- Our borrowing costs risk being too high and our investment ceiling too low because of a glitch in how a key ratings agency calculates our creditworthiness. (Speed Round)

- Good news on the FX front: Limit on USD 100k in personal transfers abroad to be scrapped, IOCs just got USD 750 mn. (What We’re Tracking Today)

- 13 of 14 economists surveyed by Reuters see the Central Bank leaving interest rates on hold. (Speed Round)

- El Sisi talks social safety net, savings from new gas fields, move to new administrative capital by 2018 in interview with editors of state newspapers. (Speed Round)

- M&A WATCH- Bidding war for United Pharma IV Solutions. (Speed Round)

- EARNINGS WATCH- SODIC reports 321% y-o-y increase in 1Q17 net profits, 71% surge in new contracted sales to EGP 1.2 bn. (Speed Round)

- Education Ministry to announce caps on international school tuition fees. (Speed Round)

- China’s JAC Motors, Hawtai plan to invest in auto manufacturing and components; distributors cut sales forecasts; the Zombie Press can’t let go of our favourite Zombie Company. (Automotive)

- The Markets Yesterday

Wednesday, 17 May 2017

Investigation: Ratings agency’s apparent glitch risks keeps Egypt’s borrowing costs high, investment ceiling low.

TL;DR

What We’re Tracking Today

Our borrowing costs are too high and our investment ceiling limited because of aglitch in how a key ratings agency calculates our creditworthiness. That’s our fundamental takeaway from our investigation of the methodology behind Standard & Poor’s credit rating on Egypt. Even if you’re not an economics geek, take a moment to check out the story, which leads Speed Round this morning. The Brits have the luxury of debating whether sovereign credit ratings matter — those of us schlepping along in emerging markets know they do. And if you’re a fellow econogeek and have a strong opinion on the subject, let us know — whether you agree or disagree with our take — by dropping us a line at editorial@enterprise.press.

The central bank will “soon” scrap its USD 100k limit on bank transfers abroad by private citizens, Governor Tarek Amer said yesterday, according to Reuters. “The limits of [USD 100,000] relating to individuals will be cancelled … We have no need for foreign currency limits,” Amer said.

In a further sign that the nation’s USD position is strengthening: International oilcompanies were just paid USD 750 mn to settle part of their arrears and another USD 750 mn is in the pipeline for payment at the beginning of June, Amer told reporters yesterday. Egypt owes the IOCs about USD 3.5 bn. “Amer said separately that Egypt has received USD 8 bn in investment from 150 global investment funds over the past six months,” Reuters reports.

MSCI is adding EFG Hermes to the MSCI Egypt index, while removing Talaat Moustafa Group (TMG), according to Reuters. The wire service says analysts at EFG estimate flows of around USD 30 mn as a result. The MSCI Egypt index includes CIB, Global Telecom Holding, and EFG Hermes, which replaced TMG. Meanwhile, Al Borsa is concerned that the total weighting of Egypt on the MSCI Emerging Market Index is falling, especially after the drop in market capitalisation following the EGP’s devaluation. This is also a concern as the MSCI Emerging Market Index is set to become a bit more crowded, with Pakistan set to be upgraded to Emerging Markets status from Frontier Markets in June and Argentina being proposed as another candidate for reclassification as EM along with China A-Shares.

Start your morning with what Al Mal says is the final draft of the Investment Act. We’re taking it with a grain of salt because it is dated “Monday, 17 May.” The document is spread over two files here and here, both of them pdfs

Top US diplomat on for Mideast to retire? Stuart Jones, the acting assistant secretary of state for the Near East and the former number two at the US embassy in Cairo, is stepping down, Reuters reports. Jones, who we knew during his service in Egypt as a very bright and engaged guy, “told colleagues the decision was his own and that he had not been pushed out or asked to leave the department.” Outgoing ambassador Stephen Beecroft is named by Reuters as one of the candidates to take over from Jones.

Travel in a time of cholera: Heading to Cairo International this morning? Give yourself a few extra minutes of flex: “Cairo airport is introducing emergency measures, including quarantine, to prevent the spread of a cholera outbreak in Yemen by flights arriving from the war-torn Arab nation,” according to an Associated Press piece picked up by Bloomberg.

Jordan’s King Abdullah II is arriving in Cairo today for talks with President Abdel Fattah El Sisi ahead of the Arab Islamic-American Summit kicking off in Riyadh next week, Al Masry Al Youm reports.

Investment Minister Sahar Nasr is heading to KSA today to meet with Saudi investors and officials from the Islamic Development Bank, Al Mal reports.

The greenback is taking a beating amid White House controversies. It’s not going to do much about the EGP:USD rate, but the furor over US President Donald Trump divulging sensitive intelligence to Russia’s foreign minister has been eclipsed by another flap that has sent USD futures and US shares down in Asian trading today. The latest: Former FBI director James Comey claims Trump asked him to shut down an investigation of Trump’s former national security advisor.

A change in our collective attitude could force the economy to grow 34%. That’s how much Bloomberg says Egypt’s economy would grow if as many women were employed as men. The comparable figure for Japan is 9%, and for the US 5%. You can check out Bloomberg’s Modern Motherhood Has Economists Worried or go check out the 2012 report from Strategy& (pdf) (that’s the outfit formerly known as Booz & Company) that makes the GDP growth projection. The 34% bit is on page 9; the section on Egypt runs pp. 106-112.

