Talk Shows

With power couple Lamees El Hadidi and Amr Adib off yesterday, the airwaves gave us little to work with. The only segment worth noting was a phone call between host Ahmed Moussa and Damietta Governor Manal Awad about the covid-19 situation in the governorate.

Damietta records zero new cases -governor: The governorate reported zero new covid-19 infections yesterday and now accounts for only 1% of the country’s total, after having made up close to 11% earlier in the outbreak, Awad tells Moussa (watch, runtime: 5:13). This was a result of successfully implementing a Health Ministry plan to confront the virus, she said.

Speed Round

Speed Round is presented in association with

Non-oil business activity plummets to all-time low in April as lockdown measures bite: Egypt’s non-oil business activity fell at an “unprecedented rate” in April as government measures to stem the covid-19 outbreak caused a “severe decline” in business conditions, according to IHS Markit’s purchasing managers’ index (PMI) (pdf). The PMI gauge fell to a record low of 29.7 in April, down from 44.2 in March as output, new orders and exports plunged due to muted demand. PMI readings above 50.0 indicate expansionary activity, while a reading below means it is contracting.

New orders collapsed at a record rate: An evaporation of client demand caused new orders to fall at the fastest pace since the survey began in 2011. This was attributed to the Sisi administration’s anti-covid measures, which were in place through the month and included restrictions on working hours, the shuttering of the hospitality and tourism sectors, and the night-time curfew.

Businesses are cutting back: Lacklustre demand and falling output is forcing businesses to make cutbacks, including reducing input spending and labor costs. The month saw an acceleration of layoffs, causing employment to decline at the fastest rate in over three years and extending a trend that began in November. The cutbacks resulted in input costs rising at the slowest pace since the survey began.

“Businesses lucky enough to remain open scaled back activity on a massive scale, as many highlighted sharp falls in domestic sales and foreign demand. Firms forced to close unsurprisingly recorded an even steeper decline in output,” said David Owen, economist at IHS Markit.

Supplier delivery time has continued to increase, marking the second month in a row it has gone up since April and the longest wait times seen since October 2017. The slowdown has mostly been attributed to held up stocks at ports.

Raw material shortages have caused an uptick in some raw material prices, despite weak cost increases recorded by IHS but have done little to affect input costs on firms generally. Inventory levels were “drastically reduced” for many firms as uncertainty over future demand prevails.

Falling foreign sales and tourism due to airport shutdowns and global travel restrictions contributed to a “marked decrease” in purchasing activity at the start of the second quarter, spelling trouble for local vendors.

Improving sentiment may limit job losses: Despite the record blow to overall activity, sentiment improved slightly in anticipation of a reopening of the economy and heightened activity in the coming year. “Business expectations remain strong … which may suggest firms will look to retain workforces for when the economy reopens,” said Owen. “The outlook may darken through should the crisis worsen and measures are extended.”

Saudi Arabia’s economic activity also contracted, albeit at a slower rate in April. The kingdom’s PMI reading (pdf) came in at 44.4, inching up modestly from 42.4 in March. Private sector output is still suffering record declines while new orders and employment are struggling to grow.

The UAE’s reading continued to fall for the sixth consecutive month, recording a PMI of 44.1 (pdf), down from 45.2 in March. The country has been ailing from significantly reduced business activity since preventive measures against covid-19 have been instituted and optimism over future recovery has reached its most grim in months.

First tranche of fresh IMF funding to land on Monday -report: The government will receive USD 2.7 bn from the International Monetary Fund (IMF) next Monday as a first tranche of funding to help it withstand the global economic shock caused by the covid-19 pandemic, Masrawy reports, citing an unnamed central bank official. Authorities last month asked the fund for a one-year rapid financing instrument (RFI) to help plug shortfalls in the country’s balance of payments and a separate stand-by arrangement (SBA) to support fiscal reform.

Did Ahmed Moussa get it right on the new IMF package? We’re yet to hear anything official about the final size of the funding package, but TV show host Ahmed Moussa suggested that authorities are seeking north of USD 7 bn to help them through the crisis. We were fairly sceptical at the time, but Masrawy’s source has corroborated one of Moussa’s claims: that a USD 2.7 bn tranche would be delivered as early as 10 May. Moussa also said that a second tranche will arrive on our shores in June.

