- State privatization program moves forward as ACCH wraps up first phase of its roadshow for secondary offering. (Speed Round)

- Russian Industrial Zone aims to land 100 new agreements this year. (Speed Round)

- Egypt’s tech startups have had a good week. (Speed Round)

- Draft FY2019-2020 budget gets committee nod, setting up general assembly vote as early as next week. (Speed Round)

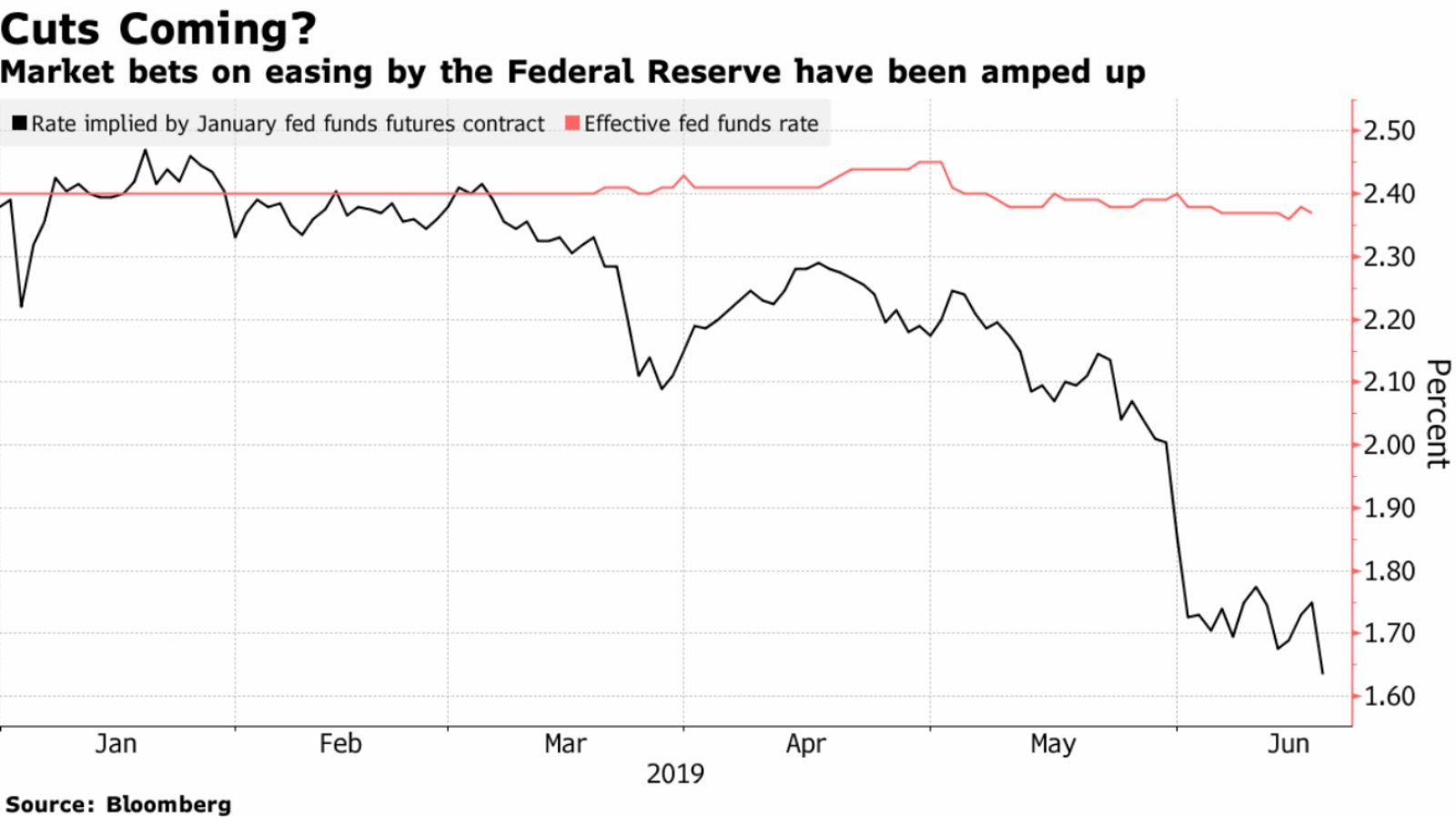

- Markets seem certain of US easing in July after the Fed left rates on hold yesterday. (What We’re Tracking Today)

- Why Mohamed El Erian thinks advanced economies are behaving more and more like emerging markets. (What We’re Tracking Today)

- Is Tarek Amer calling for an African version of the ECB? (Worth Watching)

- Hany Al Sonbaty, managing partner at Sawari Ventures (My Morning Routine)

- The Market Yesterday

Thursday, 20 June 2019

State privatization program moves forward.

Plus: A good week for early-stage tech startups

TL;DR

What We’re Tracking Today

Expect the FY2019-2020 budget debate to dominate the headlines next week. The House of Representatives general assembly will reconvene on Saturday to conclude debate of the FY2019-2020 budget before a vote.

Pharos Holding’s annual investor conference (pdf) wraps up today in El Gouna. The two-day event brought together investors, IPO prospects and more than 40 listed companies for meetings with institutional investors in one-on-one meetings during the conference’s first day.