This publication is proudly sponsored by

What We’re Tracking This Week

Daba’a nuclear power plant talks at the House: The House of Representatives’ Energy Committee is expected to discuss the Dabaa nuclear power plant agreement this week before the matter goes to the floor of the House for a vote. The news comes as Electricity Minister Mohamed Shaker has reportedly said Egypt and Russia will sign final contracts for the plant within two months.

On The Horizon

We’re still waiting for word of when the IMF Executive Board plans to review and vote on the staff-level agreement that could see Egypt receive the second tranche of the USD 12 bn extended fund facility by the end of June.

The Finance Ministry will ask Prime Minister Sherif Ismail to compel all ministries and government agencies to compile reports special revenue funds under their control. The report will be presented to the House of Representatives to review,Al Borsa said on Tuesday. MPs have been wanting to draft legislation to better monitor the slush funds and connect them to state coffers.

Enterprise+: Last Night’s Talk Shows

President Abdel Fattah El Sisi’s interview with the editors of national newspapers was the highlight of the airwaves last night.

Yahduth fi Misr’s Sherif Amer picked up the headlines, saying that El Sisi reportedly promised more tax exemptions next year and said that food subsidy allocations were weeks away from being doubled. The president also said he would release a detailed statement of account next year to compare Egypt’s figures now against those from when he assumed office and assess how much has been achieved.

On Kol Youm, Amr Adib spoke to Al Akhbar newspaper editor-in-chief Yasser Rezk about the interview, in which El Sisi reportedly told the press that he was going to leave the decision of whether or not he should run for a second term up to the people. Rezk also told Adib that El Sisi said he hopes to see presidents hand over power in Egypt in the same way as happens in France (watch, runtime: 16:26).

Adib also aired a report about Al Araby Group’s newly launched washing machine factory (watch, runtime: 1:52), which officially makes us supersaturated when it comes to news of this particular factory, which the company’s PR flacks have ensured has been in the news all week.

Masaa’ DMC’s Osama Kamal spoke with Social Solidarity Minister Ghada Wali about the last two years of cash subsidy programs Takaful and Karama, which Wali said incorporate some 100k new families each month (watch, runtime: 4:14).

Over on Hona Al Asema, Wali joined Lamees Al Hadidi to talk about the future of state welfare programs. Wali said that her ministry is devising new strategies to provide the neediest people with the necessary support and will submit a report so the cabinet and presidency soon (watch, runtime: 7:23).

Lamees also spoke to the Secretary General of the Federation of Egyptian Chambers of Commerce Alaa Ezz about Ramadan food expos, at which food makers can sell their products directly to consumers at a discount of up to 30% (watch, runtime: 5:43).

Former Interior Minister Habib El Adly was also on the agenda last night. MP Mostafa Bakry told Lamees that he submitted a formal inquiry to Interior Minister Magdy Abdel Ghaffar about El Adly’s alleged disappearance and said that official sources told him that “special efforts” were being employed to arrest him (watch, runtime: 4:18).

Lawyer Mohamed El Gendy, who claims to be on El Adly’s defense team, told Lamees that he was unaware of El Adly’s whereabouts and was surprised when the ex-interior minister was absent from his hearing at the Court of Cassation earlier this week (watch, runtime: 5:21). High-profile criminal defense attorney Farid El Deeb, who represented former president Hosni Mubarak, had earlier told Al Masry Al Youm that (a) he is El Adly’s lawyer; (b) El Adly is in hospital, not on the run; and that (c) he is still pursuing El Adly’s appeal to the Court of Cassation, the nation’s highest appeals court, against a seven-year sentence for corruption.

Speed Round

Speed Round is presented in association with

We think Standard & Poor’s sovereign credit rating model breaks down when applied to Egypt — and that’s preventing an improvement in the rating agency’s outlook on Egypt and a possible upgrade in the credit rating. Why does this matter? Lower credit ratings translate into higher borrowing costs for the state and are a barrier to some investors. At the heart of it: S&P says, qualitatively, that it welcomes the float of the EGP, which it says will do good things for the economy going forward. But quantitatively, their model for assessing our credit rating punishes us for the magnitude of the very same devaluation they say they welcome, making it impossible for them to upgrade our credit rating or outlook. Contrast that with the exceptional performance of Egypt’s eurobonds in the market, which is arguably a real-world, fact-based argument in favour of an upgrade. Here’s the backstory, and how we think S&Ps model is holding Egypt back:

THE BACKGROUND: We spoke by phone with the S&P analyst responsible for Egypt’s credit rating on Monday to dig deeper into the drivers of the agency’s most recent report on the country, in which they affirmed Egypt’s credit rating at B- / Stable on 12 May. “Overall, the situation [in Egypt] is improving,” the credit analyst said. The stable outlook and affirmation of the rating are balanced out by risks arising from fiscal and external deficits and the gradual implementation of reforms. S&P sees GDP growth slowing down to 3.8% from 4.3% in the current fiscal year. That’s because devaluation of the EGP and the subsequent wave of high inflation are seen as weighing heavily on domestic demand, the main driver of economic growth over last years. Instead, foreign and domestic investment are likely to drive growth in the coming period, alongside net exports.