The IIF thinks we’re likely to receive around USD 8.4 bn: The Institute of International Finance (IIF) wrote in a note on Sunday that the IMF is likely to lend us a total of USD 8.4 bn through the RFI and SBA facilities. The fund will extend a USD 2.8 bn loan (100% of quota) under the RFI which will allow the government to ramp up health and welfare spending, provide relief to SMEs, and bolster foreign reserves, the IIF wrote. The IMF will also likely approve a two-year SBA giving Egypt access to funds worth 200% of its quota (around USD 5.6 bn). How much we end up receiving from the SBA would — in a similar fashion to the recent USD 12 bn extended fund facility — depends on financing needs, repayment capacity, and our track record in using previous IMF funds. The conditions, however, would be much less stringent than under the EEF, with the SBA having a shorter repayment period and fewer conditions.

Budget deficit could widen to 7.8% due to covid-19 -Maait: Egypt’s budget deficit could widen to 7.8% of GDP in FY2020-2021 if the covid-19 pandemic continues until the end of the year, Finance Minister Mohamed Maait warned yesterday. The government currently expects to narrow the deficit to 6.3% in FY2020-2021.

Primary surplus to fall, debt to rise: The primary surplus will fall to just 0.6% in the coming fiscal year if the crisis continues through to December compared to the 2% surplus currently expected by the government, Maait said. Debt would rise to 88% of GDP under this scenario from current projections of 83%.

This is actually a slight improvement on previous forecasts: Budget forecasts released last month predicted almost identical figures should the crisis last until July, signifying that the government now believes that the short-term impact of the pandemic on public finances may not be as severe as previously thought.

Gov’t likely to miss its budget targets this year: The budget deficit will likely widen to 7.8% or 7.9% in the current fiscal year instead of the 7.2% targeted prior to the covid-19 outbreak, Maait said.

GDP forecast was also cut this week: The government earlier this week lowered its GDP projection for the coming fiscal year to 2% from 3.5%, should the pandemic last until the end of the year.

The IIF is now forecasting the economy to grow by 1.6% in the state’s current fiscal year: The Institute of International Finance (IIF) expects the economy to contract by 2.5% during the second half of FY2019-2020 after growing at a 5.4% clip in the first six months of the year, it wrote in a note on Sunday.

The Central Bank of Egypt has instructed local banks to comply with the latest International Financial Reporting Standards (IFRS9) to ensure best practices during the covid-19 pandemic, according to a circular published yesterday (pdf). It called on banks to submit brief quarterly statements, and annual reports by the end of December or June 2021 where applicable. It added that the six-month holiday on loan installments for clients that began on 15 March will not be considered a core index in evaluating banks’ creditworthiness, but that they remain responsible for providing accurate credit portfolios and assessing their clients’ ability to repay.

GB Auto lands MG distributorship for Iraq: GB Auto has entered a partnership with SAIC Motor to distribute MG cars in Iraq, the company announced in a statement (pdf). The agreement covers fully imported models produced by the British auto company, and operations will begin in late 3Q or early 4Q2020. GB Auto exited its partnership with Hyundai in Iraq in February after the Korean multinational shifted to a multi-distributor model.

STARTUP WATCH- Instabug raises USD 5 mn in Series “A”: Cairo-based startup Instabug has raised USD 5 mn in series A funding, Menabytes reports. The round was led by Accel — which also led the company’s USD 1.7 mn seed round in 2016 — with the participation of Cloudera co-founder Amr Awadallah and MoPub founder and CEO Jim Payne. Instabug has now raised over USD 7 mn in funding to date. It has seen 120% revenue growth y-o-y, and is nearly profitable, according to co-founder and CEO Omar Gabr. Fundraising conversations with Accel reportedly started after the covid-19 outbreak, and Instabug intends to use the funding to accelerate its growth plans and launch new products in the coming months.

Instabug’s rapid growth has been given a boost by covid-19: Instabug began as a background tool for mobile app users to send feedback or report errors by shaking their phones and is evolving into a performance tracker for mobile app teams. It has seen usage grow by 45% since January this year, the company told Menabytes. “With more people spending their time at home, there’s more app downloads and more app usage. Also, Instabug is designed to streamline the communication between QA and developers which is very relevant now since all is working remotely,” representatives said in a statement.