The African Cup of Nations kicks off tomorrow at Cairo Stadium at 10 PM CLT. The Pharaohs are set to play Zimbabwe in the first match of Group A, which also includes DR Congo and Uganda. CAF has warned participating teams of high temperatures that will average 35-38ºC over the coming month, Reuters noted. Summer in Cairo. Shocking, we know.

The tournament featured heavily in coverage of Egypt in the international press. We have a look in this morning’s Egypt in the News, below.

The US Federal Reserve left key interest rates on hold but indicated that it could cut them in the coming months if the economic outlook in the US deteriorates, the Wall Street Journal reports. “The case for a somewhat more accommodative policy has strengthened,” Fed Chairman Jay Powell said at a news conference following the conclusion of the two-day FOMC meeting. The benchmark rate is currently in a target range of 2.25% to 2.50%. The reaction on Wall Street was muted: The S&P was up 0.3%, while the Dow rose 0.15%.

When could we see a rate cut? The “divided” Fed may be guiding for a cut or two in 2020, but bond traders aren’t on the same page, CNBC and Bloomberg say. Federal funds futures now give a 100% chance of the central bank cutting rates and a 67% chance of a cut to 2% when officials next meet on 30-31 July. Market expectations of a rate cut before the end of the year have continued to rise in recent weeks as trade tensions and slowing global growth weigh on the minds of investors.

Advanced economies are behaving like emerging markets, El Erian says: ECB chief Mario Draghi’s suggestion yesterday that the central bank could soon resort to more stimulus measures is another example of how advanced economies are starting to act like emerging markets, Mohamed El Erian writes for Bloomberg.

Huh? Problems created by economic crises in EMs often cause considerable political and social instability. This is unlike advanced economies, which until the 2008 financial crisis were relatively adept at ensuring that economic turbulence didn’t affect the political status quo. Since 2008, though, developed countries have followed a path that more closely resembles emerging markets. Many countries have seen a fundamental change in political direction, while the efficacy of institutions has slowly eroded amid falling public trust.

Draghi’s short-term policy prescriptions are another step in this direction: The ECB’s willingness to fall back on increasingly ineffective short-term stimulus measures will only exacerbate problems that lie further down the road. “Such measures are developing deeper socio-political roots that render incremental reforms harder to enact, taking economies ever closer to cliff-like conditions involving the threat of accelerating economic and financial weakness in the absence of ‘big bang’ reforms,” El Erian says.

Exhibit A: Draghi’s dovish tone sent the value of the negative-yielding bond market to record highs of USD 12.5 tn yesterday, the FT reports.

Investors are making it rain for private equity: European private equity groups are looking to cash in on record investor demand and raise bns in funds before market conditions weaken, the FT says. CVC Capital Partners is targeting a record EUR 18 bn fund, while Swedish EQT expects to raise a record flagship fund of around EUR 14 bn next year.

Demand for private equity is going through the roof as investors search for returns amid a low interest rate environment. “There is a wall of cash desperate to be assigned to a private equity fund,” Ludovic Phalippou, professor of finance at Oxford Said Business School.

Just don’t expect prospective limited partners to have much appetite for MENA after the implosion of Abraaj…

You’re going to want to show this one to your employer: We should only be working eight hours per week (yes, per week — not per day) for good mental health, researchers from the University of Cambridge and the University of Salford have said after examining more than 71k employees in the UK. CNBC has the story.

This publication is proudly sponsored by

Enterprise+: Last Night’s Talk Shows

El Sisi talks cooperation with Romanian counterpart: President Abdel Fattah El Sisi discussed strengthening economic and political ties with Romanian President Klaus Iohannis during his visit to Bucharest yesterday, Al Hayah Al Youm’s Khaled Abu Bakr noted (watch, runtime: 06:59).

The Sisi administration is planning to provide in-kind compensation to Nubians who were impacted by the construction of the Aswan Dam, Abu Bakr said in another segment (watch, runtime: 05:53). Cabinet discussed the logistics of the initiative in their meeting yesterday following instructions from the president. Some 11k people who lost their homes during the construction of the dam are eligible for compensation, Yahduth Fi Misr’s Sherif Amer said (watch, runtime: 01:39).

Finally, a phone call between your favorite goal scorer Mohamed Salah and Al Azhar Grand Imam Sheikh Ahmed El Tayeb, who offered some spiritual advice ahead of Afcon, also earned some airtime on Yahduth Fi Misr (watch, runtime: 01:29).

Speed Round

Speed Round is presented in association with

Progress in state privatization program as opening legs of Alexandria Containers roadshow conclude: Advisers on the share sale by state-owned Alexandria Containers and Cargo Handling Company (ACCH) have concluded roadshows in Dubai and London as the company gears up for a secondary offering under the state privatization program, Al Mal reports, citing unnamed sources. EFG Hermes and Citi met with investors who reportedly pressed them about the company’s profits, expansion plans, reserves and shareholder structure. It is still unclear how the offering is going down with potential institutional investors.

This is good news for watchers of the state’s privatization program, who have been waiting for signs of progress on the share sale. And there’s more to come, with the roadshow expected to resume in the US within the next month.

Where does the program stand? ACCH and Abu Qir Fertilizers are expected to sell additional shares on the EGX, but those transactions have been on hold pending recommendations on timing by the investment banks quarterbacking the sales, Public Enterprises Minister Hisham Tawfik said earlier this month. Eastern Tobacco piloted the program with the sale of a 4.5% stake earlier this spring.