The ratings agency sees the Ismail government’s reforms starting to bear fruit in late2018 and early 2019. Economic growth in 2017 will take a hit as we adjust to the new foreign exchange regime and as inflation continues to be high. And presidential elections in 2018 are likely to cause investors to take a “wait and see” stance. These factors should dissipate by 2019 and, coupled with a rebound in tourism and the start of production from Zohr, should see GDP growth accelerate. S&P thinks the fiscal deficit will narrow to 7% by 2020, pulling general government debt to a declining path that should see it drop to 82% of GDP by 2020.

Before the 12 May report, S&P last looked at Egypt on 11 November 2016. Heading into our call on Monday, our primary question for S&P was how they view the reform measures taken since November, given the stable rating and outlook in their most recent assessment. We were also concerned with how the international bond market was pricing Egyptian debt, as it was cheaper than the higher-rated Nigeria and Ethiopia, for example, and very close to Jordan’s, which carries a significantly higher rating of BB-. (See our take on Ahmed Namatalla’s piece for Bloomberg, Egypt’s performance on the bond market merits a credit upgrade.)

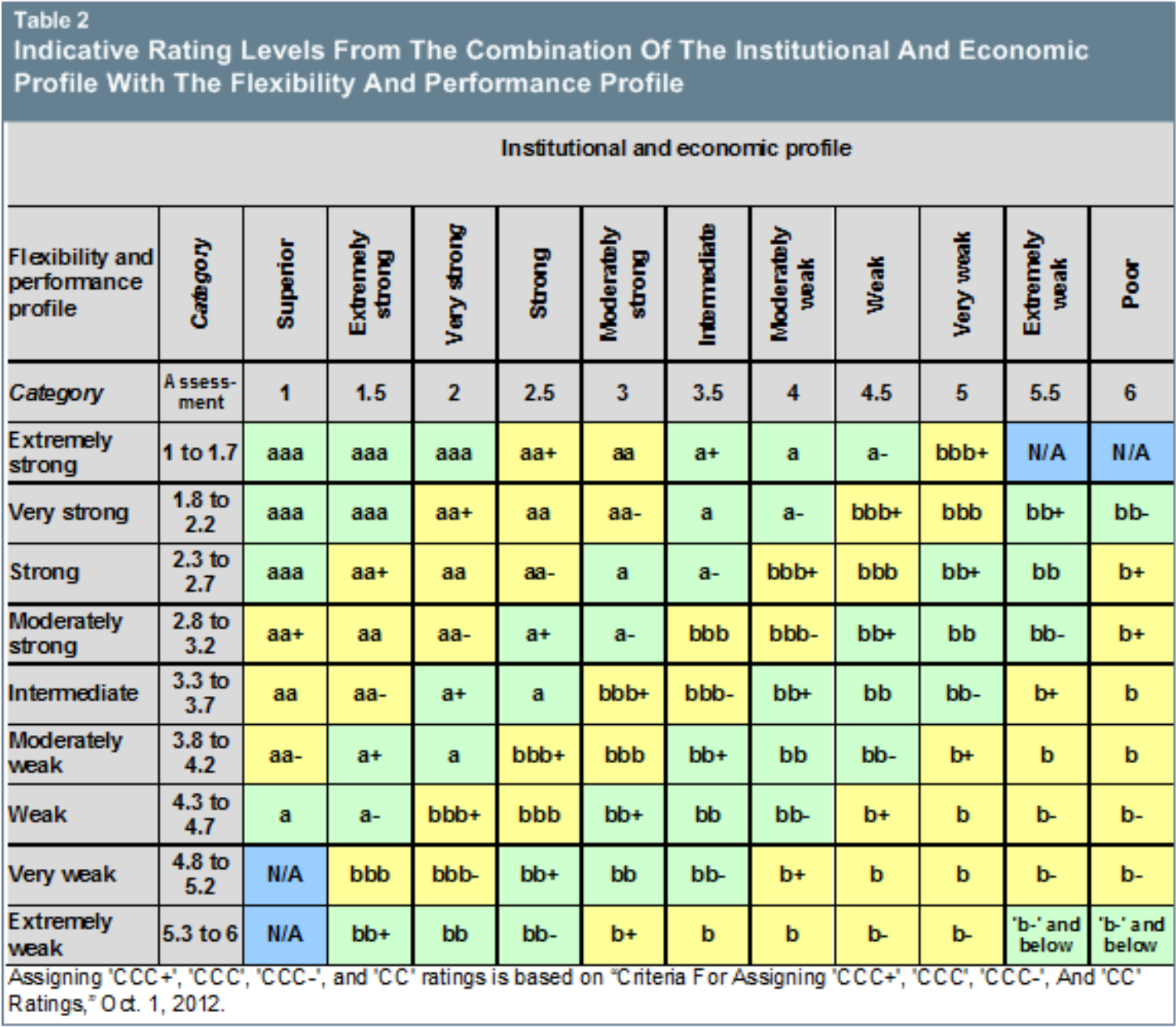

THE METHODOLOGY: This is where we need to get down into the weeds, so bear with us. The sovereign credit analyst explained that S&P’s sovereign credit ratings are driven by five factors that determine credit worthiness: institutional, economic, external, fiscal, and monetary. Together, they provide a sovereign indicative rating level that could then be subject to supplemental adjustment factors and “one notch of uplift / downlift, if applicable.” Each factor is given a score of 1 (strongest) to 6 (weakest). The institutional and economic assessments are averaged to give “the institutional and economic profile,” while the other three factors are averaged to give “the flexibility and performance profile.” The two profiles are used to determine an indicative rating level (specified in a table by S&P) with other factors that allow for the “one notch higher or lower” movement.