OIH management of Lebanese mobile operator Alfa comes to an end after 11 years: The Lebanese government will not renew Orascom Investment Holding’s contract to manage state-owned mobile operator Alfa and will issue a new management tender within three months, according to Reuters. Sawiris family-owned OIH was awarded the contract to manage Alfa, one of the two Lebanese state mobile companies, back in 2009 and has had its contract repeatedly renewed. The Lebanese Telecom Ministry said yesterday that it will take over the management of Alfa and other state mobile company Touch while it prepares the new tender. The country’s other MNO, Touch, has been run by Kuwait’s Zain Group since 2004.

Making It’s fourth episode drops Thursday featuring a microfinance pioneer: Back when financial inclusion was just a buzzword, our next guest saw an opening in an underserved segment of the Egyptian business community. His 11-year journey saw him grow to 270 branches nationwide, navigating banks, policy makers, and private equity giants to create a new sector that brings the informal economy into the fold.

Can’t wait until then? Listen to our previous episode with Laila Sedky and Adel Sedky from Nola (runtime 38:51) on our website | Apple Podcast | Google Podcast | Omny. We’re also available on Spotify, but only for non-MENA accounts. Subscribe to Making It on your podcatcher of choice here.

Egypt in the News

The release of US-Egyptian citizen Reem Dessouky from an Egyptian prison is still getting traction in the international press: The New York Times reports the art teacher renounced her Egyptian citizenship before boarding a plane back to the US on Sunday. Al Monitor also has the story.

New Ramez prank show beyond a joke: Lawmakers, including Mortada Mansour himself, are lining up calls and complaints to Prime Minister Moustafa Madbouly and the public prosecutor’s office to ban full-time prankster / former actor Ramez Galal’s Ramadan show for “inciting violence against women,” Reuters reports.

Outbreak “adds urgency” to ending arbitrary arrests in Egypt- HRW: The covid-19 pandemic has made it necessary for the US to end its support for Egypt’s security services as prison conditions are “ripe for a public health crisis,” Human Rights Watch argues.

Worth Reading

What is the ‘R’ number and how will it determine when societies can escape lockdown? The reproduction — or ‘R’ — number is a measure used by epidemiologists to determine how rapidly a disease spreads through a population. It’s calculated using the average number of new cases generated by an infected person. If the number is below 1, it indicates the virus is contracting while numbers exceeding 1 indicate exponential growth. Politicians are keeping a close eye on the R number and countries who have managed to push the figure below this crucial threshold have slowly begun lifting lockdowns. Wired has the full breakdown on how health experts are using R to track the virus.

Why are shipping companies suffering during covid-19 if traffic into and out of Egypt’s ports is basically stable? It’s complicated. Traffic at Egypt’s leading ports including East Port Said, Alexandria, and Damietta has largely remained stable despite the impact on trade from covid-19, we reported last month, but shipping and logistics firms are suffering. And the challenge could only get worse as low oil prices, Suez Canal fees and high port charges encourage more shipping lines to go around the Cape of Good Hope and bypass Egypt altogether.

Why is the slowdown affecting shipping companies, but not impacting traffic at ports? The short answer is agriculture, which has been keeping port activity busy during 1Q2020. As we enter a stage where lockdowns in a number of countries are being phased out — most significantly in China and Italy (two of Egypt’s largest trade partners) — industry insiders expect to see an uptick in demand. But these gains can only be achieved if the government can respond with the right incentives.

How badly have shipping companies been hit? Inbound container traffic fell 20% y-o-y in April 2020, said Mohamed Moselhy, local shipping agent for YangMing Marine Transport. Container traffic since the start of the crisis in mid-January had fallen 10-20% below where they were at in December 2019, he said.

This has translated into losses for shipping companies, with a drop in revenue from Egypt’s ports ranging from 50-70% y-o-y in April alone, said Ahmed Moustafa, who heads up the Egypt branch of the International Federation of Freight Forwarders Associations (FIATA). YangMing’s Moselhy puts the figure closer to 50%.