What about state IPOs? Companies selected to IPO under the program could begin listing as early as September, Tawfik said. It is widely believed that Enppi will be the first company to go public.

INVESTMENT WATCH- Russia predicts 100 new agreements for RIZ this year: There is growing interest among Russian companies to set up shop in the USD 7 bn Russian Industrial Zone (RIZ), with the Russian Export Center (which is managing RIZ) expecting to see 100 new agreements signed this year, according to statements by the center picked up by Russian state news agency Tass. “About 20 agreements have already been signed, we aim for 100 agreements this year,” REC chief Andrei Slepnev said at the Russia-Africa economic conference, currently taking place in Moscow. Forecasts from the Russian Industry and Trade Ministry suggest that the project may take up to 13 years to be fully implemented, but by 2026 companies will be able to produce USD 3.6 bn worth of products each year.

I can has direct flights now? The RIZ is wonderful. But you know what? We’re greedy. We’d like to see the resumption of direct flights from Russia to the Red Sea.

STARTUP WATCH- It was a good week for tech startups: Cairo Technology Week and the Seamless North Africa conference, which both took place this week, saw lots of startups (most of them early stage ventures) in the spotlight. Among the highlights:

Paynas wins first prize at Seamless North Africa 2019: Egyptian fintech startup Paynas took home first place for its pitch at the Seamless North Africa conference this week, according to an emailed statement (pdf). The company, which provides a cloud-based platform used to manage banking, HR, and employee benefits, walked away with USD 50k after going head-to-head with four other startups.

Flat6Labs Cairo graduated eight new startups at its first cycle of 2019, the startup accelerator said in a statement (pdf). Graduates are in sectors including virtual reality, legaltech and logistics, manufacturing, software as a service), hardware and education and wellness. They are: VRapeutic, Untap, Illa, Agrona, Elmetr, Instadiet, Tyro and Interact.

Meanwhile, three Egypt-based startups have been selected to participate in the four-month Womentum Accelerator program, run by Womena and Standard Chartered, Disrupt Africa reports. Participating startups from Egypt include FreshSource, which connects small-scale farmers to the value chain, Chefaa, an AI-powered platform for buying pharma products, and pas-sport, a platform that connects athletes with sports scholarships at universities globally.

LEGISLATION WATCH- House Budget committee approves FY2019-2020 draft budget: The House of Representatives Planning and Budget Committee has approved the draft budget for the FY2019-2020 fiscal year and referred it to the general assembly to set a date for a vote, MP Yasser Omar told the local press. The House will meet on Saturday for final discussions before members cast their ballots, Masrawy reported. Here’s a recap of the figures that matter:

- GDP growth registering 6% by June 2020;

- Budget deficit of 7.2% of GDP, down from 8.4% in the current fiscal year;

- Primary budget surplus of 2%;

- Reducing public debt to 89% of GDP, with an eye to bringing that figure down to 80% by FY2021-22;

- Unemployment falling to 9.1% and population growth slowing to 2.3%.

Education and health get some love: The committee agreed that an additional EGP 1.5 bn goes to education, an additional EGP 1.9 bn goes to the health sector, an additional EGP 2.5 bn goes to higher education and an additional EGP 1 bn goes to the transportation sector, in addition to other smaller increases, Omar said. The increases in the allocations given to the education and health sectors come short of the EGP 10 bn and EGP 27 bn the ministries had asked for, respectively.

LEGISLATION WATCH- Small amendments to capital requirements in latest draft of proposed Insurance Act: The Financial Regulatory Authority (FRA) has largely kept minimum capital requirements for property and life insurance companies unchanged in the final draft of the new Insurance Act, sources told Al Mal. The minimum for life and property insurance companies remained at EGP 150 mn, unchanged from an earlier draft which leaked in January.

Companies that need longer than the three-year grace period can apply for an extension. The sources said that the draft also relaxes the rules for companies planning to provide fuel hedging contracts or services to the aviation sector, reducing the amount of additional capital they would have had to raise to EGP 150 mn from EGP 300 mn previously.

New draft has a built-in amendment mechanism? The sources said that the final draft grants the FRA the power to revoke “any contentious article through regulatory decisions” after the law is published, without having to go through the traditional amendment process.

Shareholders in insurance companies can now become CEOs: The latest draft reverses an article that banned any insurance company shareholder from acting as chairman or CEO. This draft will restrict the position to only shareholders in non-listed businesses insurance companies. The latest draft also mandates that a minimum of two board members must work in the industry, down from three previously.

Insurance payout and coverage regs to remain the same: The bill will still double the ceiling for life insurance payouts to EGP 80k, from EGP 40k currently. It also appears to still contain stipulations making insurance coverage for public gatherings and venues (such as malls and concerts) mandatory and requiring individuals with liability-prone professions (such as doctors and architects) to obtain liability insurance.

Where do we stand? The final draft will now have to be reviewed by cabinet for approval. It will then be handed over to the State Council for a legal opinion before its introduction to the House of Representatives for a final vote, and a subsequent signing into law by the president.

LEGISLATION WATCH- FinMin finalizes PPP Act amendments: The Finance Ministry has put the final touches on draft amendments that would streamline public-private partnership (PPP) contracts, according to a cabinet statement. The draft received cabinet approval late last year and has been with the government since then.