{kind=link}

S&P says Egypt’s rating was “constrained by wide fiscal deficits, high public debt,low income levels, and institutional and social fragility,” according to the report. The fiscal deficit, as noted, is on a downward trajectory, bringing down public debt with it, S&P says. The S&P analyst also said “our institutional assessment did not change from the last one in November 2016.”

THE PROBLEM: Look at the rating criteria and you’ll see that the factor that weighed most heavily on S&P’s assessment was our poor performance on GDP per capita, which is measured in USD terms. According to S&P’s figures, USD-denominated GDP per capita dropped to USD 2.9k in FY 2016-17 from a peak of USD 3.7k in FY 2015-16.

Looking at the data provided with the S&P report as well as the S&P Sovereign Rating Methodology, we take issue with the rating agency’s criteria and the model they use. On the economic assessment criteria, S&P says: “The determination of the economic assessment uses the current-year estimate for the GDP per capita from national statistics, converted to [USD].” S&P then considers the real GDP per capita growth trend for the decision to bump the economic assessment score “one category worse or better than the initial assessment.”

S&P uses the same criteria (quite transparently) across all of the sovereigns it rates. The problem is that the methodology is not necessarily reflective of reality in Egypt. According to S&P data, real GDP per capita growth in Egypt grew by 2.9% in FY 2015-16 and by 1.5% in FY 2016-17. At the same time, using the same data, we can see that GDP per capita in USD terms has decreased by nearly 22% between FY 2015-16 and FY 2016-17 and is expected to drop further still by almost 21% to USD 2.3k in FY 2017-18. Since S&P says real GDP per capita growth in Egypt is positive, the expected decreases are then driven entirely by the exchange rate adjustment. GDP, in USD terms, is bound to be significantly lower in FY 2016-17 than in previous years as the currency lost nearly half its value, a drop that is by no means equates to an equal erosion of wealth.

And since the model’s starting point is the USD-denominated GDP figure, it seems clear to us that the ratings framework used by S&P is not responsive to large exchange rate adjustments such as the one we’re living through today in Egypt. S&P described the float of the EGP as “a vital step toward alleviating Egypt’s acute foreign currency shortage, eliminating the differential between the official and unofficial exchange rates and improving the country’s export competitiveness.” But quantitatively, the rating model punishes us for the float in calculating the economic assessment criteria.

Fundamentally, this suggests there are two problems with the model S&P is using for its sovereign credit ratings: First, forcing the USD denomination. Second, aggregating across measures — using averages based on so few criteria can lead to having one outlier causing big shifts, even when it should not.

Our take:

- S&P’s sovereign credit ratings model is broken in the case of Egypt and susceptible to bias.

- The credit rating report issued on 12 May does not necessarily reflect the reality of the economic situation in Egypt, nor the nation’s creditworthiness.

- Future rating decisions will continue to be inadequate as long as the model’s shortcomings are not addressed.

13 of 14 economists surveyed by Reuters see the Central Bank leaving interest rates on hold when it meets this coming Sunday. “There is no need to change interest rates given that monthly inflation indicates the impact of the foreign exchange and energy shocks has dissipated, and with a weak monetary policy transmission mechanism, a rise in interest rates would not curb inflation,” the newswire quotes Arqaam Capital economist Reham Al Desouki as saying. Overnight deposit rates are presently set at 14.75% while overnight lending rates are at 15.75%. The IMF has recently made rumblings about interest rates being the “right instrument” to manage inflation in Egypt. IMF boss Christine Lagarde has singled inflation out as one of Egypt’s biggest challenges at the moment.

President Abdel Fattah El Sisi promised further personal tax exemptions and larger food subsidies to protect the low- and mid-income classes when he spoke to the editors in-chief of state-owned newspapers in his second interview with them this year. The government has plans to battle inflation and expand the social safety net to protect people from the effects of his administration’s economic reforms.

El Sisi gave props to Prime Minister Sherif Ismail for how the PM has steered the ship despite challenges and setbacks. El Sisi also said he was in constant contact with the government to ensure that things are moving according to plan. The president acknowledged that there are shortcomings, but said that they were all being systematically addressed one at a time. He also promised to submit a comprehensive statement out account early next year to compare Egypt now to when he first assumed office and assess how much had been achieved.

Before his time in office is up, El Sisi hopes to have completed most, if not all, the national projects that he promised people.

Other key takeaways from El Sisi’s interview:

- Egypt will save USD 3.6 bn a year once new gas fields come on stream next year, including Zohr, Atoll, and the East and West Delta concessions;

- The emergency law will remain in place and be enforced strictly and without compromise against anyone who threatens national security and stability;

- Ministries and other government offices will move to the New Administrative Capital by the end of 2018.

Egypt is reaping the benefits of the Ismail government’s economic reform program, and the gains are clearest in the return of foreign investments and the increase in foreign reserves, World Bank MENA Vice President Hafez Ghanem said yesterday in an interview with ON Live. Further progress is contingent on continued inflows of investment that creates jobs and makes a dent in the unemployment problem — as well as on improving the country’s education system. Ghanem hinted that Egypt’s ranking in the World Bank’s Ease of Doing Business index will reflect positive developments such as the availability of FX following the EGP float. He also had plenty of nice things to say about the progress on the WB-funded rural sanitation project, including the high speed of implementation. You can watch the interview in full here (runtime 47:30).