The picture is grim when looking at earnings of EGX-listed shipping and maritime companies that have announced results in 2020. The United Arab Stevedore Company has seen its 9M2019-2020 losses grow by 20% y-o-y on the back of a 70% y-o-y drop in tonnage shipped, according to a company bourse filing (pdf). Their March figures indicate a 20% y-o-y drop in revenues on the back of a 100% y-o-y drop in shipping tonnage. The Alexandria Container and Cargo Handling Company saw its 9M2019-2020 revenues fall 12.3% y-o-y on the back of a 4% y-o-y drop in containers handled in March, according to a bourse filing (pdf). Egytrans, Egypt’s only listed private sector company, has yet to report earnings in 2020 but said in a bourse filing (pdf) that it expects to be negatively impacted by the covid-19 crisis in the coming period.

Industry losses in Egypt in line with global figures: The first half of 2020 could see a 25% fall in global shipping, Alan Murphy, chief executive of analysts Sea-Intelligence, told the BBC. Global shipping can expect to see a decline of around 17 mn twenty-foot equivalent units (TEUs) (industry-speak for containers) which amounts to around 10% of global volumes, Sea-Intelligence CEO Lars Jensen tells UBS. Ports and terminals could “potentially be looking at a loss of 80 mn TEU of handling volume.” Global shipping is experiencing losses of around USD 350 mn per week, the firm also said. A slowdown in China’s ports is playing a major role in this drop, with the number of containers coming out of its ports is expected to fall 6 mn TEU in 1Q2020, according to a report by shipping firm Alphaliner picked by Al Mal.

Oil geopolitics make Egypt shipping vulnerable: In addition to the slowdown in global trade, the oil price crash has had an adverse effect on shipping traffic and container handling at Egypt’s ports by incentivizing some of the world’s biggest companies to move their ships through countries with cheaper port fees. The 2M Alliance of Maersk Line and Mediterranean Shipping Company rerouted some of their China-EU ships from the Suez Canal and around South Africa’s Cape of Good Hope. It takes longer, but it’s less expensive with low oil prices — and cost-efficiency (not time) is the name of the game for the industry right now. This comes after France’s CMA-CGM shipping line announced in early April that it would take the South Africa route. When fuel prices are low, shipping companies can afford to go longer distances to ports with lower fees, Moselhy explained.

Are Egypt’s port fees too expensive? The high fees charged by Egyptian ports have been pushing companies into the arms of regional competitors for some time now. While Egyptian port authorities have been busy hiking fees, Moselhy tells us that ports in Greece and Cyprus have lowered their fees by 25-30%, making the destination a no-brainer for many companies.

The impact on shipping activity in Egyptian ports has so far been muted: We noted last month that the port of East Port Said saw a 36.4% increase y-o-y in the number of containers being moved at the port in 1Q2020. The port of Alexandria — which handles 70% of the commercial goods that pass through the nation’s ports — has remained steady, with the port moving an average of 7-10k containers per day in March. When asked on the impact the rerouting of ships by major shipping companies has had on Egypt’s ports, Suez Canal Economic Zone (SCZone) Chairman Yehia Zaki told us that major shipping companies continue to operate in Egypt and the impact of competing ports slashing prices has been minimal. So why haven’t we seen this decline in global shipping reflected in Egypt’s port activity?

Agriculture to the rescue: Almost all shipping companies and port officials we’ve spoken with say that the agriculture export season has kept traffic at Egypt’s ports at a steady pace. We’re seeing a 4-5% increase in outbound shipping thanks to the export season, says Moselhy. The number of ships moving agricultural goods through the port of Alexandria increased 21% y-o-y in 1Q2020, the port’s spokesperson Reda Ghandour tells Enterprise. Volumes of agricultural goods being handled at the port also rose 37% y-o-y in 1Q2020 to 205.8k tonnes.

Officials we spoke with last month had also attributed the continued activity at Egypt’s ports to a backlog of shipping from long-term contracts.

But these haven’t translated into gains for the shipping industry: For starters, if you do not ship agriculture or other essential goods during covid you are out of luck. Global trade has seen a decline in non-essential goods while essentials are continuing to be moved, said FIATA’s Moustafa. Even the long-term contracts are primarily for essential goods, he added. Furthermore, the costs and fees of docking inbound ships at Egypt’s ports and the handling of import cargo is much higher on maritime companies than for outbound ships and export cargo, says Moselhy. This means that gains in export activities are outweighed by the losses in import activities, he added. Other shipping agents we’ve spoken to also noted that an increase in the number of ships does not mean profitability is up. Container numbers and cargo are the bread and butter of the industry, so more ships carrying less cargo compounds losses, they tell us.