What is changing? The amendments would cut the time to issue tenders for public-private partnership (PPP) projects and introduce new mechanisms for private sector contracting. Private sector players would be allowed to submit unsolicited proposals, and the government to negotiate directly with a sole bidder without needing to take the project through the competitive bidding process. The sector will also be able to participate in a wider range of projects — particularly when it comes to infrastructure, public services, and utility developments. A specialized committee will be set up with members from the finance and planning ministries to assess project proposals and determine which could be executed under a PPP model.

What’s next: It is unclear whether it will make it to the House of Representatives before the expected end of the legislative session next week. In any case, it is highly unlikely it could pass committee and make it to the floor for a vote before MPs recess for the summer — look for the bill to be on the agenda when the House reconvenes on or before the first Thursday in October.

CABINET WATCH- Gov’t agrees to lower interest rates on industrial land purchases: The cabinet has agreed to a proposal from the Industrial Zones Coordination Council to set the interest rate for industrial land purchases at 7% per year,instead of CBE rates, it said in a statement yesterday following its weekly meeting. The decree, effective for three years, aims to attract investment into the sector and create space for new industrial areas and jobs. The cabinet also agreed to:

- Allocate a land plot to Bosch Home Appliances to build a factory in 10th of Ramadan City;

- Increase the rent of state-owned land for poultry and livestock companies by 12% every three years under the right-to-use framework for 30 years;

- Some amendments to the executive regulations of the Universities Act, including allowing Suez University to launch a dentistry section.

Toyota snubs Saudi Arabia: Toyota is reportedly backing out of plans to build a car plant in Saudi Arabia, sources close to the matter tell Reuters. “Nobody would say ‘No, full stop’ … but they politely conveyed they’re not interested,” one source is quoted as having said. Saudi Arabia signed an MoU with Toyota back in March 2017 to begin a feasibility study on building an auto factory in the kingdom. The study concluded that Saudi Arabia would need to provide huge subsidies for the project to be viable. “They found that production costs will be similar to other countries only if there is a 50% government incentive. But even then, they aren’t sure it will be profitable,” said one source.

This may not be good for us: The feasibility study was supposed to look at the possibility of sourcing auto parts from Egypt and Turkey as part of an analysis to see whether Toyota could make margins on assembled-in-KSA vehicles more attractive than those on full imports.

Nonetheless, in the fight for FDI regionally, Egypt is looking more attractive to car companies than Saudi: Saudi Arabia’s reforms have failed to entice auto companies to set up shop, with industry insiders noting that other regional countries, such as Egypt, are proving more attractive. “Saudi Arabia and (Gulf) countries have been persistently disappointing in terms of sales in recent years, so it’s not as if original equipment manufacturers would be entering a booming market,” Justin Cox, director of global production at LMC Automotive, tells Reuters. Egypt and Turkey have more advantages for carmakers, he said.

Is now the time for auto companies (including Toyota) to come to Egypt? This week, we reported that the government is studying a new set of incentives that were meant to encourage assemblers to move up the value chain towards manufacturing, while the Trade and Industry Ministry lowered the requirements for locally-sourced car parts to be considered made in Egypt. It was reported back in April 2018 that Toyota and Nissan were waiting on the Automotive Directive (an earlier draft of the incentives program) to decide whether to expand their investments in Egypt. A few months later, the government said it was in talks with Toyota and Volkswagen to open up shop at the Russian Industrial Zone currently being built in the Suez Canal Economic Zone.

CORRECTION- We reported yesterday that Attijariwafa Bank has named Hicham Seffa (LinkedIn) as managing director in Egypt to succeed Halla Sakr, who will assume a new position: She is to become the lender’s chairman (pending central bank approval), not its CEO as we said yesterday. We have corrected the story on our website.

** WE’RE HIRING: We’re looking for smart, talented journalists and analysts to join our team and help us make both the product you’re reading now and some exciting new stuff. We’re particularly interested people with writing plus either audio or video skills.

Interested? Send your CV along with 2-3 writing samples and a solid cover letter telling us a bit about who you are and why you’re a good fit for our team. Email us at jobs@enterprisemea.com.

Egypt in the News

Morsi’s death and Afcon dominate the conversation on Egypt in the international press this morning: Barrels of toxic ink are being spilled on Egypt in the foreign press. There were many pickups of wire reports on the news that Egypt accused the UN of being politically motivated in its calls for an investigation into Morsi’s death. Reuters, WSJ and Bloomberg are reporting that Turkey’s cry-baby-in-chief is demanding that the Egyptian government be tried in international courts, while the BBC is asking questions after Extra News TV’s Noha Darwish mistakenly read, “This was sent from a Samsung device” on the teleprompter while covering the story.

Meanwhile, the editorial board of the Washington Post has little that’s good to say about the former president, but nevertheless calls his death “cruel and unjust” and suggests it shows how far we, as a nation, have “regressed.” Steven Cook tells us in Foreign Policy that our refusal to get involved in regional conflicts makes us “irrelevant” on the world stage, saying, “Morsi’s truncated presidency and death underline Egypt’s abject and terminal mediocrity on the world stage.”

The other big topic: Afcon 2019. Reuters is laying the negativity on thick by expecting that the heavy security and the CAF corruption scandal will cloud Afcon’s opening on Friday, in spite of hopes that the tournament’s expansion to include 24 teams and switch to mid-year hosting would help to draw positive international attention to African football.