M&A WATCH- US investment fund Lincoln Investment, ACDIMA, and a Compass Capital fund are going head-to-head in a race to acquire United Pharma IV Solutions, Al Mal reports. Al Mal says Lincoln’s bid is in the EGP 450-540 mn range, while Compass Capital has offered EGP 450-500 mn, but negotiations are still ongoing. United Pharma favors ACDIMA as a suitor, as “a state company that would make IV solutions available in public hospitals,” Chairman Abdallah Mahfouz tells Al Mal.

EARNINGS WATCH- Our friends at SODIC reported a 321% y-o-y increase in net profit to EGP 211 mn in 1Q2017. The increase came on a 275% y-o-y increase in revenues “reflecting the ramp up in delivered units. Revenues were bolstered by deliveries in Eastown Residences and Westown Residences that combined accounted to more than 80% of the delivered value.” SODIC also says it record a net profit margin of 30%, improving 300 bps from 1Q2016. Managing Director Magued Sherif commented on the results saying: “Our results for the quarter reflect our continuing growth momentum. The strong trust of our clients in the SODIC brand has driven sales growth despite economic headwinds. Driven by our unwavering commitment to delivery, our financial performance is reaping gains. Our excellence in execution is reflected in the strong revenue growth and is solidified by our healthy profitability.” Critically, net contracted sales (essentially the company’s pipeline of future revenues) were up 71% to EGP 1.2 bn in the first quarter.

Orascom Hotels and Development reported consolidated net profit of EGP 75.9 mn in 1Q2017 compared with a EGP 118 mn loss a year before, according to its earnings release. The company reported a 73.8% y-o-y increase in revenues to EGP 493.9 mn in 1Q2017.

Orascom Development Company reported a consolidated net loss of CHF 12.5 mn in 1Q17, compared with a net loss of CHF 31.9 mn in 1Q16, according to its earnings filing. Real estate revenues reached CHF 12.3 mn in 1Q17 compared with CHF 21.7 mn in 1Q16.

Crédit Agricole Egypt grew its net profit for 1Q2017 by 51.6% to EGP 457.1 mn, the bank’s Managing Director François Edouard Drion told the press on Tuesday.

Education Ministry to announce caps on international school tuition fees: The Education Ministry is expected to announce a new system regulating tuition fees at international and private schools, Youm7 reports, citing unnamed ministry sources. According to the sources, Minister Tarek Shawki is refusing to allow schools to hike fees by 20% each year and will cap price increases at 7-15%. Schools will be evaluated individually and their quality will determine the maximum annual fee hike they’ll be permitted. International schools had said in January that they should be regulated by the Investment Ministry, rather than the Education Ministry, after Shawki’s predecessor El Hilali El Sherbini placed the International School of Choueifat and the American International School under administrative and financial supervision last year.

DISTRACTIONS- Tech geeks who happen to worship at the temple of Apple will want to check out wunderkind Mark Gurman’s latest for Bloomberg, wherein he claims Apple will be refreshing the MacBook Pro, 12-inch MacBook and (just maybe) the MacBook Air at WWDC in a few short weeks’ time. Finance geeks will doubtless not be short of opinions on the notion that 2016 was the worst year for hedge fund pay since 2005, the Financial Times and New York Times report. And if our deep dive into S&P’s methodology isn’t enough for you, econogeeks will want to check out the FT’s piece on how demographics are going to hobble both Asia and Africa in the future. Asia could grow old before becoming rich, but Africa’s population growth may prevent it from ever becoming wealthy.

Image of the Day

Throwback to before being stuck on Salah Salem was a valid excuse for being late: Once upon a time, a Belgian entrepreneur by the name of Édouard Empain saw in a stretch of desert the potential for a fully equipped “city of luxury,” and went about building what is now Heliopolis. Empain commissioned a French architect to build the Hindu-style Baron Palace in the middle of an enviable amount of empty land — a far cry from its current state of being surrounded by hotels and apartment buildings. Good thing Empain didn’t live long enough to experience gridlock traffic jams for which his town has become notorious.

Egypt in the News

Coverage of Egypt in the foreign press is picking up once again this morning, with international outlets offering up a varied assortment of stories. President Abdel Fattah El Sisi’s phone call on Monday night with Donald Trump is getting some digital ink from the Associated Press, which reminds us again of the two presidents’ blossoming friendship. This comes as CNN’s Elizabeth Mackintosh writes another piece about Trump’s affinity for “authoritarian leaders,” El Sisi included.

Also getting attention from the AP is Poland’s investigation of the death of a 27-year-old Polish woman vacationing in Egypt. The investigation is looking at murder, a nervous breakdown, and human trafficking as possible scenarios leading to the tourist’s death.

The Egyptian media’s “wave of highly unusual” criticism of Al Azhar is indicative of friction between the religious institution and the state, Heba Saleh writes for the Financial Times. “The tensions illustrate the complexity of the challenges facing the president as he tries to influence the religious sphere, while also fighting jihadis and cracking down on other opponents,” Saleh says, noting President Abdel Fattah El Sisi’s repeated attempts to push Al Azhar to reform itself and religious discourse as a whole. El Sisi’s evident frustration with Al Azhar for “turning a deaf ear” has emboldened media figures and MPs alike, with one MP going so far as to propose a bill that would allow the president to sack the Grand Imam. On the flipside, some analysts say El Sisi’s best bet is to support freedom of expression and political freedoms, which will yield a more tolerant society.