All good things must come to an end: The current rise in agriculture exports may not continue at the pace it is in the long-term and long-term contracts will run out. Officials we’ve spoken with could not pinpoint when that day may come, but hinted at a decline in shipping traffic if the covid-19 crisis continues past that point.

Lockdown fatigue could be the industry’s silver lining: As the global discussion over when lockdowns can be eased and economic activity can start picks up, shipping companies are pinning their hopes that this may come sooner than later. Keeping these hopes alive is the easing of the lockdown in China, the US (the biggest importer of Egyptian garments), and Italy (Egypt’s third largest trading partner). Moustafa sees the moment of truth happening in mid-July, telling us that he expects a “significant” jump in shipping activity.

But even if that does happen, Egyptian ports will need to be more competitive in order to lock in those gains. In response to Cyprus and Greece lowering their port fees, the Maritime Transport Sector has lobbied the port of Alexandria to study responding with their own port fees, said Moselhy. And that appears to have already begun. The Suez Canal Authority reduced fees for container ships crossing the Suez Canal until 30 June by 60%-75% for transit container ships originating from the US and heading to destinations in Southeast Asia. Container ships originating from Northwest Europe and the ports of Tangier and Algeria, also heading to Southeast Asian ports, will see fees reduced by 17% as of 1 May and until 30 June. The question is: Will these be enough?

Your top infrastructure news of the week:

- Logistics: Maersk and MSC plan to reroute an unspecified number of their container ships from the Suez Canal to the Cape of Good Hope bypassing Suez Canal’s passage fees.

- Ports: The Suez Canal Authority has reduced fees for container ships crossing the Suez Canal until 30 June

- Rural infrastructure: Egypt will obtain a USD 400 mn World Bank loan for universal healthcare which will include completing several infrastructure projects in the cities where the scheme will be implemented.

- Energy: SDX Energy is expected to produce 10-12 mcf/d of natural gas from its Sobhi well.

- Transit: The Transport Ministry is considering using Bus Rapid Transit (BRT) systems to help reduce Ring Road traffic.

The Market Yesterday

Powered by![]()

EGP / USD CBE market average: Buy 15.69 | Sell 15.79

EGP / USD at CIB: Buy 15.70 | Sell 15.80

EGP / USD at NBE: Buy 15.68 | Sell 15.78

EGX30 (Tuesday): 10,188 (+1.1%)

Turnover: EGP 689 mn (1% above the 90-day average)

EGX 30 year-to-date: -27.0%

THE MARKET ON TUESDAY: The EGX30 ended Tuesday’s session up 1.1%. CIB, the index’s heaviest constituent, ended up 0.9%. EGX30’s top performing constituents were GB Auto up 4.0%, Telecom Egypt up 3.0%, and Ibnsina Pharma up 2.7%. Yesterday’s worst performing stocks were Dice down 6.8%, EFG Hermes down 1.4% and Credit Agricole down 0.8%. The market turnover was EGP 689 mn, and local investors were the sole net sellers.

Foreigners: Net Long | EGP +23.7 mn

Regional: Net Long | EGP +4.7 mn

Domestic: Net Short | EGP -28.3 mn

Retail: 65.1% of total trades | 66.2% of buyers | 63.9% of sellers

Institutions: 34.9% of total trades | 33.8% of buyers | 36.1% of sellers

***

PHAROS VIEW

xx

***

WTI: USD 24.15 (+18.44%)

Brent: USD 30.31 (+11.43%)

Natural Gas (Nymex, futures prices) USD 2.14 MMBtu, (+7.38%, Jun 2020 contract)

Gold: USD 1,707.60 / troy ounce (-0.33%)

TASI: 6,710.51 (+1.74%) (YTD: -20.01%)

ADX: 4,103.82 (+1.63%) (YTD: -19.15%)

DFM: 1,931.66 (+0.36%) (YTD: -30.14%)

KSE Premier Market: 5,273.81 (+1.76%)

QE: 8,799.73 (+1.52%) (YTD: -15.59%)

MSM: 3,493.16 (-0.20%) (YTD: -12.26%)

BB: 1,298.37 (-0.20%) (YTD: -19.36%)

Calendar

14 May (Thursday): The CBE’s Monetary Policy Committee will meet to review interest rates.

23 May (Saturday): Earliest date on which suspension of international flights to / from Egypt expires.

23 May (Saturday): Earliest date by which restaurants, gyms, nightclubs, museums and archaeological sites will reopen.

23 May (Saturday): An administrative court will look into an appeal by steel rolling mills to overturn a government’s decision to place import tariffs on steel rebar and iron billets. The hearing was postponed from 22 February 2020.