And in the only non-Morsi, non-football-related article of note in the press: A US academic complains to Voice of America about Russian involvement in the Dabaa nuclear plant. VOA also provides an image gallery demonstrating exactly why Egypt needs countries like Russia to help it improve its energy security.

On The Front Pages

Worth Watching

Is Tarek Amer calling for an African version of the ECB? CBE Governor Tarek Amer spoke on the benefits of African nations further integrating their economies, going so far as to call for a unified monetary policy for the continent. Speaking with CNBC Africa on the sidelines of last week’s African Development Bank Annual Meetings in Malabo, Amer said that uniform monetary policy is a key prerequisite to integrating Africa’s economies in addition to unified trade policy standards and guidelines. “We are working [at the Association of African Central Banks (AACB)] toward a unified central bank and currency, in years to come.” Until this happens, African central bankers can do more to start better coordinating their policy decisions, he noted.

Central bank independence is still crucial: Central banks on the continent still need to be independent in order to set proper foreign exchange systems, an aspect indispensable to successful global trade and international contracting “because people want to be paid back in their currency,” he noted.

You can catch the rest of the interview, where Amer espouses the benefits of trade reform in the continent, here (watch, runtime: 6:18).

Infrastructure

Egypt to approve EGP 1.4/kWh price for waste-produced electricity

The Madbouly Cabinet will reportedly set in two weeks the standard waste-to-energy feed-in tariff at EGP 1.40 per kWh according to press sources. The Electricity Ministry will pay EGP 1.03 (c.73%) and beneficiary governorates EGP 0.37 (c.27%) per kWh. The same price was reportedly set by the Ismail Cabinet in May last year. At the time, Energy group Empower was said to be negotiating the price up for electricity it began selling to the North Delta Electricity Distribution Company.

Basic Materials + Commodities

Galina-Agrofreeze proposes EGP 1.2 bn plan in setting up retail franchises

Galina-Agrofreeze Fruits & Vegetables has submitted preliminary studies to the government to propose setting up discount retail outlets across the country, company Chairman Abdel Wahed Soliman said. The proposal would invite partners to own a franchised food store each under the company’s brand. The store will offer low-price merchandise by cutting the middleman, since the outlets’ will be fitted with products straight from Galina-Agrofreeze’s factories. The authorities and the company are set to hold a meeting in the coming period to further discuss the proposal. Funding for the plan, which would cost EGP 1.2 bn, will partially come through the SME Authority’s loan program, which offers retailers loans at 5% interest.

Manufacturing

Kima 2 fertilizers plant to be inaugurated by Sisi on 30 June

Egyptian chemicals company Kima will begin operations at its new manufacturing facility “Kima 2” in Aswan on 30 June after an inauguration ceremony presided by President Abdel Fattah El Sisi, Chemical Industries Holding Co.’s Chairman Emad El Din Moustafa told Youm7. The project cost EGP 11.6 bn, with 62% of the financing coming from a consortium of six banks. The project was scheduled to be completed in November last year but Italian engineering and construction firm Tecnimont asked for a five-month extension and an extra USD 76 mn to complete it.

Egypt Politics + Economics

Govt, CBE and Capmas working on unified definition of the informal economy

The ministries of planning, industry and investment, along with the CBE and Capmas will create a unified definition for the informal economy which will enable the government to produce an accurate estimate of its size, Capmas head Khairat Barakat said. They plan to organize a workshop that will aim at putting a precise definition that would help quantify the size of the informal economy and help set an economic consensus on its impact on GDP figures, Barakat said. Incorporating the informal economy into the formal economy has been a major goal of many past governments and administrations. The government and CBE’s financial inclusion and cashless society initiatives, in addition to the Finance Ministry’s anticipated SMEs Act, are all part of that goal. Egypt has been trying to get the informal economy to be factored by global institutions into their GDP calculations for the country.

My Morning Routine

My Morning Routine looks each week at how a successful member of the community starts their day — and then throws in a couple of random business questions just for fun. Speaking to us this week is Hany Al Sonbaty (LinkedIn), managing partner of Sawari Ventures, a venture capital firm that invests in North African entrepreneurs.

My name is Hany Al Sonbaty. I’m 46 years old and getting greyer (and presumably wiser) by the day. I’m the husband to Dalia Elsokari and father of the theatrical Noor (13) and the resourceful Yousef (9).

I’m privileged to be one of the founders and the managing partner of Sawari Ventures, a venture capital fund-management firm focused on investing in Egyptian and North African early stage companies. We typically invest anywhere between USD 1-3 mn in fast-growing, knowledge-based companies. Beyond the numbers, our ultimate aim is to find the best entrepreneurs, with the desire and capability to build great companies.

My morning routine depends on whether my wife is out running or not, as we alternate in taking responsibility for getting the kids ready for school. Noor is usually up by 6am and gets herself ready, but Yousef requires a monumental “shove” to get out of bed. By 7:40am, the kids are out the door and my wife and I get ready for work. I drop her off, make a short coffee-run detour and head to Sawari. It’s a routine born out of ‘necessity,’ but one of which I have become increasingly fond.