CNN apparently just caught wind of a ridiculous bill being drafted to restrict access to social media including Twitter and Facebook by requiring registration with the government. “Successful applicants would receive a login linked to their national ID. Unauthorized use could result in prison sentences and heavy fines,” writes Kieron Monks, who misses the mark entirely: The bill’s chances of passing are nil, and even if it were to go through, the ease with which Egyptians find ways to poke holes in any system…

Other coverage in the international media worth a skim:

- There’s a new joint for bikers in Zamalek, Reuters reports.

- “I saw myself being defamed in state-controlled media as a traitor [after 2013],” Amr Hamzawy says in an interview with Carnegie Middle East Center’s Michael Young.

- The dispute between Egypt and Ethiopia over the Grand Ethiopian Renaissance Dam should be resolved “by technical experts and legal bodies that would base any recommendations as to water flows etc. on an independent and impartial evaluation under the direction of an international body,” Tuhimi Akebet writes for Australia’s Eureka Street.

On Deadline

Sometimes, it takes a foreigner to point out that here in Egypt, the sky is notnecessarily falling: Egypt has gone through the ringer these past few years, but there are plenty of indicators that suggest the country is on the upswing, high profile Emirati business leader Khalaf Al Habtoor writes in an optimistic column penned for Youm7. While many in Egypt feel dejected by the outcome of the revolution and are struggling with inflation, the country needs its people to do what they can to push for progress, rather than give up altogether. Our past is also chock-full of examples of success and prosperity that give us a solid foundation to build upon, Al Habtoor says, reminding us that now-booming Dubai was basically built from scratch.

Worth Watching

Who needs a toothbrush? Russian professional diver Vitaly Bazarov was about 100 ft under water off Sinai when he got some dental check-up from some inquisitive fish. Bazarov let a pair of cleaner fish inside his mouth as they were nibbling his lips and looking for food. He removed his regulator and let the cleaner wrasses clear the inside of his mouth. Diving and a free dental cleaning — the latest offering in medical tourism for Egypt? (Watch, runtime 0:31)

Diplomacy + Foreign Trade

Negotiations between Egypt and Ethiopia over the Grand Ethiopian Renaissance Dam (GERD) have “failed,” Al Masry Al Youm said ominously yesterday, citing unnamed sources. The Irrigation Ministry said that following a round of meetings, a few technical points remain unaddressed and will be looked into in a future meeting, without setting a time or date. Sudanese sources told AMAY the Ethiopian delegation showed no flexibility and refused to compromise when met with Egyptian concerns.

Sudanese President Omar Al Bashir continued to slam Egypt in the Mideast press on Tuesday, driven by his quest to retake Shalatin and Halayeb — Egyptian territory that is also claimed by Sudan. The venue this time: An interview with Qatari newspaper Al Sharq in which he is reported to have said that Egypt occupied Halayeb at a time when Khartoum was “busy rallying against the rebellion from the South.” He said that the occupation created a deep chasm in Egyptian-Sudanese relations and that Khartoum is willing to go to arbitration to resolve the matter.

The Bahraini government and private sector investors are considering opportunities in the Suez Canal Economic Zone and the 1.5 mn feddans project, Bahrain’s Deputy Prime Minister Sheikh Khalid bin Abdulla Al-Khalifa said, according to Ahram Gate.

Investment and International Minister Sahar Nasr signed a contract for EUR 100 mn loan from the French Development Agency (AFD) for the EUR 360 mn Alexandria tram project, the ministry said in a statement yesterday.

Italy’s Deputy General Prosecutor Sergio Colaiocco arrived in Cairo on Tuesday with a delegation for a two-day visit to follow-up on the latest in the investigation into the murder of Italian graduate student Giulio Regeni, AMAY reported.

A delegation of German central bank officials lands in Cairo today, AMAY reports. The Germans will meet with Central Bank Governor Tarek Amer and Investment and International Cooperation Minister Sahar Nasr.

House of Representatives Speaker Ali Abdel Aal led a delegation to Tokyo on Tuesday night, Ahram Gate reports.

Energy

Production from Nooros surpasses 1 bcf/d

Gas production from the Nooros field has exceeded 1 bcf/d, Reuters reports. Eni, which manages the field, has said last year it plans to raise production to more than 1 bcf/d in 1Q2017.

Saudi Arabia set to trade electricity with Africa through Egypt by 2020

Saudi Arabia is planning to sell electricity with Africa by 2020 via Egypt, Gulf Business reports. In addition to linking up with Egypt, Saudi Arabia is also looking to connect its power grid to Europe through Turkey, Energy, Industry, and Natural Resources Minister Khalid Al Falih said.

Basic Materials + Commodities

GASC launches global wheat tender

The General Authority for Supply Commodities launched a global tender yesterday for an unspecified amount of wheat, to be delivered between 15 and 24 June, according to Reuters’ Arabic service.

Health + Education

State-funded universities to launch electronic aptitude testing system for new applicants next year

State-funded universities that require students to take aptitude tests during the application process will be implementing a new electronic testing system as of the upcoming school year in a bid to cut back on red tape and reduce bureaucratic procedures, Ahram Gate said on Tuesday.

