Egyptian debt is still a safe bet for investors

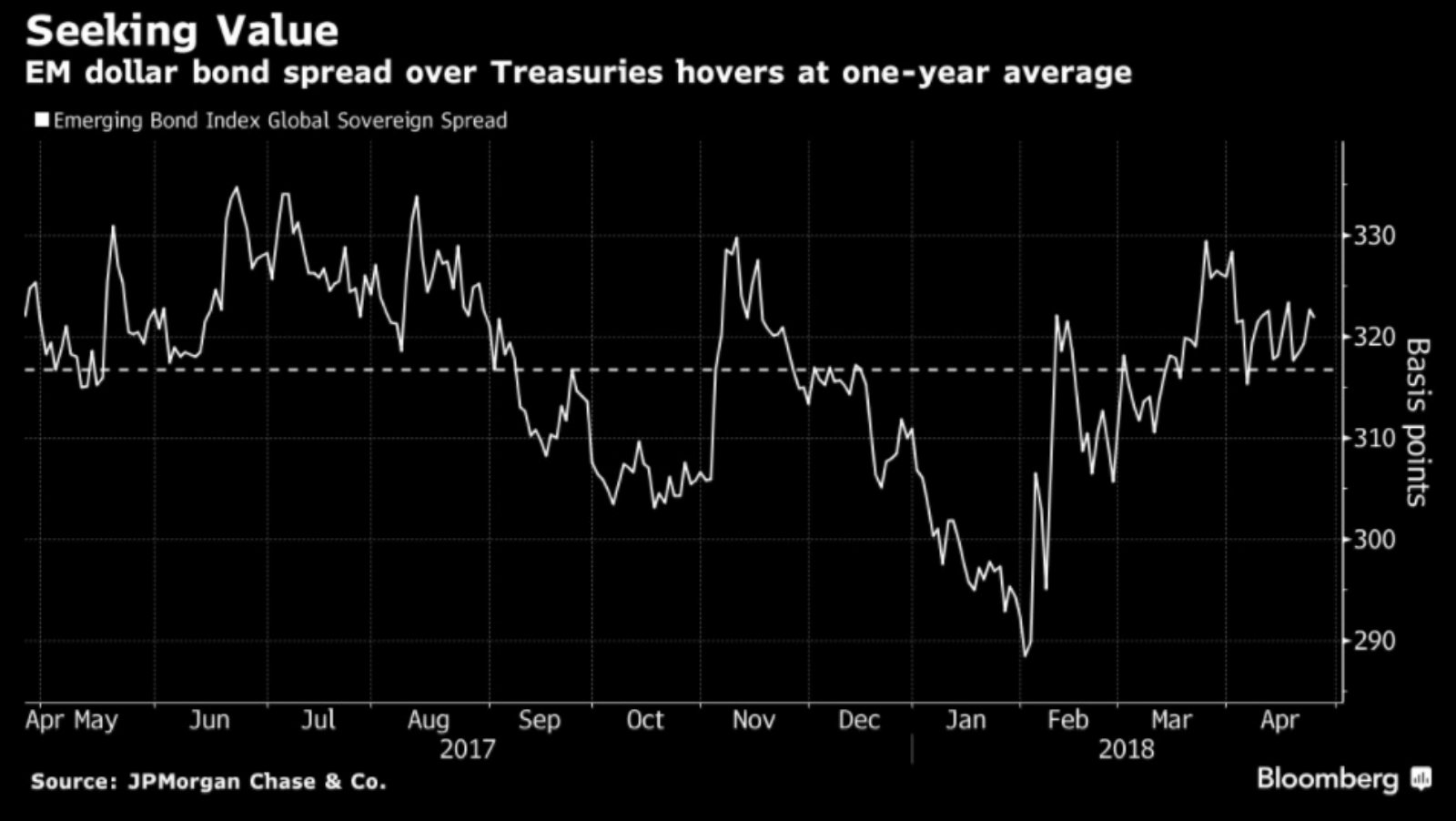

Egypt still attractive to the carry trade. Although rising US interest rates and global acknowledgement of credit risk from government bonds undermines slightly the competitive advantage of emerging markets, there is a view that the gap is still “meaningful enough” to indicate that EMs will do just fine this year. “The trick is to seek securities in places where there’s relatively low interest-rate risk,” Morgan Stanley Investment’s Michael Kushma tells Bloomberg in an interview, where he names Egypt and the Ukraine as two markets where “domestic stories dominate any external factors.” He points out that both countries have been successful in their attempts to raise debt, with Egypt having just raised EUR 2 bn from its first EUR-denominated eurobond sale earlier this month that was 3.8x oversubscribed. Kushma echoes our friend Ahmed Badr, MENA chief at Renaissance Capital, who said much the same thing when we sat down for a chat earlier this week.

But keep an eye on 10-year treasuries, the pundits say: Yields on ten-year US treasuries are now above 3%, a mark that preoccupied anchors on Bloomberg this past Tuesday and that today sees the Financial Times suggesting that the resulting resurgence in the USD could “hit EM carry trade favorites.”

Is shareholder activism becoming a thing in the GCC? It seems to be getting there, “if events of the past week are a guide,” Shaji Mathew writes for Bloomberg. A number of companies in the region — including Damac, Drake & Scull International, and Union Properties — saw their stocks tumble on Monday and Tuesday as shareholders attempted to fire chairmen and board members, asked for new share issuances, and recommended lower dividends. “It’s unusual in the six members of the GCC, where shareholders tend to rubber-stamp board decisions.”