There really isn’t a ‘typical’ day within our line of work. The only “set-in stone” calendar item is a company-wide meeting on Sunday mornings from 11am-1 pm, commonly referred to as the “partners’ meeting.” This usually sets the agenda for the rest of the week. All aspects of the partnership are discussed during this two hour period: the investment agreement pipeline, agreement execution, key portfolio updates, staffing etc.

On any given day, our time is usually split between taking pitch idea meetings, executing agreements (analysis, due diligence, documentation), managing our portfolio of investments and engaging with our investor base and the ecosystem at large. Time allocation varies greatly based on where we are in the fund cycle and with specific events like closing a transaction or preparing for an exit. Portfolio management is the biggest part (timewise) of the job. How best to add value to the companies that we invest in is at the heart of our business, so often we are heavily involved in business development, strategy formulation and implementation, board representation and instilling good governance. We strive to do whatever it takes to help the entrepreneurs succeed.

As a sci-fi fan growing up in the 80s, Star Wars and comic books were a huge part of my childhood. So the new Star Wars trilogy and the entire Marvel Cinematic Universe have a very special emotional resonance with me. Artistically, Infinity War and Endgame did not disappoint. At the same time, Star Wars will always be special — no matter what.

For me, Seinfeld is the best tv-show ever made. The writing is timeless and the scripts are tight. But TV has changed dramatically over my lifetime, and it’s been almost entirely driven by technology. So I also give special mention to two shows made possible by this transformation: The Man in the High Castle and Insecure, which both started off as webisodes on YouTube.

Sawari Ventures is a partnership between Ahmed Alfi, Wael Amin, and me. We all crossed paths during our individual careers.

Prior to founding Sawari, I was in charge of technology, media and telecom investments at EFG-Hermes. Between 1999 and 2009 we invested in over 30 companies (including Masrawy, Otlob, LinkdotNet, and Maktoob) and launched the first venture capital FRA-regulated funds in Egypt, which invested in Si-ware and were among the founding investors in Fawry. I first met Wael nearly 20 years ago, when we invested in his company, ITWorx. Alfi I met later, in 2005. He was an avid techie and tech investor in the US, looking to relocate back to Egypt after 40 years and searching for opportunities here and the region. Seeing Egypt’s immense potential, Alfi relocated in 2006 and was briefly my boss at EFG-Hermes.

Alfi and I joined forces in 2010 to launch Sawari Ventures. Our efforts to raise a dedicated venture capital fund were slowed down by the political and economic situation in Egypt, but we believed in the future and invested our own capital in companies like Kngine (sold to Samsung) and Elves. We also created Flat6Labs, which went on to expand to Saudi Arabia, UAE, Lebanon, Tunisia and Bahrain.

Even before Wael became a partner in Sawari Ventures, he was always there with us. He was one of our portfolio companies’ most dedicated mentors and the go-to person for technology and operational issues. On his 20th anniversary of founding ITWorx, a 1k-strong, USD 50 mn company whose alumni have gone on to start over 150 companies, Wael decided to join us officially.

We recently announced the first closing of our fund, with commitments of nearly USD 40 mn, and are expecting our second closing in 1Q next year, with commitments topping USD 70 mn.

My partners and I all share a passion for entrepreneurship and believe in its immense power to positively transform economies.

Institutional VC is still nascent in the region, and the ecosystem on the whole is on an accelerated learning curve. Perceptions and realities (i.e. ‘rules of the game’ and ‘best practice’) amongst the participants themselves are still not fully aligned or appreciated.

One persistent underappreciated truism is the critical role of personalities in influencing outcomes. Business 101 teaches you that people create value, but most individuals I’ve met just pay lip service to this mantra. In no other industry do people matter more or is their effect as obvious and easily traceable as VC. It’s about the people first, second and third.

The other generally misunderstood issue is the nature of the relationship between the entrepreneur and the venture capitalist. It is a unique (and quite unsettling for the uninitiated) blend of personal and business. On average we hold our investments for five years before we exit. That's a very long time in relationship terms. Like any relationship, you will get out of it (and your investment) what you put in, so align interests and expectations upfront, build trust and don’t make it transactional in nature if you want to see it flourish.

The entire entrepreneurial ecosystem in Egypt and the region is woefully undercapitalized. This is not just in terms of the available funding but also the depth of the investor base itself at various stages of a company’s life (seed, early stage, growth and more growth).

But this is changing at a much faster pace than I had imagined just three or four years ago. Given that a substantial portion of the GDP (healthcare, transport, banking, education, agriculture) will one day be digitized in one form or another, a substantial number of new companies created will be entrepreneur-led. I personally expect that the capital available for VC will increase by close to two orders of magnitude within our lifetime and this will transform our economy beyond the perceived macro constraints.

There are four realizations that have helped me along in business through thick and thin. First: There is no single path to success. As a former boss once told me in his heavy French accent, “Hanneee! You can be an angel or the prince of darkness and still succeed. ” Second: There are no solutions, only trade-offs. Third: Kobayashi Maru: Alfi and I agree on many issues but are diametrically opposed on one: Star Trek vs. Star Wars. Sometimes, he brings up Kobayashi Maru, a fictional training simulation for Star Trek cadets, which is a no-win situation where everyone dies. The moral I take from this is that in a seemingly no-win situation, you have to change your narrative and perspective. Fourth: The sun’ll come out, tomorrow.