23-26 May (Saturday-Tuesday): Eid El Fitr (TBC).

31 May (Sunday): A postponed court session for the lawsuit filed by Cairo Development and Auto Industry, a subsidiary of Arabia Investment Holding, against Peugeot Automotive to demand EUR 150 mn compensation.

9-10 June (Tuesday-Wednesday): US Federal Open Market Committee will hold its two-day policy meeting to review the interest rate.

30 June (Sunday): Anniversary of the June 2013 protests, national holiday.

25 June (Thursday): The CBE’s Monetary Policy Committee will meet to review interest rates.

28-29 July (Tuesday-Wednesday): US Federal Open Market Committee will hold its two-day policy meeting to review the interest rate.

30 July-3 August (Thursday-Monday): Eid El Adha (TBC), national holiday.

13 August (Thursday): The CBE’s Monetary Policy Committee will meet to review interest rates.

20 August (Wednesday-Thursday): Islamic New Year (TBC), national holiday.

15-16 September (Tuesday-Wednesday): US Federal Open Market Committee will hold its two-day policy meeting to review the interest rate.

24 September (Thursday): The CBE’s Monetary Policy Committee will meet to review interest rates.

24 September- 2 October (Thursday-Friday): El Gouna Film Festival, El Gouna, Egypt.

6 October (Tuesday): Armed Forces Day, national holiday.

29 October (Thursday): Prophet Mohamed’s birthday (TBC), national holiday.

November: Egypt will host simultaneously the International Capital Market Association’s emerging market, and Africa and Middle East meetings.

4-5 November (Tuesday-Wednesday): US Federal Open Market Committee will hold its two-day policy meeting to review the interest rate.

12 November (Thursday): The CBE’s Monetary Policy Committee will meet to review interest rates.

15-16 December (Tuesday-Wednesday): US Federal Open Market Committee will hold its two-day policy meeting to review the interest rate.

24 December (Thursday): The CBE’s Monetary Policy Committee will meet to review interest rates.

25 December (Friday): Western Christmas.

1 January 2021 (Friday): New Year’s Day, national holiday.

7 January 2021 (Thursday): Coptic Christmas, national holiday.

Enterprise is a daily publication of Enterprise Ventures LLC, an Egyptian limited liability company (commercial register 83594), and a subsidiary of Inktank Communications. Summaries are intended for guidance only and are provided on an as-is basis; kindly refer to the source article in its original language prior to undertaking any action. Neither Enterprise Ventures nor its staff assume any responsibility or liability for the accuracy of the information contained in this publication, whether in the form of summaries or analysis. © 2022 Enterprise Ventures LLC.

Enterprise is available without charge thanks to the generous support of HSBC Egypt (tax ID: 204-901-715), the leading corporate and retail lender in Egypt; EFG Hermes (tax ID: 200-178-385), the leading financial services corporation in frontier emerging markets; SODIC (tax ID: 212-168-002), a leading Egyptian real estate developer; SomaBay (tax ID: 204-903-300), our Red Sea holiday partner; Infinity (tax ID: 474-939-359), the ultimate way to power cities, industries, and homes directly from nature right here in Egypt; CIRA (tax ID: 200-069-608), the leading providers of K-12 and higher level education in Egypt; Orascom Construction (tax ID: 229-988-806), the leading construction and engineering company building infrastructure in Egypt and abroad; Moharram & Partners (tax ID: 616-112-459), the leading public policy and government affairs partner; Palm Hills Developments (tax ID: 432-737-014), a leading developer of commercial and residential properties; Mashreq (tax ID: 204-898-862), the MENA region’s leading homegrown personal and digital bank; Industrial Development Group (IDG) (tax ID:266-965-253), the leading builder of industrial parks in Egypt; Hassan Allam Properties (tax ID: 553-096-567), one of Egypt’s most prominent and leading builders; and Saleh, Barsoum & Abdel Aziz (tax ID: 220-002-827), the leading audit, tax and accounting firm in Egypt.