Tourism

Pickalbatros Hotels launches new EGP 1 bn hotel and aqua park in Sharm El Sheikh

Pickalbatros Hotels launched its newest EGP 1 bn hotel in Sharm El Sheikh on Tuesday in a ceremony featuring Portuguese football star Cristiano Ronaldo and his family, Al Borsa said on Tuesday. The project will open on 19 May and features what company officials claim is the Middle East’s largest water park.

Telecoms + ICT

CIT Ministry signs MoU with Visa Inc

CIT Minister Yasser El Kady signed an MoU with Visa President Ryan McInerney to develop Egypt’s digital infrastructure for financial transactions, according to a cabinet statement. McInerney also met with President Abdel Fattah El Sisi to discuss cooperating on the government’s electronic payment program, Al Mal reports.

Automotive + Transportation

China’s JAC Motors, Hawtai planning to increase investments in Egypt

China’s Hawtai is looking to invest as much as USD 1 bn in Egypt’s auto manufacturing and component industries, the head of the company’s international department Jeffrey Zhang told Trade and Industry Minister Tarek Kabil, Ahram Gate reports. Kabil also met with deputy manager of JAC Motors’ international trade division Steven Wang, who told the minister that the Chinese company is studying setting up a factory in Egypt to expand its investments in Africa. Kabil invited both officials to visit Egypt soon to further discuss the projects.

Auto companies decrease sales targets due to market slowdown

Car distributors companies are slashing their sales targets for the remainder of the year by 30-50% due to the market slowdown following the EGP float, Al Mal reports.

Plans to revive El Nasr Automotive not going so well, negotiations stalled

If there’s one company that has captured the attention of a certain generation of local-press journalists, it’s Nasser-era pet project El Nasr Automotive, where “a source” tells Al Mal that negotiations with potential foreign partners to restart operations at El Nasr have stalled. Shocking. To hear the local press tell it, the defunct national car manufacturer had plans to begin operations by June. El Nasr needs EGP 300-500 mn to modernize its WWII-era equipment, they add. The company was in talks with Chinese companies last year to secure USD 20 mn in funding needed to revive the company.

Banking + Finance

Crédit Agricole has no plans to exit its Egypt operations -Drion

Crédit Agricole is not planning on exiting its operations in Egypt, Crédit Agricole Egypt Managing Director François Edouard Drion told Al Mal. Drion added that Crédit Agricole Egypt has already received a USD 10 mn bridging loan from its parent to support operations in Egypt. He says there is a USD 20 mn tranche remaining, of which USD 10 mn is scheduled to be disbursed this month.

Egypt Politics + Economics

Gov’t initiates EGP 1 bn employment program

The government has agreed to allocate EGP 1 bn to the Forsa employment program, which aims to create job opportunities across different governorates and villages Al Borsa reports. Social Solidarity Minister Ghada Waly said her ministry is already in negotiations with a number of private sector companies to increase employment. She added that beneficiaries of the Takaful and Karama programs will not be eligible for Forsa. Waly noted that there are 8 mn people currently benefiting from Takaful and Karama, on which the government spent EGP 7.4 bn to date. Wali also said she expects the fourth USD 65 mn tranche of the World Bank’s USD 400 mn loan to support Takaful and Karama to be disbursed within a few weeks.

On Your Way Out

The Finance Ministry issued a procedural document yesterday that extends the moratorium on implementing the capital gains taxes for stock-market transactions until the 0.125% stamp tax is approved by the House of Representatives and published in the official gazette, Al Borsa said on Tuesday. Deputy Finance Minister Amr El Monayer had said he expects the levy, which will increase gradually to 0.175% over a three-year period and replace the capital gains tax, to come into effect in late May or early June.

Dubai-based delivery business Fetchr announced raising USD 41 mn series B financing round led by New Enterprise Associates (NEA), according to CPI Financial. Other investors in the round include Nokia Growth Partners, Raed Ventures, Iliad Partners, BECO Capital, YBA Kanoo , Venture Souq, and Swicorp. The funding will be using to “continue expanding globally and developing its proprietary technology.” Fetchr, which currently operates in UAE, Saudi Arabia, Egypt, and Bahrain, “tackles the ‘no address problem’ in emerging markets, typically encountered by traditional companies delivering packages to customers” by “going directly to customers’ phone and capturing the geo-location for package deliveries.”

At least one in four children in the MENA region live in poverty, according a UNICEF study. “These children are deprived of the minimum requirements in two or more of the most basic life necessities including basic education, decent housing, nutritious food, quality health care, safe water, sanitation and access to information.”

The markets yesterday

Powered by![]()

EGP / USD CBE market average: Buy 18.0376 | Sell 18.1397

EGP / USD at CIB: Buy 18.05 | Sell 18.15

EGP / USD at NBE: Buy 17.95 | Sell 18.05

EGX30 (Tuesday): 12,937 (+0.6%)

Turnover: EGP 1.5 bn (40% below the 90-day average)

EGX 30 year-to-date: +4.8%

THE MARKET ON TUESDAY: The EGX30 ended Tuesday’s session up 0.6%. CIB, the index heaviest constituent ended up 0.7%. EGX30’s top performing constituents were: Porto Group up 10.0%, EFG Hermes up 7.4%, and SODIC up 3.1%. Yesterday’s worst performing stocks were: TMG Holding down 9.9%, ACC down 2.3%, and GB Auto down 1.7%. The market turnover was EGP 1.5 bn, and foreign investors were the sole net buyers.