The Market Yesterday

Powered by![]()

EGP / USD CBE market average: Buy 16.6939 | Sell 16.7939

EGP / USD at CIB: Buy 16.69 | Sell 16.79

EGP / USD at NBE: Buy 16.69 | Sell 16.79

EGX30 (Wednesday): 14,132.18 (-0.50%)

Turnover: EGP 535 mn (29% below the 90-day average)

EGX 30 year-to-date: +8.41%

THE MARKET ON WEDNESDAY: The EGX30 ended Wednesday’s session down 0.50%. CIB, the index heaviest constituent ended down 0.47%. EGX30’s top performing constituents were Egyptian Resorts up 1.94%, Madinet Nasr Housing up 1.13%, and GB Auto up 0.96%. Yesterday’s worst performing stocks were Arabia Investments Holding down 9.91%, Ezz Steel down 2.34% and Sarwa Capital down 1.65%. The market turnover was EGP 535 mn, and foreign investors were the sole net buyers.

Foreigners: Net long | EGP +9.0 mn

Regional: Net short | EGP -1.0 mn

Domestic: Net short | EGP -7.9 mn

Retail: 47.3% of total trades | 44.0% of buyers | 50.5% of sellers

Institutions: 52.7% of total trades | 56.0% of buyers | 49.5% of sellers

WTI: USD 53.76 (-0.26%)

Brent: USD 62.25 (+0.18%)

Natural Gas (Nymex, futures prices) USD 2.28 MMBtu, (-2.23%, July 2019 contract)

Gold: USD 1,348.80 / troy ounce (-0.14%)

TASI: 8,936.26 (-0.71%) (YTD: +14.18%)

ADX: 4,974.84 (+1.27%) (YTD: +1.22%)

DFM: 2,639.48 (+0.41%) (YTD: +4.34%)

KSE Premier Market: 6,303.52 (-0.04%)

QE: 10,507.40 (+0.84%) (YTD: +2.02%)

MSM: 3,943.46 (+0.72%) (YTD: -8.80%)

BB: 1,453.74 (+0.16%) (YTD: +8.71%)

Calendar

1H2019 (date TBD): Investment Minister Sahar Nasr will head a delegation of businessmen into Mexico City to explore cooperation avenues with the Latin American country.

June: International Forum for small and medium enterprises (SMEs).

June: Egypt will host the first economic forum for Union for the Mediterranean (UfM) countries to promote trade and investment in the 43 member states.

June: The Egyptian Businessmen’s Association will host a delegation of 20 Saudi real estate companies to explore investment prospects.

Mid-June: A delegation of Egyptian businessmen will head to Estonia and Latvia to explore investment prospects in the two eastern European nations.

18-21 June (Tuesday-Friday): President Abdel Fattah El Sisi to attend US-Africa Business summit in Mozambique.

18-22 June (Tuesday-Saturday): The Russia-Africa economic conference and the annual meeting of Afreximbank shareholders will take place in Moscow.

19-20 June (Wednesday-Thursday): Pharos Holding Annual Investor Conference, El Gouna, Egypt.

23 June (Sunday): Cairo Arbitration Court hearing for Amer Group vs. Antaradous for Touristic Development.

25-26 June (Tuesday-Wednesday): US-backed conference on the ‘economic dimension’ of Trump’s Mideast peace plan, Manama, Bahrain.

25-26 June (Tuesday-Wednesday): OPEC conference, OPEC and non-OPEC ministerial meeting, Vienna, Austria.

28-29 June (Friday-Saturday): G20 Global Economic Summit, Osaka, Japan.

30 June (Sunday): June 2013 protests anniversary, national holiday.

July: Customs officials from Egypt and the US will sit down to discuss “procedural and administrative matters” as part of the Trade and Investment Framework Agreements (TIFA).

7 July (Wednesday) The FRA will hear an appeal filed by Adeptio AD Investments, the lead shareholder of Egyptian International Tourism Projects Company’s (Americana Egypt), against an order to submit an MTO for Americana

11 July (Thursday): Central Bank of Egypt’s monetary policy committee will meet to review interest rates.

19-21 July (Friday-Sunday): LED Middle East Expo, Egypt International Exhibition Center, Nasr City, Cairo.

23 July (Tuesday): 23 July revolution anniversary, national holiday.

28 July-02 August (Sunday-Friday): Fab15 Conference and Graduation Ceremony, TU Berlin, El Gouna, Egypt.

30-31 July (Tuesday-Wednesday): US Federal Open Market Committee will hold its two-day policy meeting to review the interest rate.

03-04 August (Saturday-Sunday): Fab15 Festival, Tours, and Conference Closing, GrEEk Campus, Cairo.

7-11 August (Wednesday-Sunday) Eid El Adha (TBC).

22 August (Thursday): Central Bank of Egypt’s monetary policy committee will meet to review interest rates.

29 August (Thursday): Islamic New Year (TBC), national holiday.

September: Cairo will host an Egypt-Hungary business forum, according to a Trade Ministry statement (pdf)

2-4 September (Monday-Wednesday): The Big 5 Construct Egypt, Egypt International Exhibition Center, Nasr City, Cairo.

03-04 September (Tuesday-Wednesday): Shared Services and Outsourcing Forum Middle East, Nile Ritz Carlton, Cairo.

8-11 September (Sunday-Wednesday): Sahara Expo, Egypt International Exhibition Center, Nasr City, Cairo.

9-12 September (Monday-Thursday): The 9th Annual EFG Hermes London Conference, Arsenal Emirates Stadium, London.

17-18 September (Tuesday-Wednesday): US Federal Open Market Committee will hold its two-day policy meeting to review the interest rate.

21 September (Saturday): Cairo’s streets get really, really crowded as students at the nation’s public schools go back to class.

26 September (Thursday): Central Bank of Egypt’s monetary policy committee will meet to review interest rates.

October: A forum will be organized by Russia’s Rosatom and the Nuclear Power Plants Authority to introduce local suppliers and contractors to the Dabaa nuclear plant.

6 October (Sunday): Armed Forces Day, national holiday.

10-13 October (Tuesday-Sunday): Big Industrial Week Arabia 2019, Egypt International Exhibition Center, Nasr City, Cairo.

23-24 October (Wednesday-Thursday): Intelligent Cities Exhibition & Conference, Hilton Heliopolis, Cairo.

23 October-1 November (Wednesday-Friday): CIB PSA Women’s World Championship, Great Pyramid of Giza, Cairo.

28 October-22 November (Monday-Friday): World Radiocommunication Conference 2019, Sharm El Sheikh, Egypt.

29-30 October (Tuesday-Wednesday): US Federal Open Market Committee will hold its two-day policy meeting to review the interest rate.

3-5 November (Sunday-Tuesday): Electrix 2019, Egypt International Exhibition Center, Nasr City, Cairo.

9 November (Saturday): Prophet Mohammed’s birthday, national holiday.

10-14 November (Sunday-Thursday): GeoMEast International Congress and Exhibition, Marriott, Cairo.

14-17 November (Thursday-Sunday): Machtech Expo, Egypt International Exhibition Center, Nasr City, Cairo.

14-17 November (Thursday-Sunday): Transpotech Expo, Egypt International Exhibition Center, Nasr City, Cairo.

14-17 November (Thursday-Sunday): Airtech Expo, Egypt International Exhibition Center, Nasr City, Cairo.

November: Suez Canal Conference for Investment, organized in cooperation with the European Union

December: Egypt will host for the first time the Pack Process trade expo for the Middle East and African region.

3-6 December (Tuesday-Friday): Cairo WoodShow, Egypt International Exhibition Center, Nasr City, Cairo.

9-11 December (Monday-Wednesday): Pacprocess Middle East Africa, Egypt International Exhibition Center, Nasr City, Cairo.

9-11 December (Monday-Wednesday): Food Africa 2019 Expo, Egypt International Exhibition Center, Nasr City, Cairo.

10-11 December (Tuesday-Wednesday): US Federal Open Market Committee will hold its two-day policy meeting to review the interest rate.

26 December (Thursday): Central Bank of Egypt’s monetary policy committee will meet to review interest rates.

9-12 January 2020 (Tuesday-Sunday): PLASTEX, Egypt International Exhibition Center, Nasr City, Cairo.

25 January 2020 (Saturday): 25 January revolution anniversary / Police Day, national holiday.

25 January 2020 (Saturday): Midterm break for public schools and universities. Also known as: Two weeks of good commute.

8 February (Saturday): Midterm break ends. Traffic in Cairo stinks once more.

11-13 February 2020 (Tuesday-Thursday): Egypt Petroleum Show, Egypt International Exhibition Center, Nasr City, Cairo.

25-26 March (Wednesday-Thursday): Mega Projects Conference, Egypt International Exhibition Center, Nasr City, Cairo.

Enterprise is a daily publication of Enterprise Ventures LLC, an Egyptian limited liability company (commercial register 83594), and a subsidiary of Inktank Communications. Summaries are intended for guidance only and are provided on an as-is basis; kindly refer to the source article in its original language prior to undertaking any action. Neither Enterprise Ventures nor its staff assume any responsibility or liability for the accuracy of the information contained in this publication, whether in the form of summaries or analysis. © 2022 Enterprise Ventures LLC.

Enterprise is available without charge thanks to the generous support of HSBC Egypt (tax ID: 204-901-715), the leading corporate and retail lender in Egypt; EFG Hermes (tax ID: 200-178-385), the leading financial services corporation in frontier emerging markets; SODIC (tax ID: 212-168-002), a leading Egyptian real estate developer; SomaBay (tax ID: 204-903-300), our Red Sea holiday partner; Infinity (tax ID: 474-939-359), the ultimate way to power cities, industries, and homes directly from nature right here in Egypt; CIRA (tax ID: 200-069-608), the leading providers of K-12 and higher level education in Egypt; Orascom Construction (tax ID: 229-988-806), the leading construction and engineering company building infrastructure in Egypt and abroad; Moharram & Partners (tax ID: 616-112-459), the leading public policy and government affairs partner; Palm Hills Developments (tax ID: 432-737-014), a leading developer of commercial and residential properties; Mashreq (tax ID: 204-898-862), the MENA region’s leading homegrown personal and digital bank; Industrial Development Group (IDG) (tax ID:266-965-253), the leading builder of industrial parks in Egypt; Hassan Allam Properties (tax ID: 553-096-567), one of Egypt’s most prominent and leading builders; and Saleh, Barsoum & Abdel Aziz (tax ID: 220-002-827), the leading audit, tax and accounting firm in Egypt.