Foreigners: Net Long | EGP +87.1 mn

Regional: Net Short | EGP -24.5 mn

Domestic: Net Short | EGP -62.6 mn

Retail: 59.0% of total trades | 58.0% of buyers | 59.9% of sellers

Institutions: 41.0% of total trades | 42.0% of buyers | 40.1% of sellers

Foreign: 24.4% of total | 27.3% of buyers | 21.6% of sellers

Regional: 14.2% of total | 13.3% of buyers | 15.0% of sellers

Domestic: 61.4% of total | 59.4% of buyers | 63.4% of sellers

WTI: USD 48.13 (-1.09%)

Brent: USD 51.15 (-0.97%)

Natural Gas (Nymex, futures prices) USD 3.24 MMBtu, (+0.15%, June 2017 contract)

Gold: USD 1,242.30 / troy ounce (+0.48%)

ADX: 4,582.07 (+0.39%) (YTD: +0.79%)

DFM: 3,376.75 (-0.03%) (YTD: -4.37%)

KSE Weighted Index: 402.46 (-0.07%) (YTD: +5.89%)

QE: 10,125.44 (+0.07%) (YTD: -2.98%)

MSM: 5,432.61 (+0.30%) (YTD: -6.05%)

BB: 1,313.59 (+0.12%) (YTD: +7.63%)

Calendar

14-17 May (Sunday-Wednesday): Arab Sustainable Development Week, Nile Ritz-Carlton, Cairo.

15-17 May (Monday-Wednesday): Morgan Stanley’s 3rd Annual GEMS Conference (EEMEA), London.

21 May (Sunday): Central Bank of Egypt’s Monetary Policy Committee Meeting.

22-23 May (Monday-Tuesday): North Africa Mobile Network Optimisation Conference, Cairo.

27 May (Saturday): First day of Ramadan (TBC).

07-09 June (Wednesday-Friday): 19th Annual Africa Energy Forum, Copenhagen, Denmark.

26-28 June (Monday-Wednesday): Eid Al-Fitr (TBC).

30 June (Friday): 30 June, national holiday.

15-19 July (Saturday-Wednesday): SSIGE’s GeoMEast 2017 International Congress and Exhibition, Sharm El Sheikh.

23 July (Sunday): Revolution Day, national holiday.

02-05 September (Saturday-Tuesday): Eid Al-Adha, national holiday (TBC).

17-19 September (Sunday-Tuesday): Pipeline-Pipe-Sewer-Technology Conference & Exhibition, Intercontinental Citystars Hotel, Cairo.

18-19 September (Monday-Tuesday): Euromoney Egypt conference, venue TBD.

20-23 September (Wednesday-Saturday): 2017 Automech Formula car expo, Cairo International Convention Center, Nasr City, Cairo.

22 September (Friday): Islamic New Year, national holiday (TBC).

03-05 October (Tuesday-Thursday): J.P. Morgan’s Credit and Equities Emerging Markets Conference, London, UK.

06 October (Friday): Armed Forces Day, national holiday.

18-20 October (Wednesday-Friday): AfriLabs annual gathering with the theme “Smart Cities,” The French University, Cairo. Register here.

01 December (Friday): Prophet’s Birthday, national holiday.

08-10 December (Friday-Sunday): RiseUp Summit, Downtown Cairo.

Enterprise is a daily publication of Enterprise Ventures LLC, an Egyptian limited liability company (commercial register 83594), and a subsidiary of Inktank Communications. Summaries are intended for guidance only and are provided on an as-is basis; kindly refer to the source article in its original language prior to undertaking any action. Neither Enterprise Ventures nor its staff assume any responsibility or liability for the accuracy of the information contained in this publication, whether in the form of summaries or analysis. © 2022 Enterprise Ventures LLC.

Enterprise is available without charge thanks to the generous support of HSBC Egypt (tax ID: 204-901-715), the leading corporate and retail lender in Egypt; EFG Hermes (tax ID: 200-178-385), the leading financial services corporation in frontier emerging markets; SODIC (tax ID: 212-168-002), a leading Egyptian real estate developer; SomaBay (tax ID: 204-903-300), our Red Sea holiday partner; Infinity (tax ID: 474-939-359), the ultimate way to power cities, industries, and homes directly from nature right here in Egypt; CIRA (tax ID: 200-069-608), the leading providers of K-12 and higher level education in Egypt; Orascom Construction (tax ID: 229-988-806), the leading construction and engineering company building infrastructure in Egypt and abroad; Moharram & Partners (tax ID: 616-112-459), the leading public policy and government affairs partner; Palm Hills Developments (tax ID: 432-737-014), a leading developer of commercial and residential properties; Mashreq (tax ID: 204-898-862), the MENA region’s leading homegrown personal and digital bank; Industrial Development Group (IDG) (tax ID:266-965-253), the leading builder of industrial parks in Egypt; Hassan Allam Properties (tax ID: 553-096-567), one of Egypt’s most prominent and leading builders; and Saleh, Barsoum & Abdel Aziz (tax ID: 220-002-827), the leading audit, tax and accounting firm in Egypt.